- 화장품 뷰티의 비중이 상승하고 있는데, 디바이스는 공격적인 전략 포기한건지?

- 미국을 졸라게 파는 이유는?

- 매출 규모 대비 B2B가 적다. 그 이유는? 앞으로는 영업 어떻게할 계획인지?

20250217_company_437262000.pdf

0.85MB

'Finance Investment > Investment_report' 카테고리의 다른 글

| 250204_왜 기술주는 항상 미국의 독차지란 말인가?: [교육 시스템, 인재 유입 시스템, 거대 내수시장, 금융 시스템]의 선순환 구도 (0) | 2025.02.04 |

|---|---|

| 241227_국제수지로 본 한국 외환위기 가능성 (1) | 2025.01.02 |

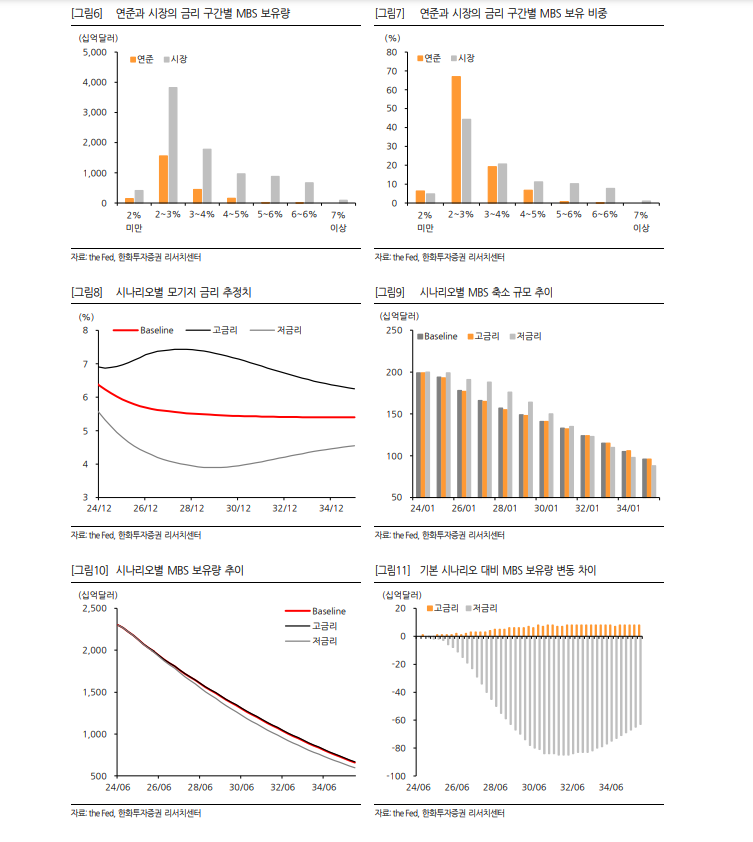

| 241224_장기간 QT에도 불구, MBS 축소가 더딘 이유 (0) | 2024.12.24 |

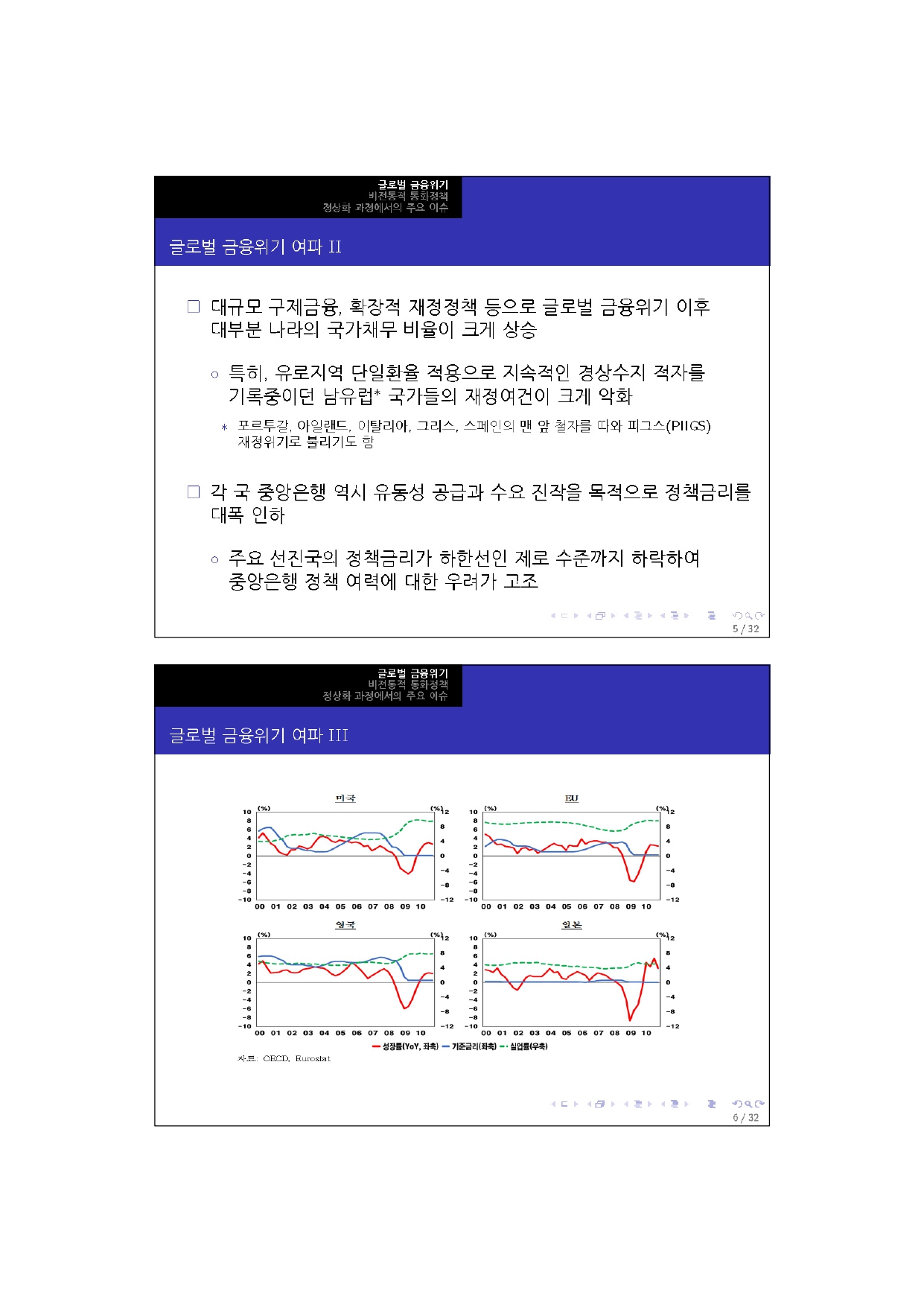

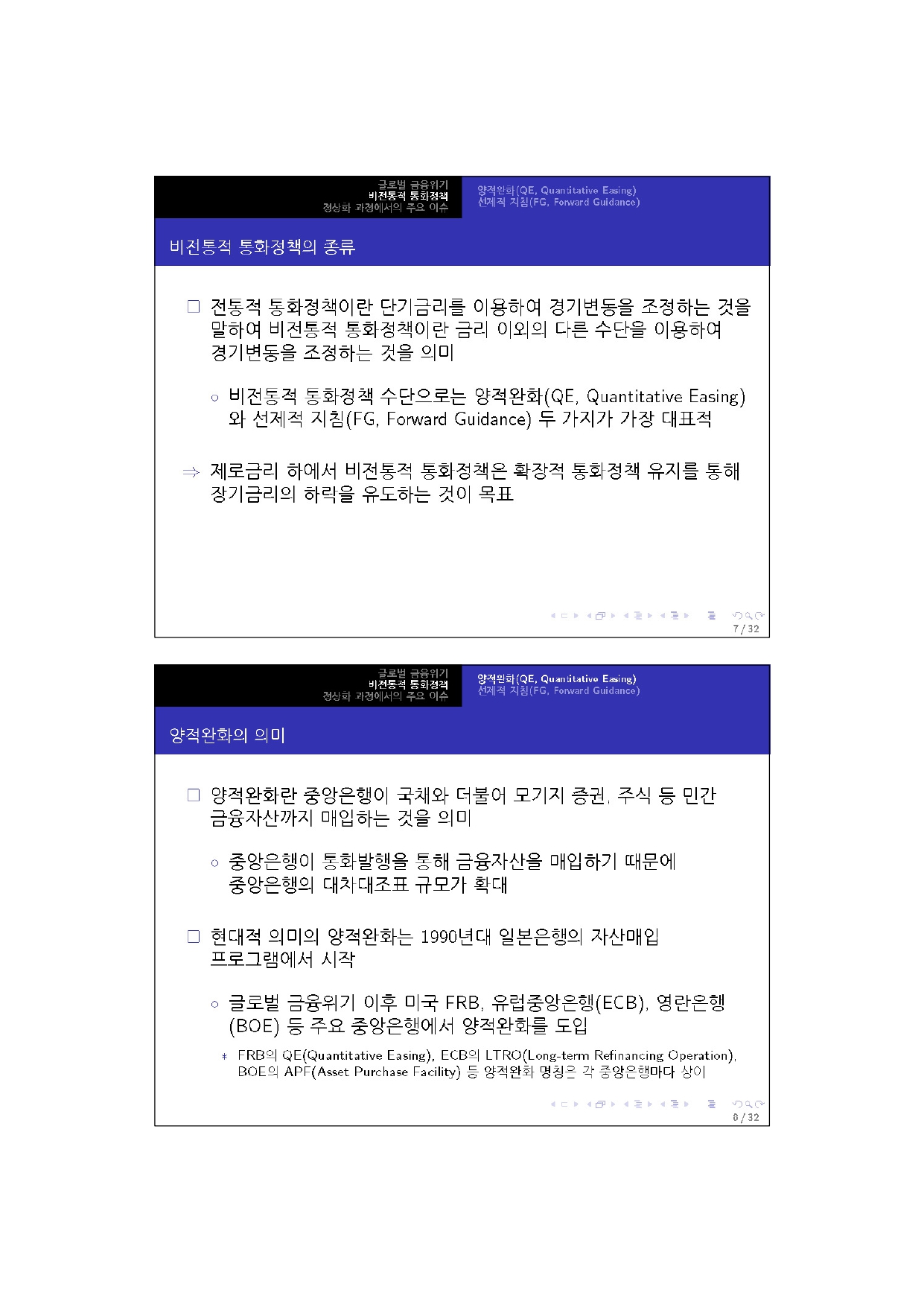

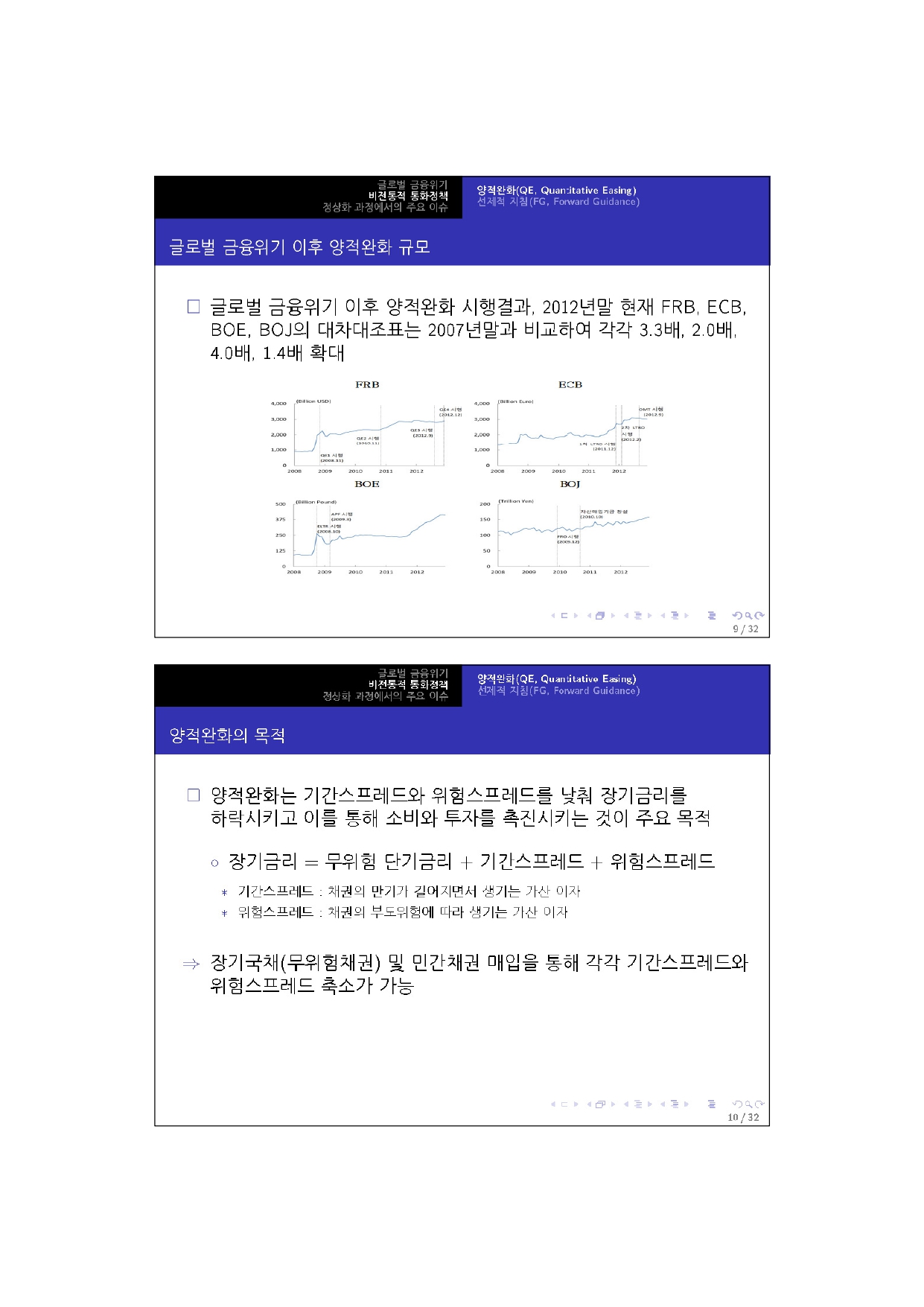

| 241111_비전통 통화정책의 효과와 정상화 과정에서의 주요 이슈 (0) | 2024.11.11 |

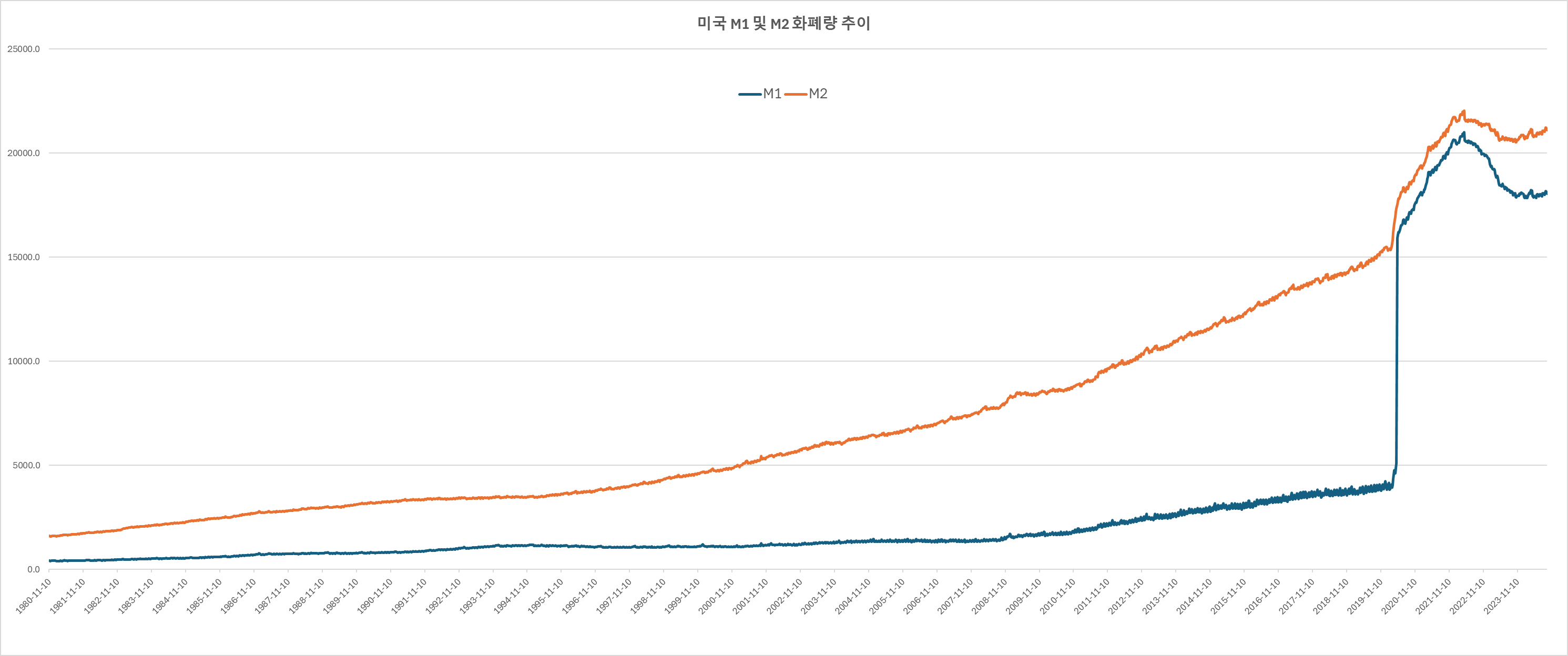

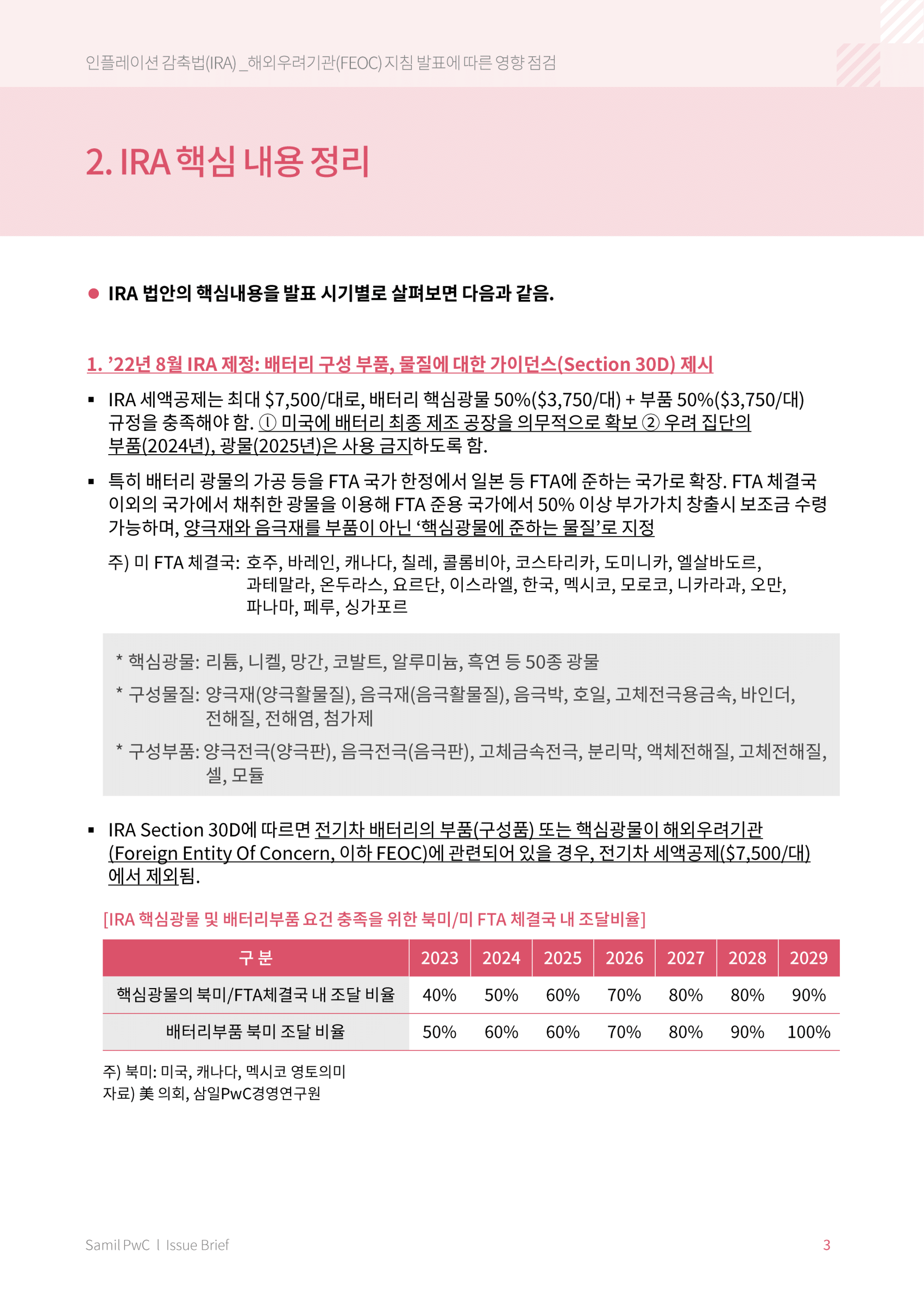

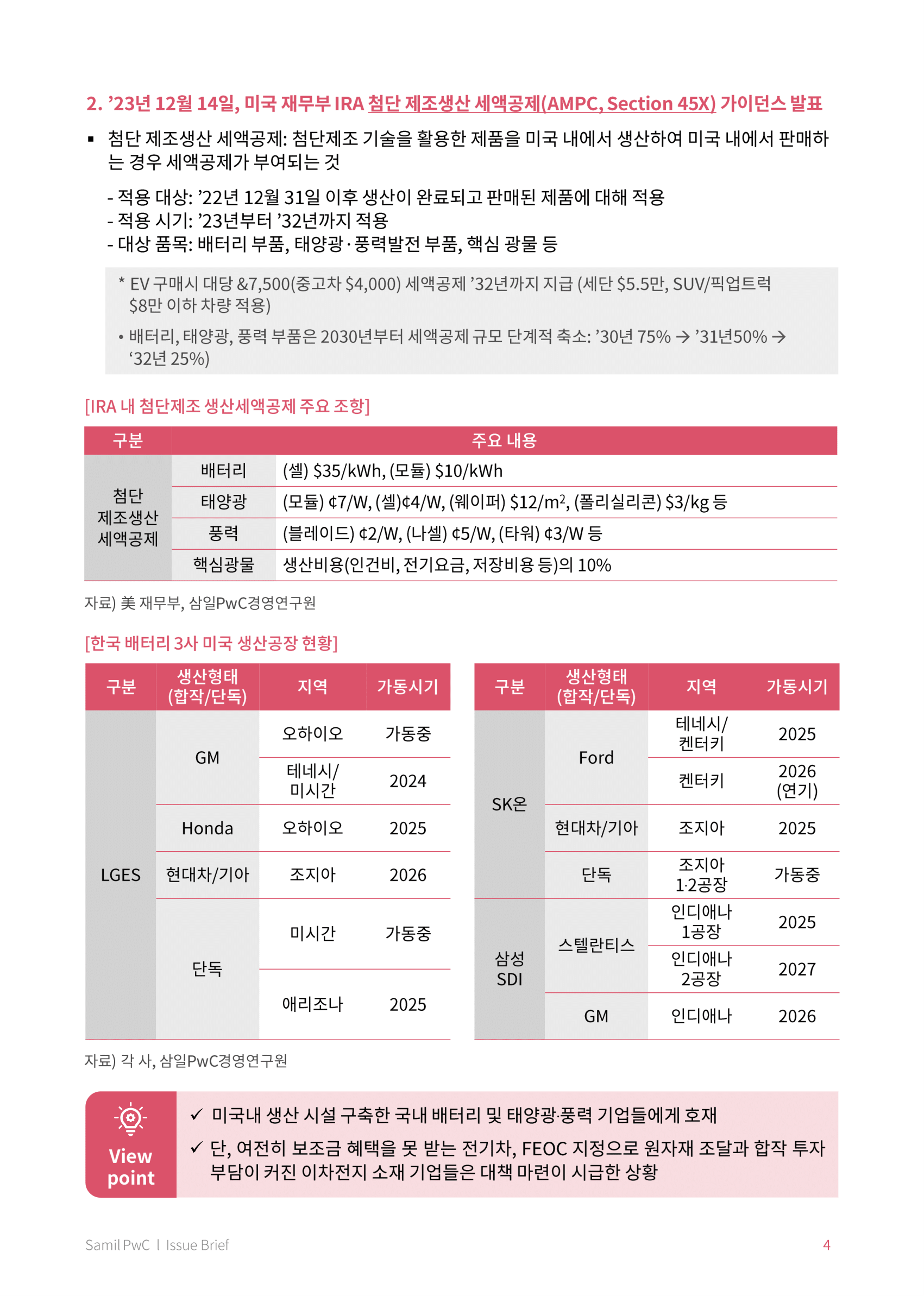

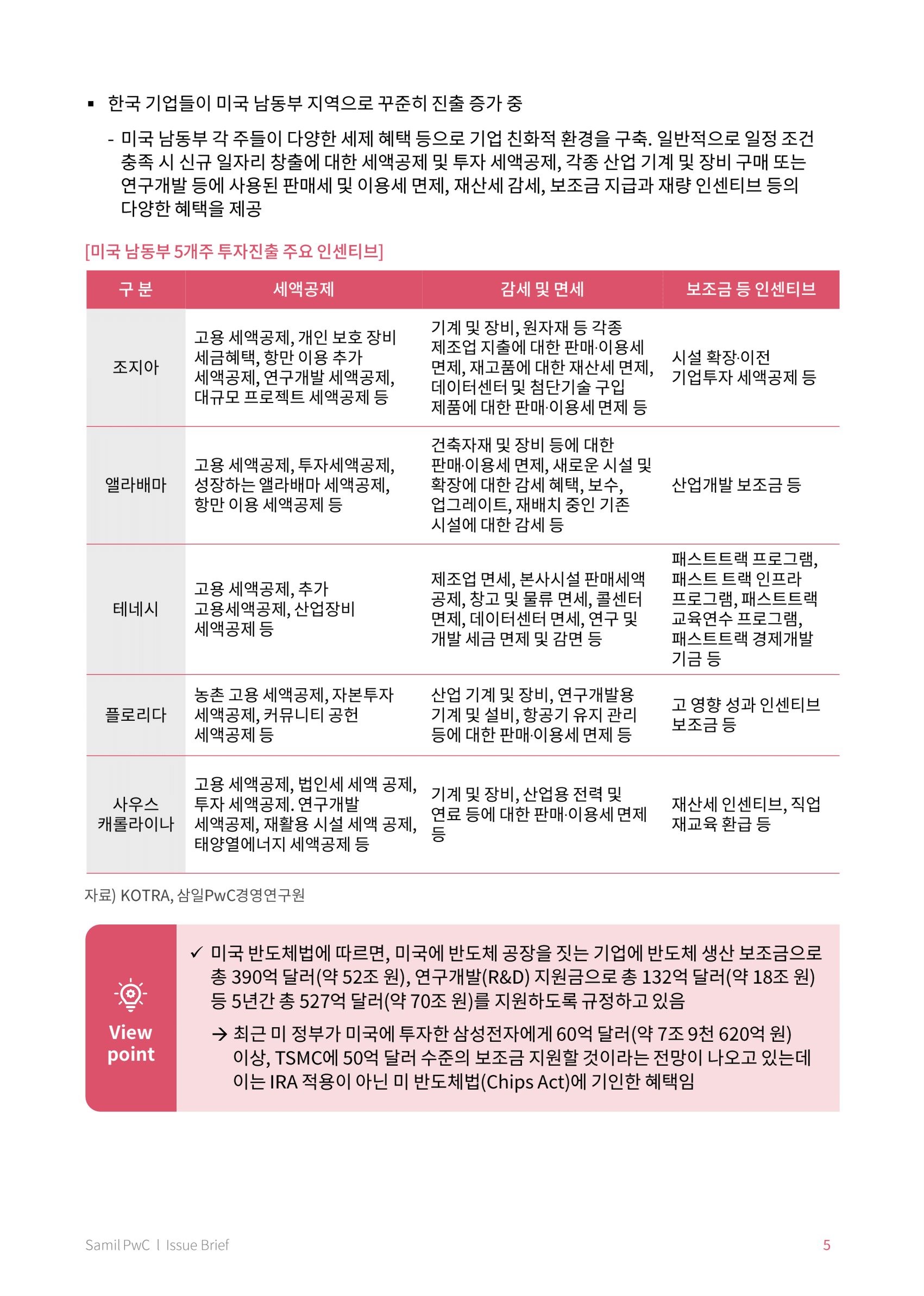

| 240301_PwC: 인플레이션감축법 IRA에 따른 영향 점검 (0) | 2024.10.29 |