부동산 PF (Project Financing). 말 그대로 프로젝트 자체의 사업성을 보고 대출을 실행하는 것을 말합니다.

일반 대출과 차이점

일반적인 대출의 경우 돈을 빌려주는 사람(대주)은 돈을 빌린 사람(차주)의 상환능력과 상환이 지연될 경우 최소한 이자를 지급할 수 있는 능력을 보고 진행 여부를 결정하게 됩니다. 반면 부동산 PF의 경우 미래에 지어질 건물(담보물)과 그 건물을 분양해서 발생하는 현금흐름(상환능력)을 보고 대출 여부를 결정하게 됩니다.

부동산 PF를 이해하기 위해서는 돈을 빌려주는 입장이 되어 생각해볼 필요가 있습니다.

담보물이 없는 상황에서 리스크를 최소화하려면 무엇을 믿고 빌려줘야 할까요?

돈을 빌려주는 대주 입장에는 빌려준 돈을 못 갚을 가능성을 대해 2가지 고민이 생기게 됩니다.

첫째 과연 건물을 짓는 업체가 끝까지 말썽 없이 건물을 완성시킬 수 있을까? 중간에 부도가 나거나 자취를 감추면 어떻게 하지? 이런 생각을 할 수 있고요. 둘째 건물이 완성이 되어 담보물이 생겨도 경기가 안 좋거나 기타 상황에 의해 예상처럼 분양이 안 되는 경우가 발생하면 어떻게 하지?라는 고민이 생길 수 있습니다.

PF대출을 안전하게 실행하려면 이 두 가지 고민에 대한 해결책이 있어야 하는데요. 대주는 아래와 같은 방법으로 위험성을 관리하게 됩니다.

먼저 건물이 지어질 수 있을지에 대한 고민은 시공사가 책임을 지고 완성을 하는 것을 확약받는 방식으로 진행을 합니다. 이를 시공사 책임준공이라고 하는데요. 만약 준공을 못하는 상황이 발생하면 시공사가 책임을 지고 대주단의 대출금을 모두 상환해야 합니다. 이런 시공사의 확약에 대한 신뢰는 어떻게 확보할 수 있을까요? 크게 건물을 지을 수 있는 능력이 있는지 기존 "시공능력"을 보고 준공을 못하는 경우 대출금을 갚을 수 있는 현금이 있는지 "상환능력"을 검토하게 됩니다.

시공능력과 달리 상환능력에 대해서는 현금보유액이 풍부한 시공사는 극히 일부입니다. 아무리 재무제표가 좋아도 현금을 쌓아놓고 있는 시공사는 드물기 때문에 시공사가 회사채를 발행하여 자금을 조달할 수 있는지 여부를 판단하게 됩니다. 회사채를 발행할 신용등급이 되지 않는 시공사의 경우 만약 모회사가 연대보증을 서게 되면 모회사의 신용등급을 통해 책임준공 능력을 인정받을 수도 있습니다.

보통 일반적인 기업들은 신용등급 회사(한신평, 한기평)가 기업의 재무제표와 현금흐름, 자산을 고려해 신용등급을 평가하게 되는데 BBB+ 이상의 등급을 받아야 최소한의 재무능력을 인정받을 수 있습니다.

건물이 지어져서 담보물이 확보가 되어도 분양이 안 되는 경우 현금흐름이 막혀 대출을 상환하지 못하는 상황이 발생할 수 있습니다. 당연히 돈을 빌려준 대주단 입장에서는 분양 리스크를 줄이는 방법을 모색하게 됩니다. 일반적으로 두 가지 조건을 걸어 분양률이 저조한 상황을 대비하는데요.

첫 번째로 대출 승인 조건을 제시해서 최소한 일정 수준의 청약률이 달성된 경우에 대출을 승인해줍니다. 청약은 정식 계약이 아니므로 언제든지 해지가 될 수는 있지만 대주단 입장에서는 분양성을 어느 정도 확인할 수 있는 근거가 될 수 있기 때문에 이런 대출 기표 선행조건을 제시하게 됩니다.

예를 들어, 전체 분양 매출액이 500억인데 대주단에게 빌린 돈이 250억이라면 LTV는 250억/500억 = 50%가 되므로 최소한 30~50%의 청약을 받으면 대출을 승인해준다고 기표 승인조건을 걸게 됩니다.

두 번째는 분양률 트리거 조건을 두어 일정기간 동안 예상했던 목표 분양률이 달성되지 않는 경우가 생기면 강제적인 할인분양을 통해 분양성을 높이는 방식을 제시합니다. 분양성은 분양금액과 밀접한 연관이 있기 때문에 대주단 입장에서 분양이 안 되는 기간이 장기화되는 경우 트리거를 적용하여 분양성을 좀 더 끌어올리는 방식으로 분양가를 5~10%가량 강제로 낮추게 됩니다.

간단하게 부동산 PF대출이 무엇이고 대출을 해주는 입장에서 담보물이 없는 상황에서 프로젝트의 리스크들을 어떻게 줄여나갈 수 있을지에 대해 설명해드렸는데요. 부동산 PF대출을 쉽게 이해하기 위해서는 돈을 빌리는 입장이 아니라 돈을 빌려주는 대주단으로 빙의되어 PF대출의 조건을 이해하는 것이 중요합니다.

부동산 PF대출을 쉽게 이해하려면?

역지사지 (易地思之)

PF대출 = 프로젝트 자체의 사업성을 보고 대출을 해주는 것 (미확정 담보물 상태)

→ 돈을 빌려주는 입장(대주단)에서 무엇을 믿고 빌려줄 것인가? 에 대해 입장을 바꿔놓고 생각해보시기 바랍니다.

나중에 PF대출을 활용할 일이 생기면 돈을 빌려주는 대주단의 입장이 되어서 자신을 객관적으로 판단할 수 있어야 합니다. 대주단에게 어떻게 프로젝트의 사업성을 좀 더 설득할 수 있을지 어떻게 하면 대주단이 나의 부동산 프로젝트를 신뢰할 수 있을지에 대해 고민을 해보시면 PF대출을 좀 더 쉽게 이해하실 수 있습니다.

부동산 프로젝트파이낸싱(PF) 문제로 건설업계와 금융계가 바짝 긴장하고 있습니다. 부동산 PF란 부동산 사업에서 발생할 미래 수익을 담보로 돈을 빌려 부동산을 개발하는 금융기법을 가리키는데요. 금리가 높아지고 건설 경기가 침체하면서 부동산 PF 연체율이 높아지고, 돈을 빌려준 금융기업과 보증을 서준 기업의 부실화 우려가 커지죠.

오늘 <상식 한입>에선 건설과 금융업계의 뇌관으로 지목되는 부동산 PF를 다룹니다. 사실 이번 위기에서 문제가 되는 건 부동산 PF뿐 아니라, 부동산 PF 대출채권을 유동화한 증권도 있는데요. 이 둘은 구체적으로 무엇인지, 또 어떻게 위기를 유발했는지 살펴보겠습니다.

부동산 PF가 뭐야?

🏠 프로젝트파이낸싱(Project Financing, PF)이란?: 말 그대로 어떤 사업의 계획이나 수익성을 토대로 자금을 조달하는 것을 뜻합니다. 보통의 금융(Financing)은 개인이나 기업의 신용 혹은 담보에 기초해 이뤄집니다. 주택을 담보로 돈을 빌리거나, 기업의 신용을 토대로 채권을 발행하는 게 대표적이죠. 하지만 프로젝트파이낸싱은 별다른 담보 없이, 어떤 사업으로부터 나올 미래 수익을 담보로 대출이 이뤄집니다. 건물이나 주택 같은 부동산을 개발하거나 발전소, 터널, 항만 등 사회간접자본 개발 프로젝트를 진행할 때 주로 PF를 활용합니다. 지금 당장은 담보가 없더라도, 미래에 사업이 완료되면 분양이나 사용료 수익이 발생하니 이를 담보로 돈을 빌리는 거죠. 담보가 불확실해 위험성이 높은 대출로 꼽히며, 이자도 높은 편입니다.

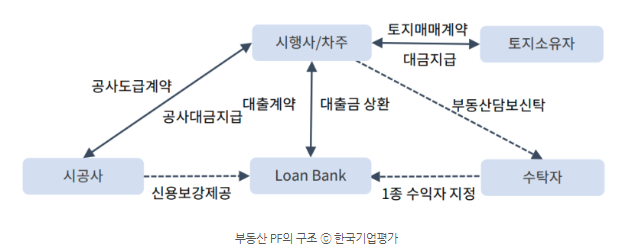

❓ 부동산 PF의 구조: 요즘 문제가 되는 부동산 PF도 이런 PF의 일종입니다. 우리나라의 부동산 PF 대출잔액은 약 130조에 달할 정도로 규모가 큰데요. 자세히 들여다보면 구조가 복잡하긴 하지만, 큰 골자는 사업의 주체인 시행사가 시공사인 건설사의 신용을 빌려 금융기관에서 돈을 조달한 후 청약 등으로 발생한 수익을 통해 원리금을 상환하는 것입니다.

부동산 PF의 구조 ⓒ 한국기업평가

🤝 시행사와 시공사: 부동산 개발 사업 주체는 크게 시행사와 시공사로 나뉩니다. 시행사는 토지 매입, 공사 계약, 자금 조달 등을 수행하며 개발 사업을 이끌어 나가고, 시공사는 시행사와 계약을 맺고 건물을 올리죠. 다만, 통상 시행사는 임시적으로 만들어지는 특수목적법인(SPC)이라 돈을 빌리기엔 신용이 부족한 편인데요. 따라서 신용등급이 높은 시공사(건설사)가 시행사의 신용을 보강해 줍니다.

💰 브릿지론과 본 PF: 일단 사업이 시작되면 시행사는 토지 매매 계약부터 체결합니다. 아직 사업이 본격화하기 전이라 PF 대출을 받기 힘든데요. 초기 자금을 마련하기 위해 PF 이전에 브릿지론이라는 고금리 초기 자금 대출을 활용합니다. 우리나라의 경우 평균 토지 구입 대금의 70~90%를 브릿지론으로 조달합니다. 이후 금융사와 본 PF 대출 계약이 체결되면 대출금을 활용해 브릿지론을 상환하는 구조입니다.

🏦 PF 대출을 해주는 금융기관: 금융기관은 투자자를 모집하거나 보유한 자금을 활용해 대출을 내어줍니다. 이렇게 돈을 빌려주는 기관을 대주 혹은 대주단이라고 하는데요. 통상 위험성이 높은 대출이기에 증권사나 저축은행, 상호금융, 캐피탈 등 제2금융권의 비중이 높습니다. 대주단 입장에선 프로젝트를 통해 원리금을 회수할 수 있는지를 따져보고 대출 승인 여부를 결정하는데요. 따라서 가장 중요하게 보는 두 가지 요소가 바로 책임준공과 분양성입니다.

🏗️ 책임준공: 대주단이 원리금을 제대로 돌려받으려면 일단 건물이 제대로 올라가서 담보물의 역할을 할 수 있어야 합니다. 그래서 대주단은 공사를 맡은 시공사에 책임준공을 약속받습니다. 책임준공이란 시공사가 건물을 계획대로 올릴 건설역량이 있다는 것(시공능력), 그리고 준공에 실패할 경우 대출금을 갚아줄 돈이 있다는 것(상환책임능력)을 증명하고 준공과 대출 상환을 약속하는 것입니다. 상환책임능력의 경우 시공사가 발행하는 회사채 등급으로 평가하며, 회사채를 발행하지 않는 시공사는 신용평가사가 매기는 신용등급으로 평가하죠. 이번에 위기에 빠진 태영건설도 이 책임준공 확약 금액이 3조 5천억 원에 달합니다.

💸 분양성: 건물이 기한 내에 올라갔더라도 분양이 되지 않는다면 대주단은 원리금을 돌려받기 어렵습니다. 따라서 대출 전 프로젝트의 분양성이 충분한지를 확인하는데요. 먼저 대주단은 시행사에 청약을 미리 실시할 것을 요구합니다. 이 청약률이 얼마나 나오는지를 보고 대출 여부를 결정하는 거죠. 또, 대주단은 할인분양트리거를 걸어두는데요. 분양을 시작한 후 일정 기간이 지나도 분양률이 목표에 못 미치면 강제로 정해진 할인율을 적용해 분양가를 깎는 것이죠. 이 두 가지 장치를 활용해 대주단은 프로젝트에서 충분한 현금흐름을 확보하고자 합니다.

부동산 PF 유동화란?

이번 태영건설 부도 위기에서 문제가 된 것은 부동산 PF만이 아니었습니다. 부동산 PF 대출채권을 유동화한 ABCP도 건설기업의 부실 요인으로 떠올랐는데요. 대출채권을 유동화한다는 것이 무엇인지, 그리고 이게 왜 위기의 원인이 됐는지 살펴보겠습니다.

💵 자산유동화란?: 시행사에 돈을 빌려준 대주단은 만기가 돌아오는 수 년간 차용증(대출채권)을 들고 있어야 합니다. 건물이 예정대로 준공되면 원리금을 받을 수 있는 건데요. 하지만 수십, 수백억 원짜리 채권을 몇 년간 들고 있자니 답답하기 그지없습니다. 그래서 이 대출채권을 잘게 쪼개서 기관이나 개인 투자자에게 판매하고 현금을 확보하는데, 이를 자산(대출채권) 유동화라고 하며, 쪼개진 채권을 유동화증권(Asset-Backed Securities, ABS)이라고 합니다. 이 과정에서 대주단은 자산유동화를 위한 특수목적법인(SPC)을 설립하는데요. 하지만 신용이 부족한 SPC로는 증권 발행이 어렵기에 시공사와 증권사의 신용보강을 거치게 됩니다. ABS를 사는 투자자 입장에선 '만약 PF 대출채권이 부도날 경우 증권사나 시공사가 ABS를 대신 사준다'라는 약속을 받는 것이죠.

'25년 6월 26일까지 주가 32,000원 이하일 경우 전동규 대표 개인이 주가 - 풋옵션 차액을 현금으로 갚아야함 <- 사채발행 통한 롤오버?

32,000원 이상일 경우 유통 주식으로 편입 가능성 高

24년 5월 28일 전동규 소유 및 풋옵션 체결 외 414만주 중 썬플라워 홀딩스 보유 1,742,488주 블록딜 되었으며, 풋옵션 체결된 10,638,293주 중 127,035주 5월 27일 및 28일 양일에 거쳐 장내 매도됨

이에 아직 매도 가능한 전환 사채 물량 2,395,441주 시장에 남아 있어 리스크로 존재

장내 매도된 풋옵션 127,035주는 7차 전환사채 발행 물량이 나온 것으로 7차 전환 사채 700억 中 대신에스케이에스이노베이션제2호사모투자합자회사와 에스케이에스한국투자제1호사모투자합자회사는 각각 425,561주 보유하였으나, 금번 장내 매도를 통해 각각 76,978주, 50,057주 매도하여 348,553주, 375,474주 보유하게 됨 -> 에스케이투자펀드 성격 상 매도 의지 높을 것으로 판단되고 매도 가능 물량 많아 오버행 이슈 지속 존재

24년 7월 17일 썬플라워홀딩스 보유 2,004,047주 중 451,138 장내 매도하여 1,552,909주 잔여, Rivendell Investments 229,482주 + 227,239주 中 51,743주 장내 매도하여 404,978주 잔여, 에스케이에스공동투자2021사모투자 합자회사 2,553,191주 中 28,500주 장내 매도하여 2,524,691주 잔여

이번 전환 물량은 기존 발행한 전환사채 물량 1,889만주 중 94%에 해당하는 1,770만주이며 5월 17일부터 상장 예정

대표이사 및 풋옵션 물량 제외 시장 오버행 이슈가 존재하는 414만주 전환가액은 14,500원으로 '24년5월15일 시총 대비 75% 수익

https://blog.naver.com/inee1104/223133370586https://m.blog.naver.com/hism16a1/223434527413https://blog.naver.com/startingpoint1/223467866106 , https://blog.naver.com/startingpoint1/22343613722624년 7월 17일 주식 세부변동 내역, https://dart.fss.or.kr/dsaf001/main.do?rcpNo=20240717000405

'24년6월18일 현대차증권 70억원・BNK증권 130억원・하이투자증권 20억원 총 220원 주식담보대출로 차입

담보유지비율은 현대차증권과 하이투자증권이 200%, BNK증권은 180%로 평균 140% 대비 높게 설정

인적분할 실패하였으나 ESS 부분 Spin-off하려는 의도 발각

서진시스템 : 서진에너지 시스템 = 85:15로, ESS 시장 성장 동력 위해 서진시스템에 투자해도 향후 15% 비율만 ESS 사업 비중으로 가져가게 될 우려

Updated April 26, 2024, 4:12 pm EDT / Original April 26, 2024, 2:30 am EDT

When customers walk into Ali’s Chicken & Waffles in San Diego hungry for a buttermilk fried chicken sandwich or a Surf n’ Bird burrito, they can place an order with a cashier or on a tablet. Owner Genemo Ali, who opened his first restaurant in 2020, finds the hybrid model has helped increase the number of orders processed and boost customer engagement. If a cashier is tied up, a cook doesn’t have to leave the kitchen to assist customers.

When customers walk into Ali’s Chicken & Waffles in San Diego hungry for a buttermilk fried chicken sandwich or a Surf n’ Bird burrito, they can place an order with a cashier or on a tablet. Owner Genemo Ali, who opened his first restaurant in 2020, finds the hybrid model has helped increase the number of orders processed and boost customer engagement. If a cashier is tied up, a cook doesn’t have to leave the kitchen to assist customers.

Ali estimates that the system has helped him serve at least twice as many customers as cashier service alone. “Technology doesn’t take away the job; it just enhances the quality,” he says.

The investments in tools, equipment, and technology that businesses like Ali’s have made in the past few years are starting to pay dividends across the U.S. economy, with workers nationwide producing more for each hour worked. That surge in productivity has helped underpin the U.S. economy’s extraordinary expansion, and output enhancements could shield the economy as it shakes off the last pandemic-era restraints.

Although the seeds of the recent productivity boom were planted before the Covid-19 outbreak, the pandemic was a watershed moment for businesses and consumers, demanding that both find new ways to adapt to changed circumstances. It pushed businesses like Ali’s to speed up operations with more technological assists, retailers to beef up online shopping tools, and white-collar workers to embrace remote and hybrid work models that helped connect colleagues across cities, states, and countries. Many of those transformations improved workplace productivity and helped corporations boost profits, even during turbulent times.

As a result, the economy continued to post solid growth, defying predictions of an imminent recession and upending the Federal Reserve’s interest-rate-cutting plans. While many economists expect growth to cool—and it has, with the economy expanding at a disappointing 1.6% annualized rate in the first quarter—increased labor productivity could help to insulate the U.S. from stagnation.

“There are reasons to be optimistic that we’re at the start of something more substantive,” says Mark Zandi, chief economist at Moody’s Analytics.

Measuring Productivity

Labor productivity is the measure of how quickly and efficiently workers generate goods and services. It is a volatile data set that the Bureau of Labor Statistics calculates by dividing real output by total hours worked. The BLS releases an estimate every quarter.

Productivity growth typically reflects capital improvements, such as tools or equipment, that increase labor quality and provide workers with the ability to improve capacity. Ultimately, gains in productivity lead to improved living standards and greater consumption.

Labor productivity grew at an average annual rate of 1.6% from 2020 to 2023 when smoothing out pandemic volatility, according to the BLS. That’s up from a decadelong average of 1.2% growth in the 2010s, but below the 2.8% average annual growth rate seen during the last big productivity boom, from 1995 to 2005, which was largely attributed to the proliferation of computers and the internet, andincreased business competition.

Total factor productivity, another measure that includes both labor and capital outlays, also showed growth last year, albeit a smaller uptick of 0.7%.The government reports TPF dataannually.

Economists tend to study labor productivity on a long time horizon, comparing decades rather than quarterly shifts. But the uptick in worker efficiency recorded in the second half of 2023 was so strong that it’s worth examining. Labor productivity increased by an estimated 3.3% in last year’s fourth quarter, kindling optimism among many economists that the U.S. is beginning to shift to structurally higher-trend growth in the coming years

[Editors’ note: The Bureau of Labor Statistics issued a press release on April 26 in the afternoon indicating it was correcting its previously published labor productivity data for first-quarter 2019 through fourth-quarter 2023 due to a computation error that distorted the hours-worked ratios. The BLS issued revised estimates of quarterly and annual labor productivity data, and will issue final figures on May 2. Fourth-quarter labor productivity previously was reported as 3.2%. This story and related charts have been updated to reflect the initial corrected estimates.]

Increases in real outputs played a critical role in helping the U.S. avoid a much-anticipated recession last year, says Edward Yardeni, president of Yardeni Research. “Productivity is like the economy’s fairy dust,” he says.

Productivity developments are of particular interest to Federal Reserve officials, as the faster pace of wage growth might have been more inflationary without the labor efficiencies. The relationship of productivity to inflation and economic growth probably will factor into the Fed’s rate-cut decisions this year. The central bank’s policy-setting committee will meet again on April 30 and May 1.

Behind the Gains

One of the biggest drivers of increased productivity has been public and private investment. Five of the largest technology companies—AlphabetGOOGL10.22%,Amazon.com AMZN3.43%,AppleAAPL-0.35%,Meta PlatformsMETA0.43%, andMicrosoftMSFT1.82%—invested $400 billion last year, half directed to research and development, according to Olivia White, director of the McKinsey’s Global Institute, the firm’s business and economics research arm. That’s up from roughly $71 billion in 2017, and $127 billion in 2020.

Investments, particularly in tech, historically have been a significant driver of productivity growth. When investment fell off after the financial crisis of 2008-09, productivity growth in the U.S. decelerated. “Investment is important, and we’re seeing it coming in again,” White says.

Other factors have played a role in driving productivity growth, such as changing labor-market dynamics and new business formation. On the labor front, the U.S. economy has reaped the benefits of low unemployment and the so-called Great Resignation, which led to the turnover of nearly 100 million jobs from 2021 to 2022. Ultimately, that helped to improve the allocation of people and talent.

Tight labor markets offer workers opportunities to move into more-productive and higher-paying jobs. They also force employers to do more with fewer workers. Employee turnover can be disruptive, but the U.S. quit rate has eased substantially since 2022, falling to 2.2% as of February from a peak of 3% two years earlier, and a prepandemic rate of 2.3%. Longer tenure can add to workers’ productivity.

“The excess supply, especially of labor, went away and forced companies to think about capital-for-labor substitution,” says Jason Draho, chair of the U.S. investment strategy committee at UBS.

This shift typically is a good indicator of productivity gains two to three years down the road, Draho says, because companies have no choice but to equip existing workers with better tools, more capital, and technology.Starbucks, for example, has invested heavily in digitizing its supply chain and store operations since 2019. The companyreported in Novemberthat the changes helped lead to 30% labor productivity growth.

Working from home probably had an impact, as well, pulling more Americans into the workforce who traditionally have recorded lower participation and productivity rates. Even before the pandemic, performance among call-center employees working from home improved by 13%, according toresearchfrom Nick Bloom, a professor of economics at Stanford University and an expert on remote work.

Bloomestimatesthat well-organized hybrid workers typically see3% to 5% more productivity, while Goldman Sachsresearchhas found that remote-work productivity gains generally have been about 3%.

New business formation might be one of the biggest drivers of recent productivity growth, and has helped set the U.S. economy up for continued success. Americans filed 17.3 million new business applications from January 2021 to March 2024, according to data from the U.S. Census Bureau. In the past three years, monthly applications have nearly doubled relative to prepandemic levels going back to 2004.

The uptick is significant because new businesses tend to have higher productivity, probably reflective of the fact that they launch with the newest technologies and workers with up-to-date skills, according to Lucia Foster, chief economist at the U.S. Census Bureau. While new business applications haveslowed in recent months, the productivity gains of new entrants are far from over.

“All those businesses forming would generally mean more innovation, more entrepreneurship, more technological change, and higher productivity growth,” Moody’s Zandi says. “We’re four years into this surge in business formation, and companies are becoming more stable and ingrained in the economy—and probably starting to generate those productivity gains.”

Other Growth Engines

While labor productivity might help to drive and stabilize the recent economic growth, broader labor-market gains have been a significant contributor to the economy’s resilience. Although the U.S. job market is gradually normalizing after three years of outsize growth, payroll gains remain healthy, layoffs and unemployment are low, and wages rose 4.1% year over year in March, outpacing the rate of inflation. “You’re not seeing cracks” in the labor market, says Sarah House, a senior economist at Wells Fargo.

The U.S. added303,000 jobsin March, surpassing both expectations and prepandemic payroll growth. Given demographic trends, the rate of employment growth should have slowed as older workers aged out of the labor market. But immigration has driven faster population growth and is adding to the nation’s workforce.

Immigration could also help to sustain new business formation and productivity. Historically, immigration has led to greater productivity over time, in part because immigrants tend to start companies at a higher rate than the native population, Zandi says.

While demand for workers has cooled in some parts of the economy, small businesses are still hiring. About56% of small-business ownersreported that they hired or tried to hire workers in March, the same percentage as in February, according to data from the National Federation of Independent Business.

Skilled workers remain in demand. Four in 10 private companies surveyed by Deloitte in February 2024 said their top strategy to boost productivity is to hire qualified or skilled talent.

“Businesses are waking up to some of the demographic challenges that we have, and they’re thinking about labor a little bit differently,” says Wells Fargo’s House, noting that many employers now value workers more than they did before the Covid pandemic.

That could help to cushion the labor market from some of the negative effects of higher interest rates and quell employers’ impulse to cut workers if the market turns down. Limiting layoffs would also bolster consumers’ finances and spur spending. Total retail salesjumped 0.7% in March, while the data for February were revised higher.

Last year’s boom in consumer spending, which accounts for about 70% of economic activity, helped lift gross domestic product by2.5%, adjusted for inflation. Demand remains fairly healthy, although consumers are pulling back from the pandemic-era glut, based on the latest GDP report, which came in well below consensus expectations. The report is the first of three GDP estimates, and is based on data subject to revisions.

Des Moines, Iowa–based business owner Mike Draper has been a beneficiary of the growth in consumer spending. Draper opened the first of his Raygun printing, design, and clothing stores in 2005 and has since expanded to nine stores and a production facility, with a tenth store opening this summer.

“The hardest thing about the economy during the past two years was hearing people worry about the economy,” Draper says, adding that recession predictions don’t square with what he’s seeing. While spending patterns have become a bit less predictable, he says, he hasn’t seen consumers pulling back yet.

The pandemic forced Raygun to “speed up content release,” says Draper, who is optimistic about the outlook for the company and the economy.

“America is just on this unbelievable winning streak that started with inventing a vaccine, and it has gone on from there,” he says. “I can’t wrap my head around what people are so bummed out about.”

Reasons for Optimism

The U.S. probably has wrung out by now the majority of the productivity gains from pandemic-era business upgrades and workforce dynamics. But that needn’t be the end of the story. Continued public and private investment could provide tailwinds, especially when paired with emerging technologies such as generative artificial intelligence.

Government-funded research and development in nondefense sectors historically has improved productivity, and recent legislation, including the Chips Act and the Inflation Reduction Act, probably will help to boost U.S. productivity in the medium and long term, says Andrew Fieldhouse, an economics professor at the Mays Business School at Texas A&M University.

Fieldhouse’s research shows that the effects of government R&D boost productivity for eight to 15 years after an increase in appropriations. In the past two fiscal years that ended on Sept. 30, Congress hasn’t come close to appropriating the full amount authorized by Chips. That legislation could have an impact on productivity growth for at least the next five to 10 years, he figures.

Additionally,real manufacturing-construction spendingdoubled from 2022 to early 2023, coinciding with healthy growth in private, nonresidential fixed investment. “All of this should be giving workers more factories and more equipment to work with, boosting labor productivity,” Fieldhouse says.

Innovation holds even greater potential for increasing U.S. labor productivity. Goldman Sachs projects that the impact of AI could boost GDP growth by up to 2.3% by 2034, although adoption of the technology is still in its infancy.

Only about3.9% of businesses nationwidehave used AI—including machine learning, natural language processing, virtual agents, and voice recognition—to produce goods or services, according to the Census Bureau’s November 2023 Business Trends and Outlook Survey. Still, about 87% of private businessesrecently surveyed by Deloitteexpect AI to deliver increases in their labor productivity in the next three years.

Other recent innovations also could improve productivity, including mRNA vaccines, green transition technologies, cloud computing, robotics, and even advances in material science. “We can get myopically focused on generative AI, but it surely shouldn’t be the only technology that’s boosting productivity in the future,” says McKinsey’s White.

It is unclear how transformative or ubiquitous any of these advances will be, and estimates of their potential impact vary. Nor is it reasonable to expect that productivity will grow in a linear fashion, increasing in every quarter. But just as the U.S. economy’s strength has stunned almost everyone, from economists and policymakers to investors, productivity could prove surprisingly robust in the years ahead.