Updated April 26, 2024, 4:12 pm EDT / Original April 26, 2024, 2:30 am EDT

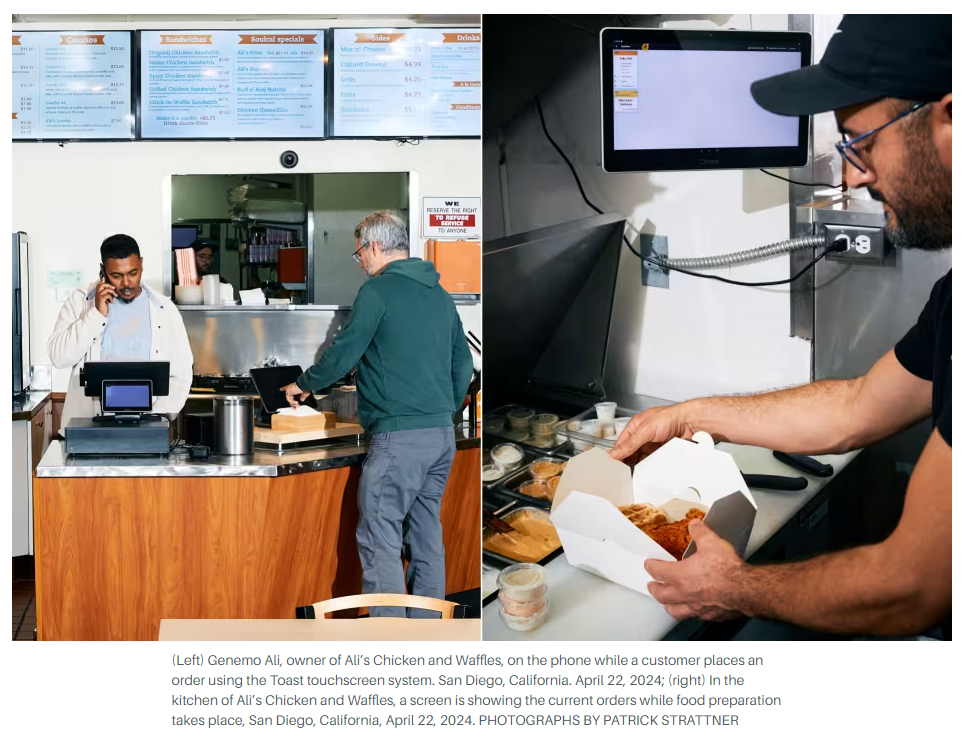

When customers walk into Ali’s Chicken & Waffles in San Diego hungry for a buttermilk fried chicken sandwich or a Surf n’ Bird burrito, they can place an order with a cashier or on a tablet. Owner Genemo Ali, who opened his first restaurant in 2020, finds the hybrid model has helped increase the number of orders processed and boost customer engagement. If a cashier is tied up, a cook doesn’t have to leave the kitchen to assist customers.

When customers walk into Ali’s Chicken & Waffles in San Diego hungry for a buttermilk fried chicken sandwich or a Surf n’ Bird burrito, they can place an order with a cashier or on a tablet. Owner Genemo Ali, who opened his first restaurant in 2020, finds the hybrid model has helped increase the number of orders processed and boost customer engagement. If a cashier is tied up, a cook doesn’t have to leave the kitchen to assist customers.

Ali estimates that the system has helped him serve at least twice as many customers as cashier service alone. “Technology doesn’t take away the job; it just enhances the quality,” he says.

The investments in tools, equipment, and technology that businesses like Ali’s have made in the past few years are starting to pay dividends across the U.S. economy, with workers nationwide producing more for each hour worked. That surge in productivity has helped underpin the U.S. economy’s extraordinary expansion, and output enhancements could shield the economy as it shakes off the last pandemic-era restraints.

Although the seeds of the recent productivity boom were planted before the Covid-19 outbreak, the pandemic was a watershed moment for businesses and consumers, demanding that both find new ways to adapt to changed circumstances. It pushed businesses like Ali’s to speed up operations with more technological assists, retailers to beef up online shopping tools, and white-collar workers to embrace remote and hybrid work models that helped connect colleagues across cities, states, and countries. Many of those transformations improved workplace productivity and helped corporations boost profits, even during turbulent times.

As a result, the economy continued to post solid growth, defying predictions of an imminent recession and upending the Federal Reserve’s interest-rate-cutting plans. While many economists expect growth to cool—and it has, with the economy expanding at a disappointing 1.6% annualized rate in the first quarter—increased labor productivity could help to insulate the U.S. from stagnation.

“There are reasons to be optimistic that we’re at the start of something more substantive,” says Mark Zandi, chief economist at Moody’s Analytics.

Measuring Productivity

Labor productivity is the measure of how quickly and efficiently workers generate goods and services. It is a volatile data set that the Bureau of Labor Statistics calculates by dividing real output by total hours worked. The BLS releases an estimate every quarter.

Productivity growth typically reflects capital improvements, such as tools or equipment, that increase labor quality and provide workers with the ability to improve capacity. Ultimately, gains in productivity lead to improved living standards and greater consumption.

Labor productivity grew at an average annual rate of 1.6% from 2020 to 2023 when smoothing out pandemic volatility, according to the BLS. That’s up from a decadelong average of 1.2% growth in the 2010s, but below the 2.8% average annual growth rate seen during the last big productivity boom, from 1995 to 2005, which was largely attributed to the proliferation of computers and the internet, andincreased business competition.

Total factor productivity, another measure that includes both labor and capital outlays, also showed growth last year, albeit a smaller uptick of 0.7%.The government reports TPF dataannually.

Economists tend to study labor productivity on a long time horizon, comparing decades rather than quarterly shifts. But the uptick in worker efficiency recorded in the second half of 2023 was so strong that it’s worth examining. Labor productivity increased by an estimated 3.3% in last year’s fourth quarter, kindling optimism among many economists that the U.S. is beginning to shift to structurally higher-trend growth in the coming years

[Editors’ note: The Bureau of Labor Statistics issued a press release on April 26 in the afternoon indicating it was correcting its previously published labor productivity data for first-quarter 2019 through fourth-quarter 2023 due to a computation error that distorted the hours-worked ratios. The BLS issued revised estimates of quarterly and annual labor productivity data, and will issue final figures on May 2. Fourth-quarter labor productivity previously was reported as 3.2%. This story and related charts have been updated to reflect the initial corrected estimates.]

Increases in real outputs played a critical role in helping the U.S. avoid a much-anticipated recession last year, says Edward Yardeni, president of Yardeni Research. “Productivity is like the economy’s fairy dust,” he says.

Productivity developments are of particular interest to Federal Reserve officials, as the faster pace of wage growth might have been more inflationary without the labor efficiencies. The relationship of productivity to inflation and economic growth probably will factor into the Fed’s rate-cut decisions this year. The central bank’s policy-setting committee will meet again on April 30 and May 1.

Behind the Gains

One of the biggest drivers of increased productivity has been public and private investment. Five of the largest technology companies—AlphabetGOOGL10.22%,Amazon.com AMZN3.43%,AppleAAPL-0.35%,Meta PlatformsMETA0.43%, andMicrosoftMSFT1.82%—invested $400 billion last year, half directed to research and development, according to Olivia White, director of the McKinsey’s Global Institute, the firm’s business and economics research arm. That’s up from roughly $71 billion in 2017, and $127 billion in 2020.

Investments, particularly in tech, historically have been a significant driver of productivity growth. When investment fell off after the financial crisis of 2008-09, productivity growth in the U.S. decelerated. “Investment is important, and we’re seeing it coming in again,” White says.

Other factors have played a role in driving productivity growth, such as changing labor-market dynamics and new business formation. On the labor front, the U.S. economy has reaped the benefits of low unemployment and the so-called Great Resignation, which led to the turnover of nearly 100 million jobs from 2021 to 2022. Ultimately, that helped to improve the allocation of people and talent.

Tight labor markets offer workers opportunities to move into more-productive and higher-paying jobs. They also force employers to do more with fewer workers. Employee turnover can be disruptive, but the U.S. quit rate has eased substantially since 2022, falling to 2.2% as of February from a peak of 3% two years earlier, and a prepandemic rate of 2.3%. Longer tenure can add to workers’ productivity.

“The excess supply, especially of labor, went away and forced companies to think about capital-for-labor substitution,” says Jason Draho, chair of the U.S. investment strategy committee at UBS.

This shift typically is a good indicator of productivity gains two to three years down the road, Draho says, because companies have no choice but to equip existing workers with better tools, more capital, and technology.Starbucks, for example, has invested heavily in digitizing its supply chain and store operations since 2019. The companyreported in Novemberthat the changes helped lead to 30% labor productivity growth.

Working from home probably had an impact, as well, pulling more Americans into the workforce who traditionally have recorded lower participation and productivity rates. Even before the pandemic, performance among call-center employees working from home improved by 13%, according toresearchfrom Nick Bloom, a professor of economics at Stanford University and an expert on remote work.

Bloomestimatesthat well-organized hybrid workers typically see3% to 5% more productivity, while Goldman Sachsresearchhas found that remote-work productivity gains generally have been about 3%.

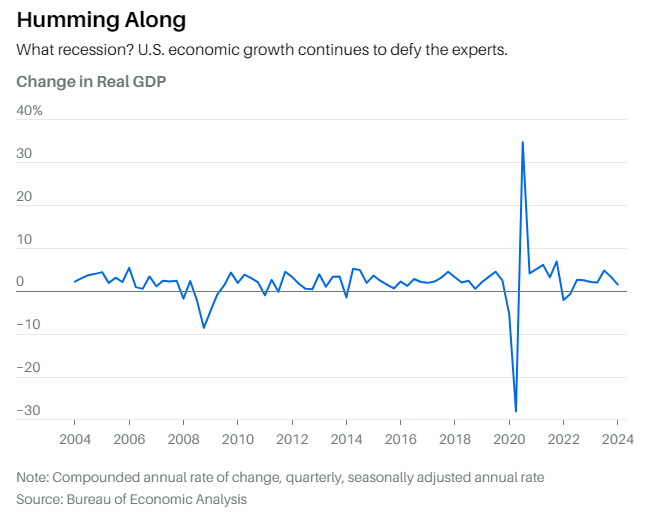

New business formation might be one of the biggest drivers of recent productivity growth, and has helped set the U.S. economy up for continued success. Americans filed 17.3 million new business applications from January 2021 to March 2024, according to data from the U.S. Census Bureau. In the past three years, monthly applications have nearly doubled relative to prepandemic levels going back to 2004.

The uptick is significant because new businesses tend to have higher productivity, probably reflective of the fact that they launch with the newest technologies and workers with up-to-date skills, according to Lucia Foster, chief economist at the U.S. Census Bureau. While new business applications haveslowed in recent months, the productivity gains of new entrants are far from over.

“All those businesses forming would generally mean more innovation, more entrepreneurship, more technological change, and higher productivity growth,” Moody’s Zandi says. “We’re four years into this surge in business formation, and companies are becoming more stable and ingrained in the economy—and probably starting to generate those productivity gains.”

Other Growth Engines

While labor productivity might help to drive and stabilize the recent economic growth, broader labor-market gains have been a significant contributor to the economy’s resilience. Although the U.S. job market is gradually normalizing after three years of outsize growth, payroll gains remain healthy, layoffs and unemployment are low, and wages rose 4.1% year over year in March, outpacing the rate of inflation. “You’re not seeing cracks” in the labor market, says Sarah House, a senior economist at Wells Fargo.

The U.S. added303,000 jobsin March, surpassing both expectations and prepandemic payroll growth. Given demographic trends, the rate of employment growth should have slowed as older workers aged out of the labor market. But immigration has driven faster population growth and is adding to the nation’s workforce.

Immigration could also help to sustain new business formation and productivity. Historically, immigration has led to greater productivity over time, in part because immigrants tend to start companies at a higher rate than the native population, Zandi says.

While demand for workers has cooled in some parts of the economy, small businesses are still hiring. About56% of small-business ownersreported that they hired or tried to hire workers in March, the same percentage as in February, according to data from the National Federation of Independent Business.

Skilled workers remain in demand. Four in 10 private companies surveyed by Deloitte in February 2024 said their top strategy to boost productivity is to hire qualified or skilled talent.

“Businesses are waking up to some of the demographic challenges that we have, and they’re thinking about labor a little bit differently,” says Wells Fargo’s House, noting that many employers now value workers more than they did before the Covid pandemic.

That could help to cushion the labor market from some of the negative effects of higher interest rates and quell employers’ impulse to cut workers if the market turns down. Limiting layoffs would also bolster consumers’ finances and spur spending. Total retail salesjumped 0.7% in March, while the data for February were revised higher.

Last year’s boom in consumer spending, which accounts for about 70% of economic activity, helped lift gross domestic product by2.5%, adjusted for inflation. Demand remains fairly healthy, although consumers are pulling back from the pandemic-era glut, based on the latest GDP report, which came in well below consensus expectations. The report is the first of three GDP estimates, and is based on data subject to revisions.

Des Moines, Iowa–based business owner Mike Draper has been a beneficiary of the growth in consumer spending. Draper opened the first of his Raygun printing, design, and clothing stores in 2005 and has since expanded to nine stores and a production facility, with a tenth store opening this summer.

“The hardest thing about the economy during the past two years was hearing people worry about the economy,” Draper says, adding that recession predictions don’t square with what he’s seeing. While spending patterns have become a bit less predictable, he says, he hasn’t seen consumers pulling back yet.

The pandemic forced Raygun to “speed up content release,” says Draper, who is optimistic about the outlook for the company and the economy.

“America is just on this unbelievable winning streak that started with inventing a vaccine, and it has gone on from there,” he says. “I can’t wrap my head around what people are so bummed out about.”

Reasons for Optimism

The U.S. probably has wrung out by now the majority of the productivity gains from pandemic-era business upgrades and workforce dynamics. But that needn’t be the end of the story. Continued public and private investment could provide tailwinds, especially when paired with emerging technologies such as generative artificial intelligence.

Government-funded research and development in nondefense sectors historically has improved productivity, and recent legislation, including the Chips Act and the Inflation Reduction Act, probably will help to boost U.S. productivity in the medium and long term, says Andrew Fieldhouse, an economics professor at the Mays Business School at Texas A&M University.

Fieldhouse’s research shows that the effects of government R&D boost productivity for eight to 15 years after an increase in appropriations. In the past two fiscal years that ended on Sept. 30, Congress hasn’t come close to appropriating the full amount authorized by Chips. That legislation could have an impact on productivity growth for at least the next five to 10 years, he figures.

Additionally,real manufacturing-construction spendingdoubled from 2022 to early 2023, coinciding with healthy growth in private, nonresidential fixed investment. “All of this should be giving workers more factories and more equipment to work with, boosting labor productivity,” Fieldhouse says.

Innovation holds even greater potential for increasing U.S. labor productivity. Goldman Sachs projects that the impact of AI could boost GDP growth by up to 2.3% by 2034, although adoption of the technology is still in its infancy.

Only about3.9% of businesses nationwidehave used AI—including machine learning, natural language processing, virtual agents, and voice recognition—to produce goods or services, according to the Census Bureau’s November 2023 Business Trends and Outlook Survey. Still, about 87% of private businessesrecently surveyed by Deloitteexpect AI to deliver increases in their labor productivity in the next three years.

Other recent innovations also could improve productivity, including mRNA vaccines, green transition technologies, cloud computing, robotics, and even advances in material science. “We can get myopically focused on generative AI, but it surely shouldn’t be the only technology that’s boosting productivity in the future,” says McKinsey’s White.

It is unclear how transformative or ubiquitous any of these advances will be, and estimates of their potential impact vary. Nor is it reasonable to expect that productivity will grow in a linear fashion, increasing in every quarter. But just as the U.S. economy’s strength has stunned almost everyone, from economists and policymakers to investors, productivity could prove surprisingly robust in the years ahead.

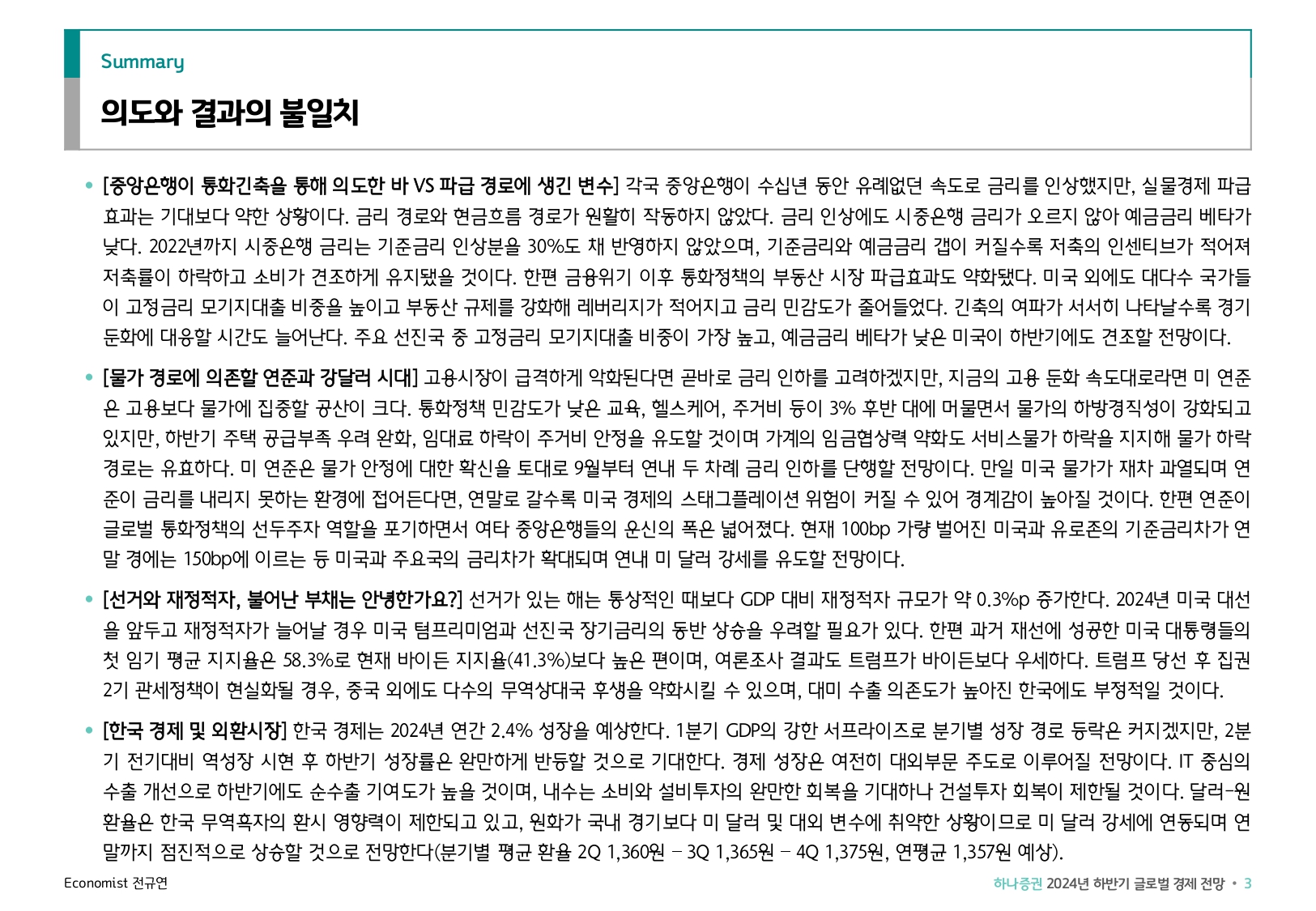

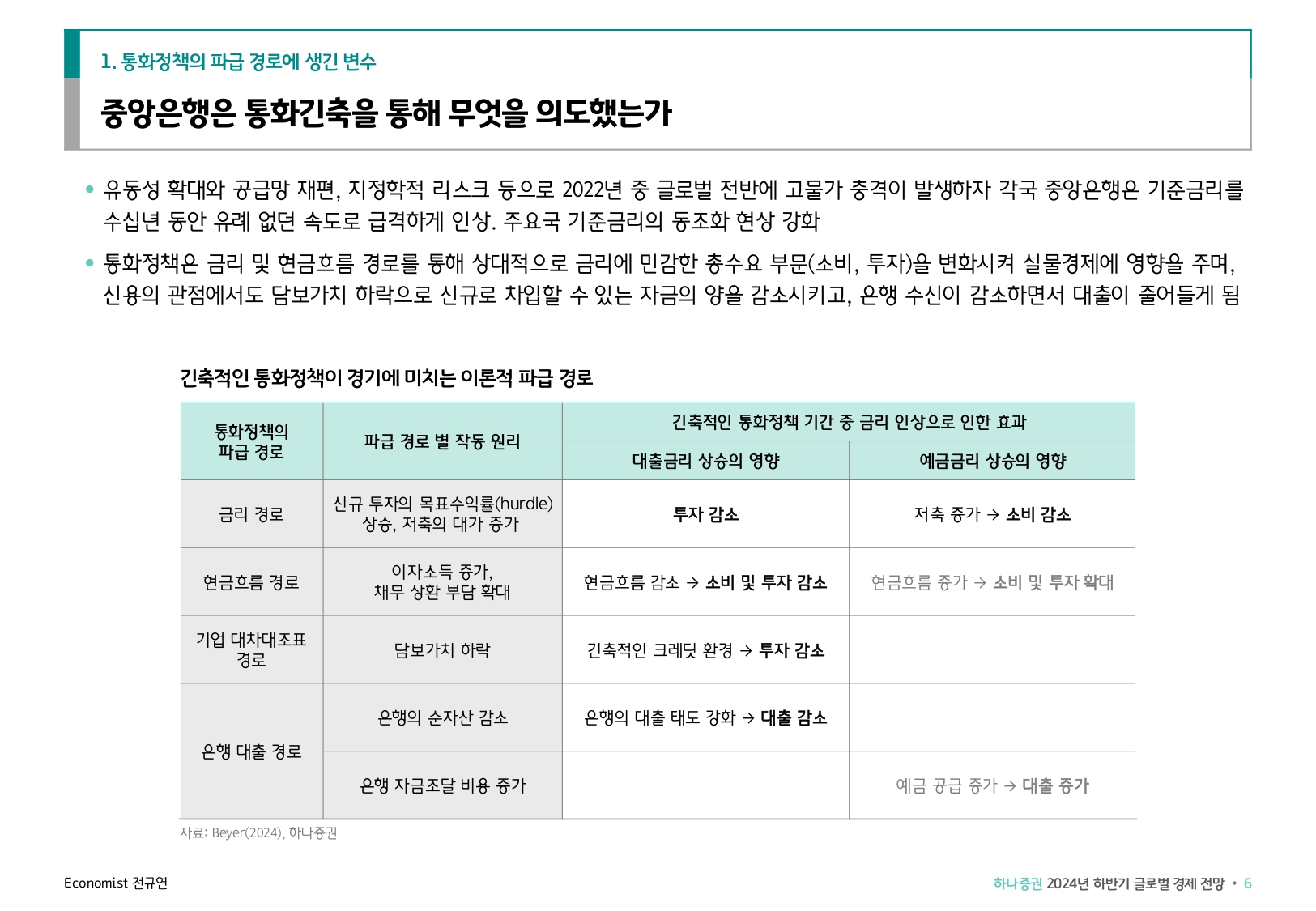

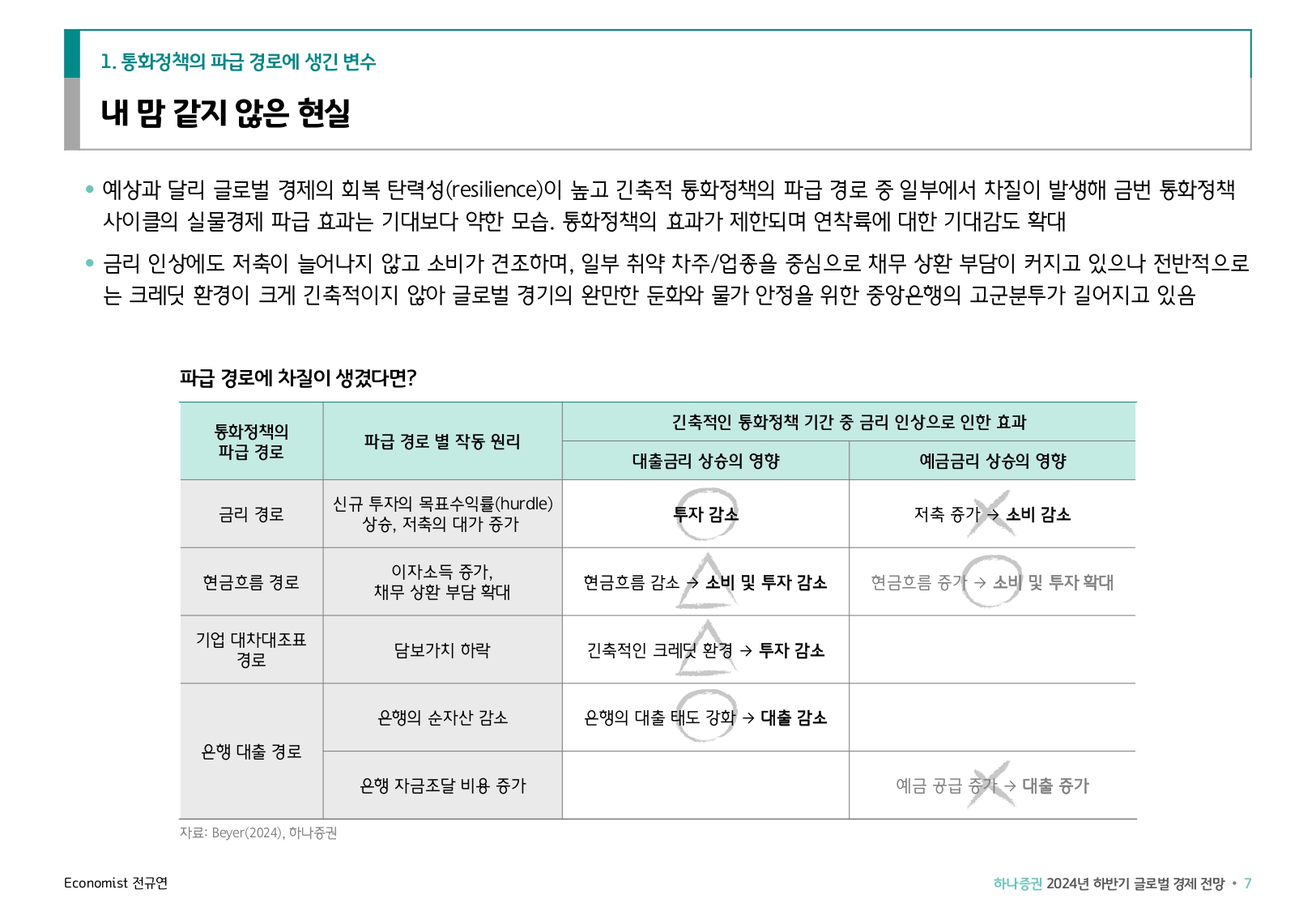

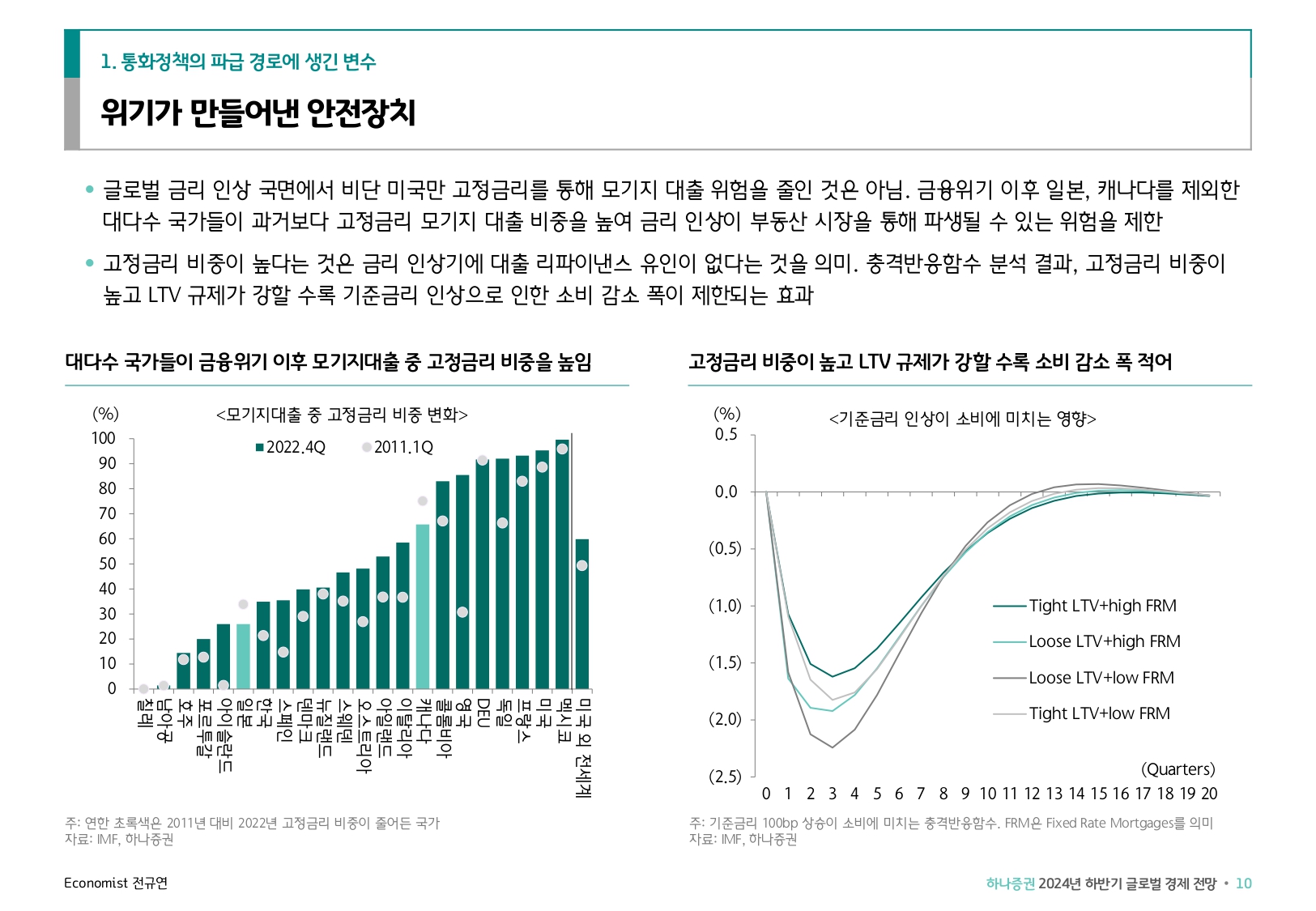

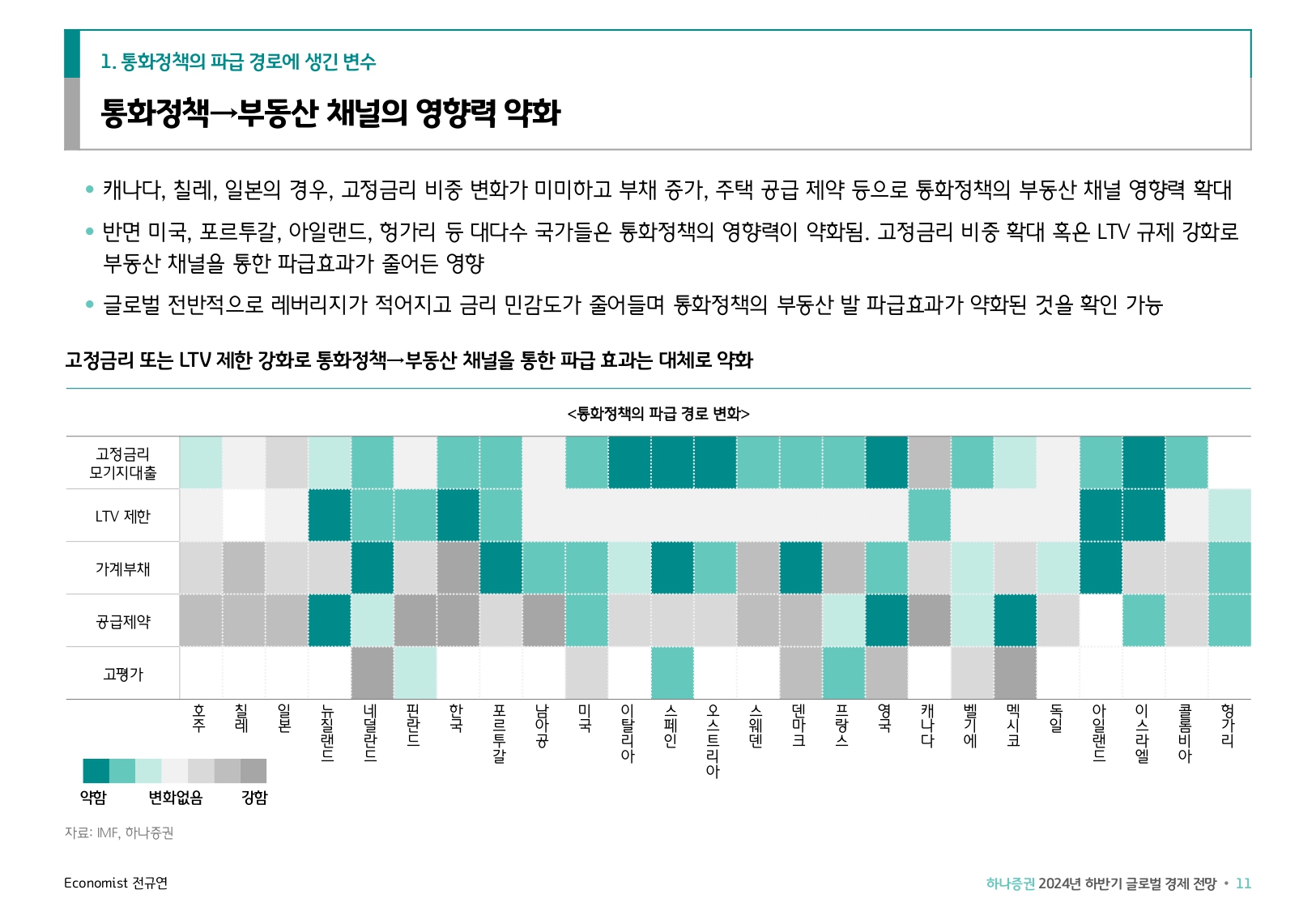

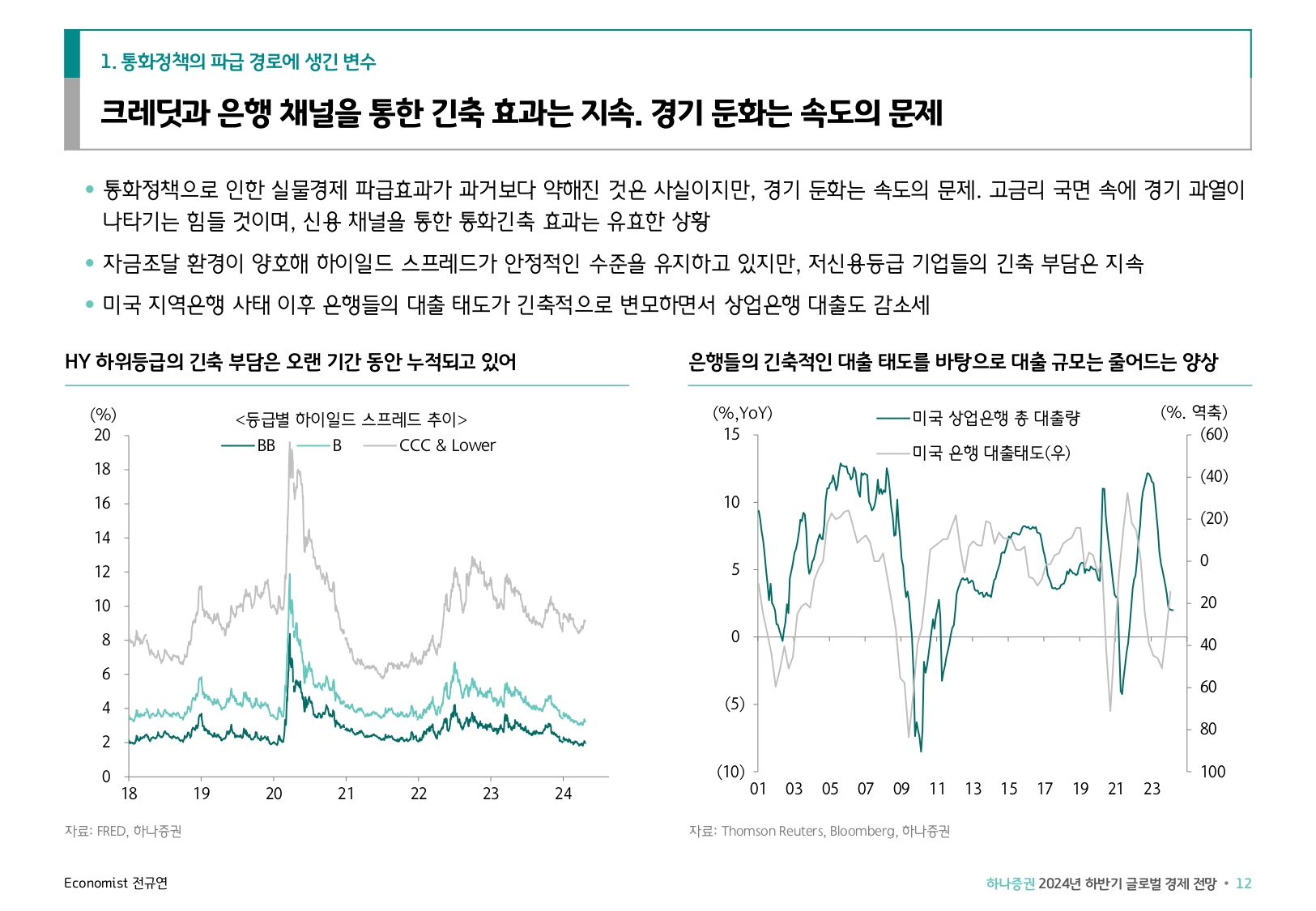

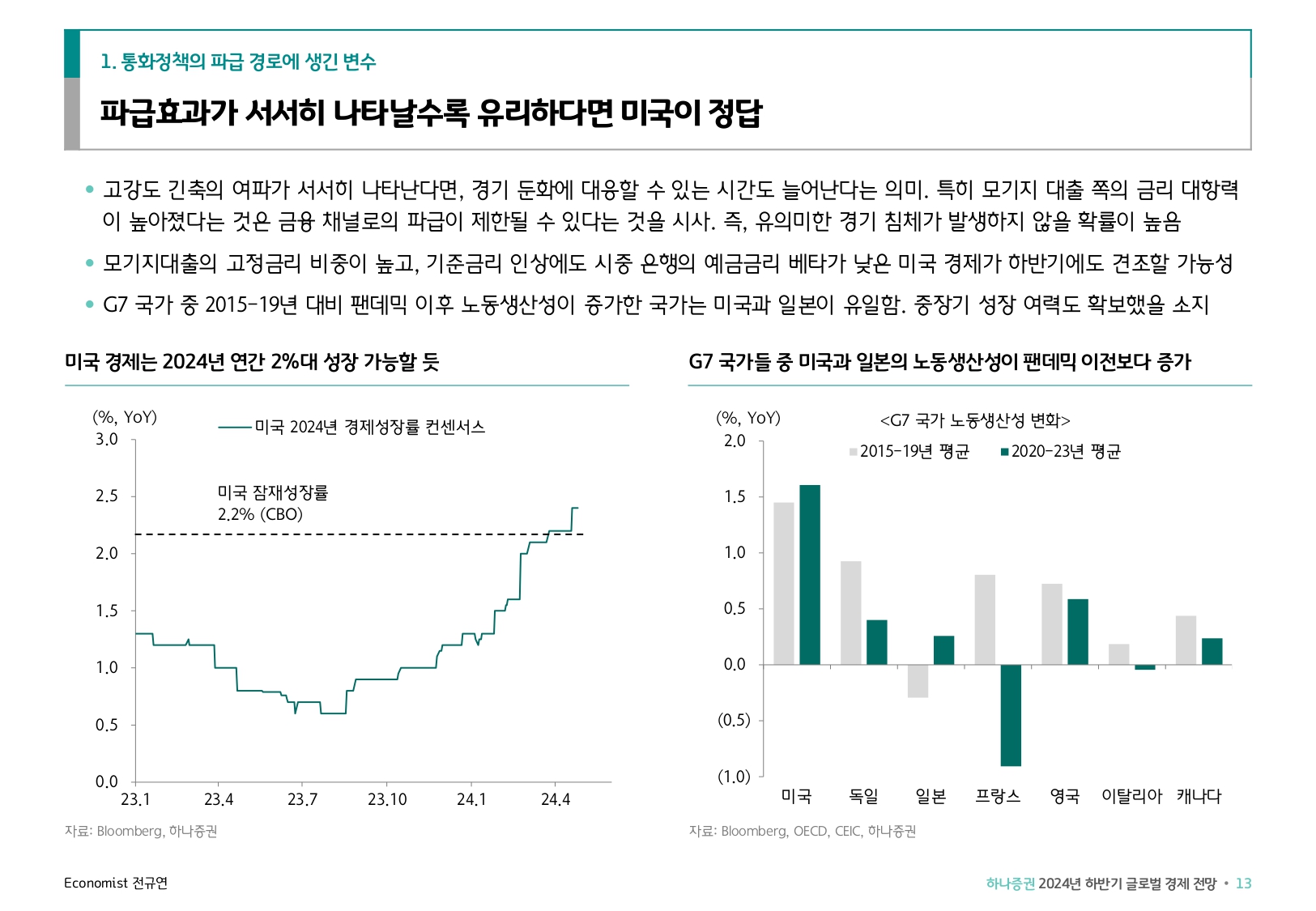

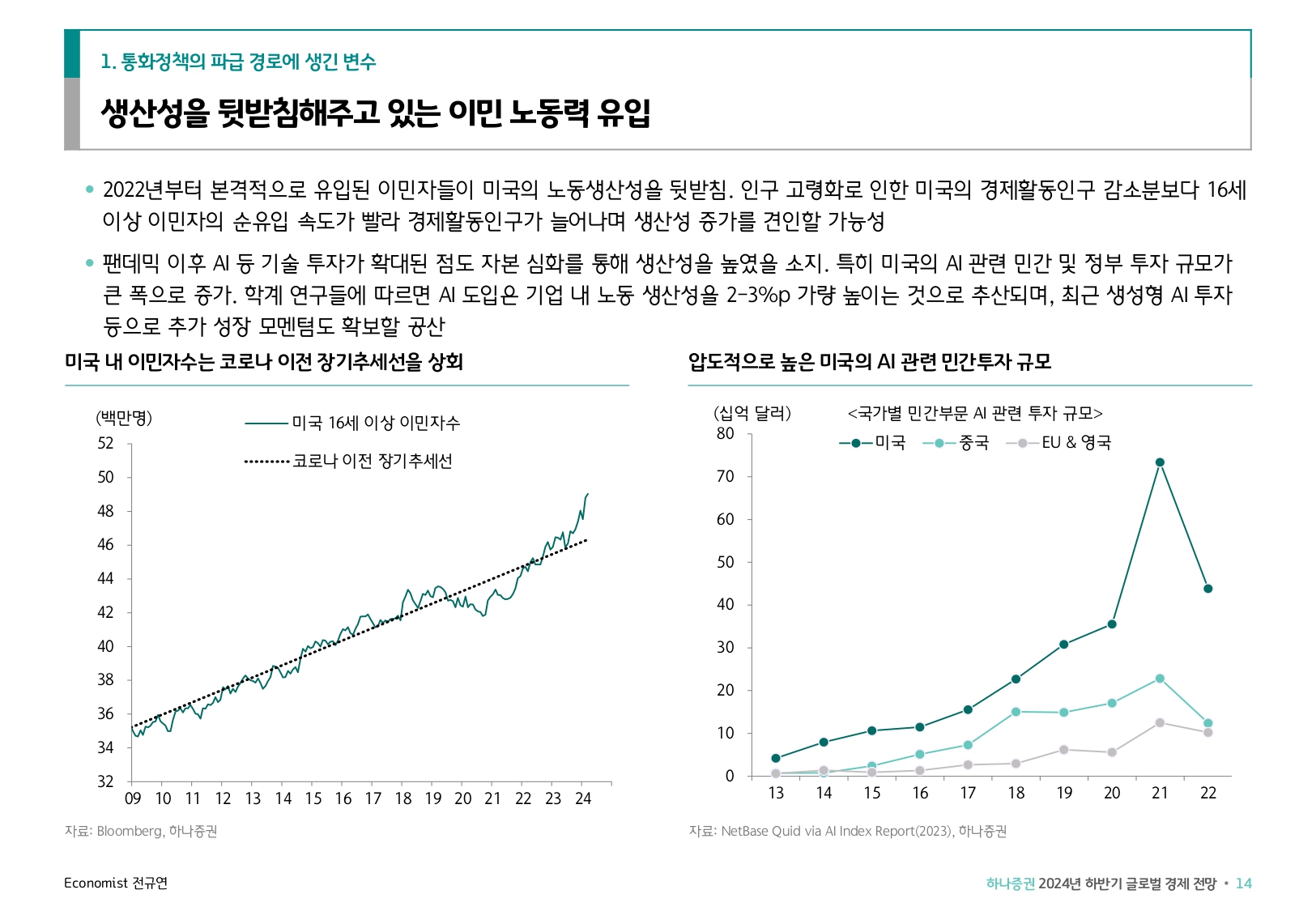

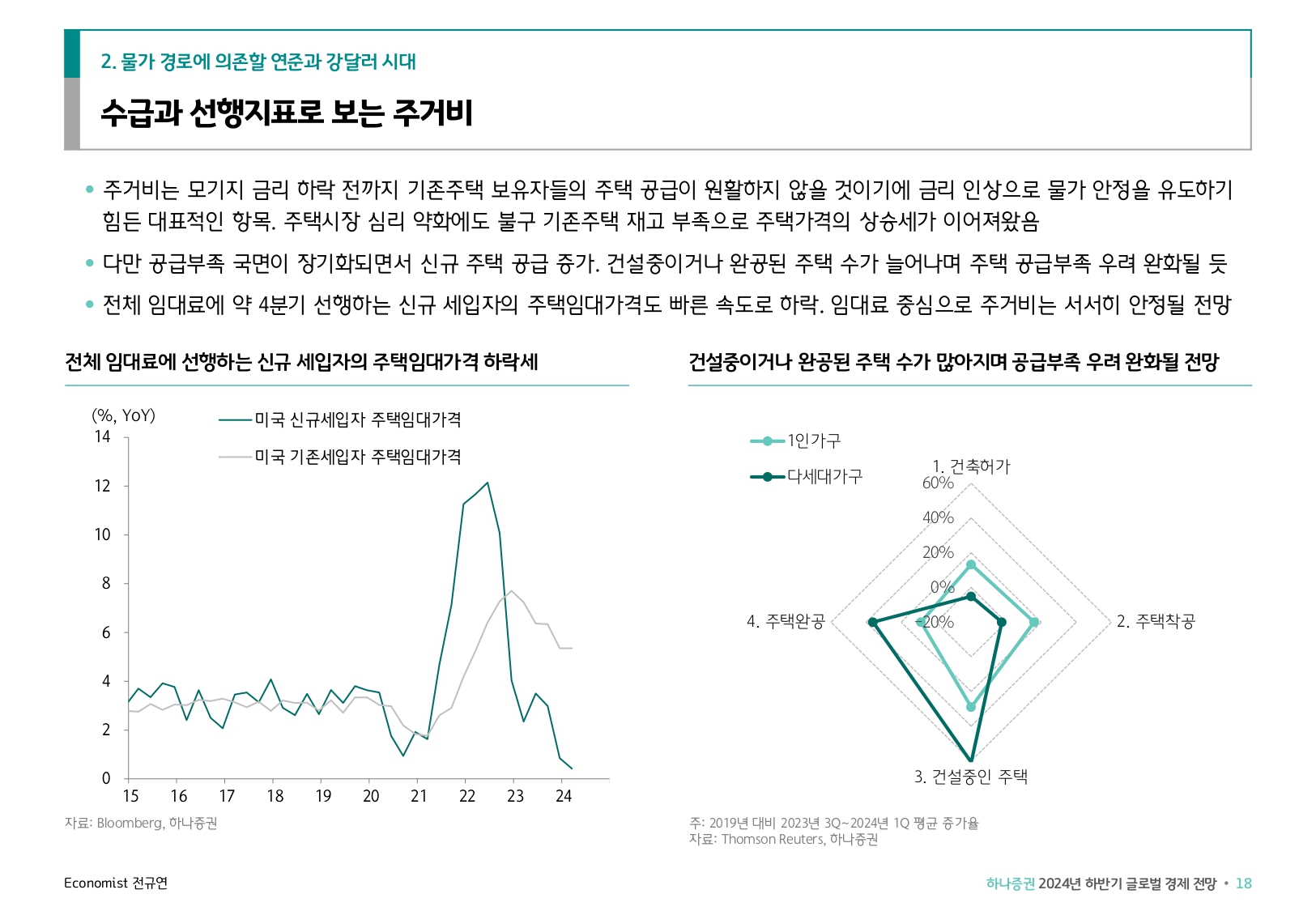

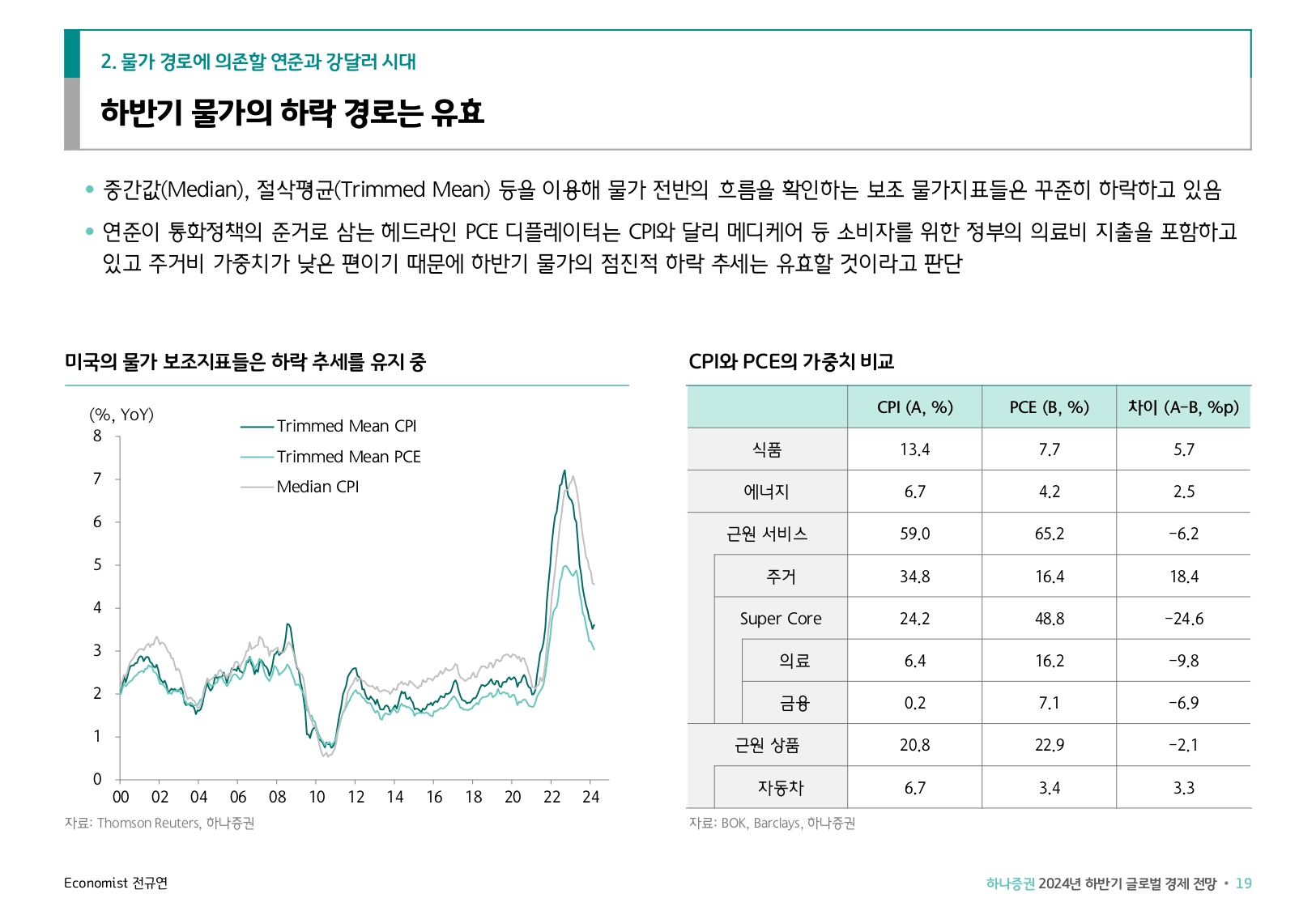

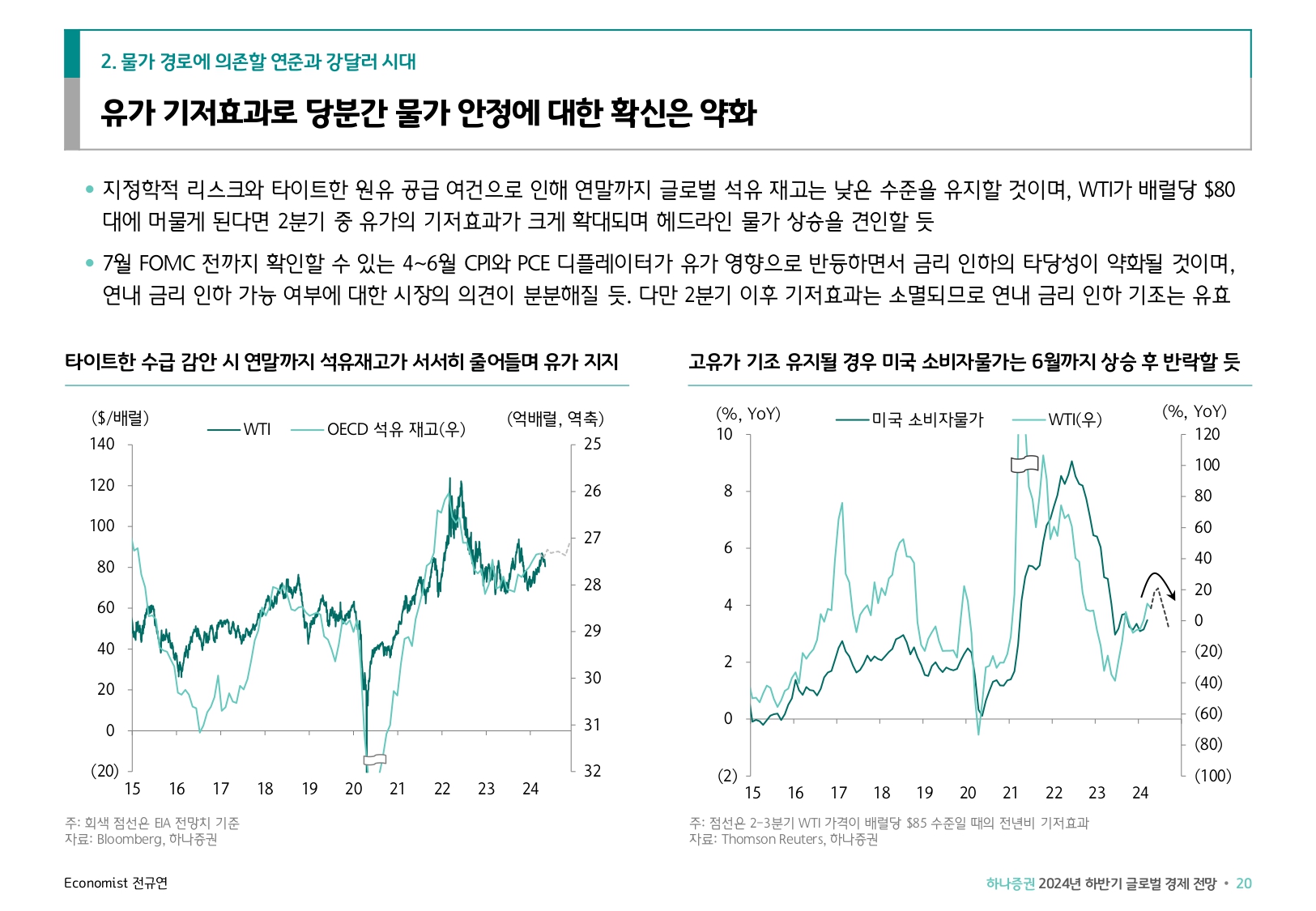

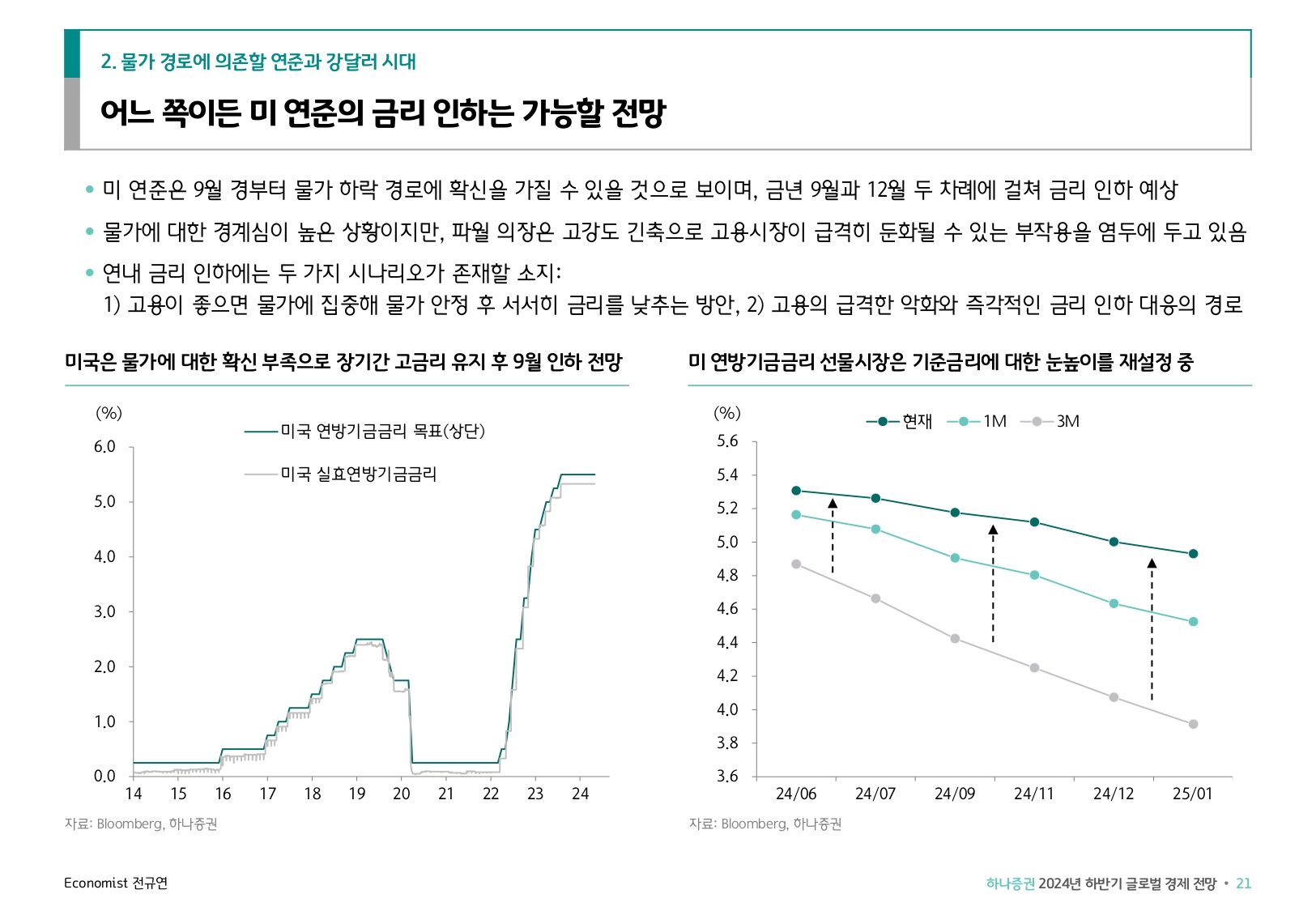

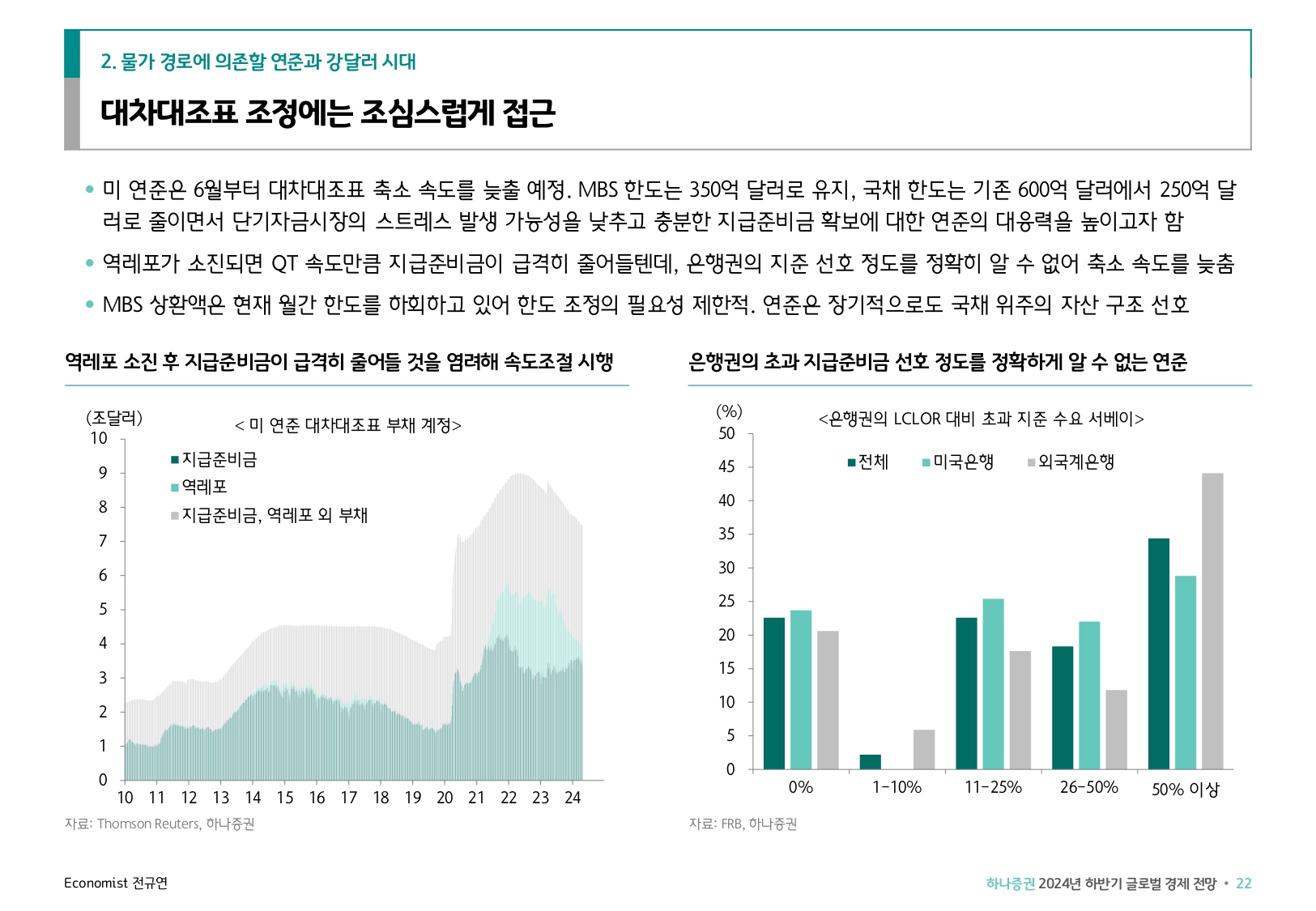

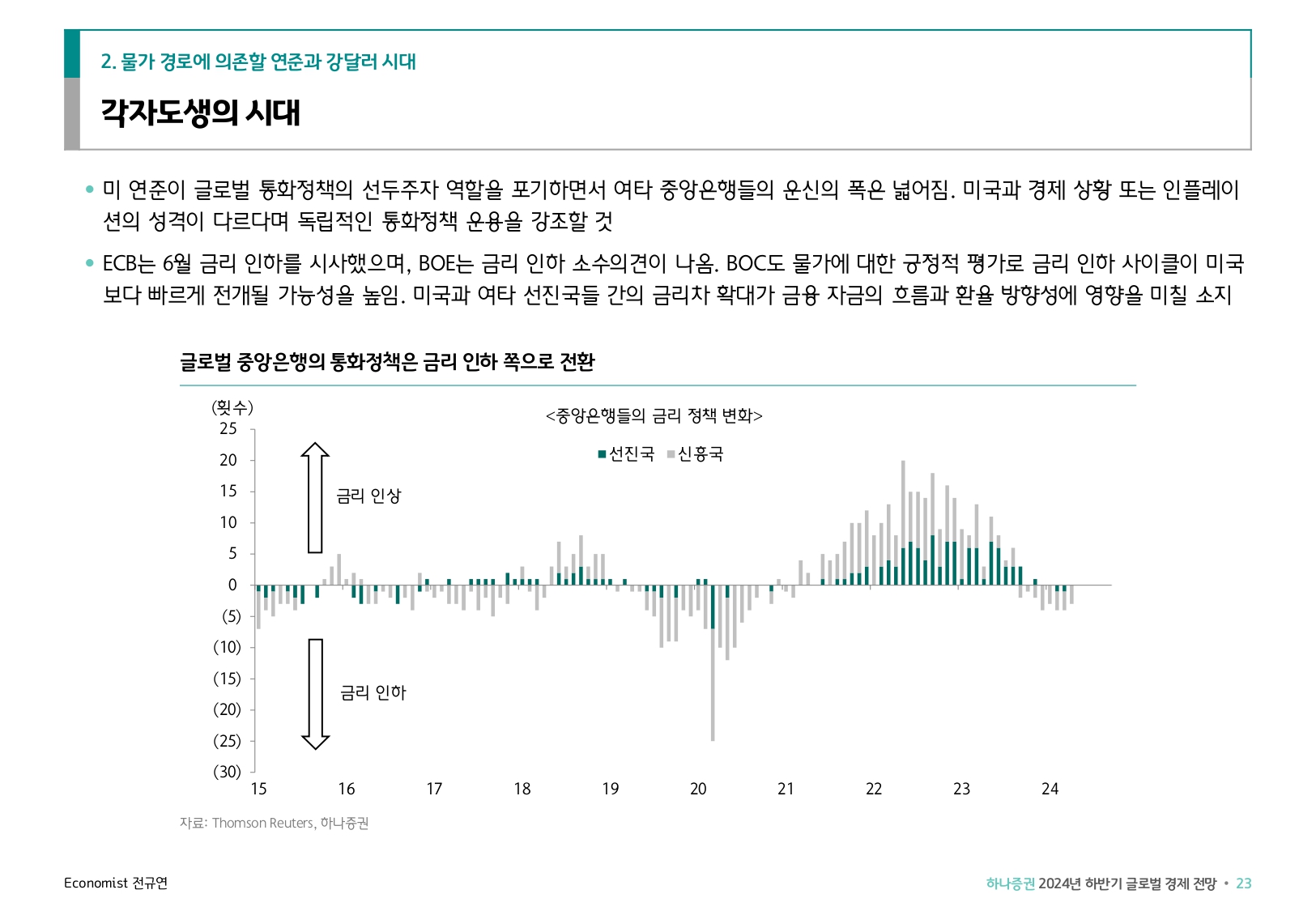

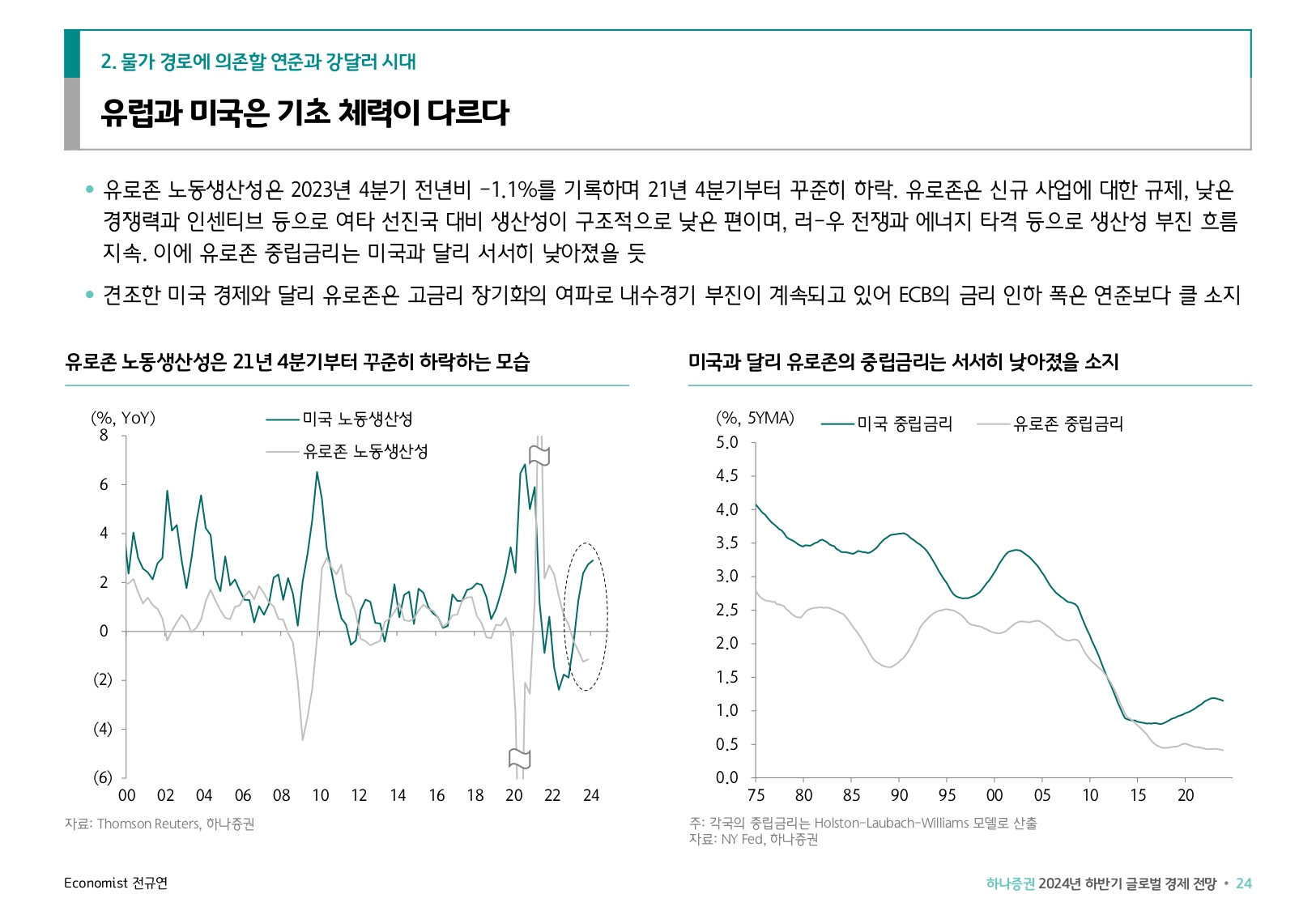

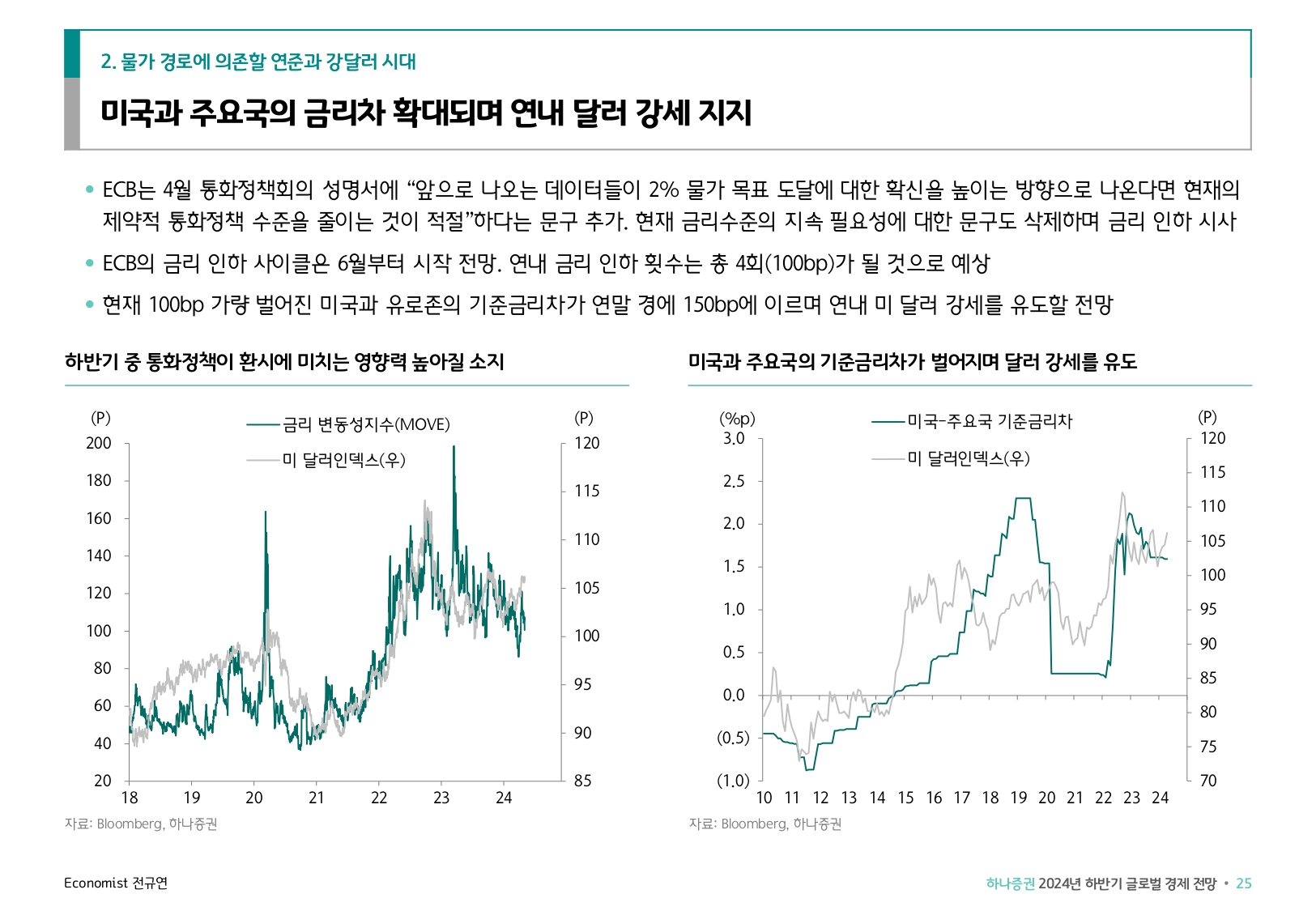

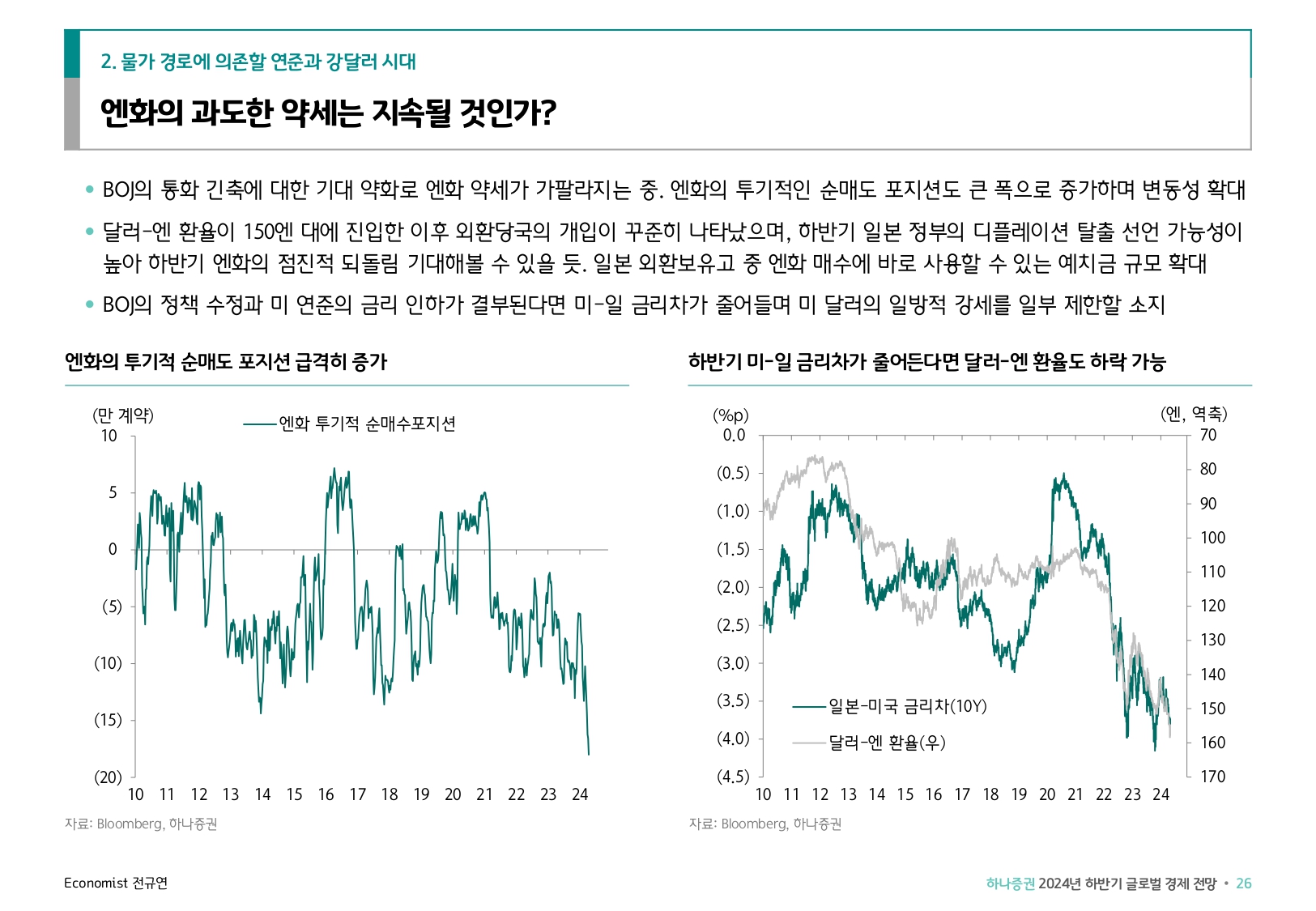

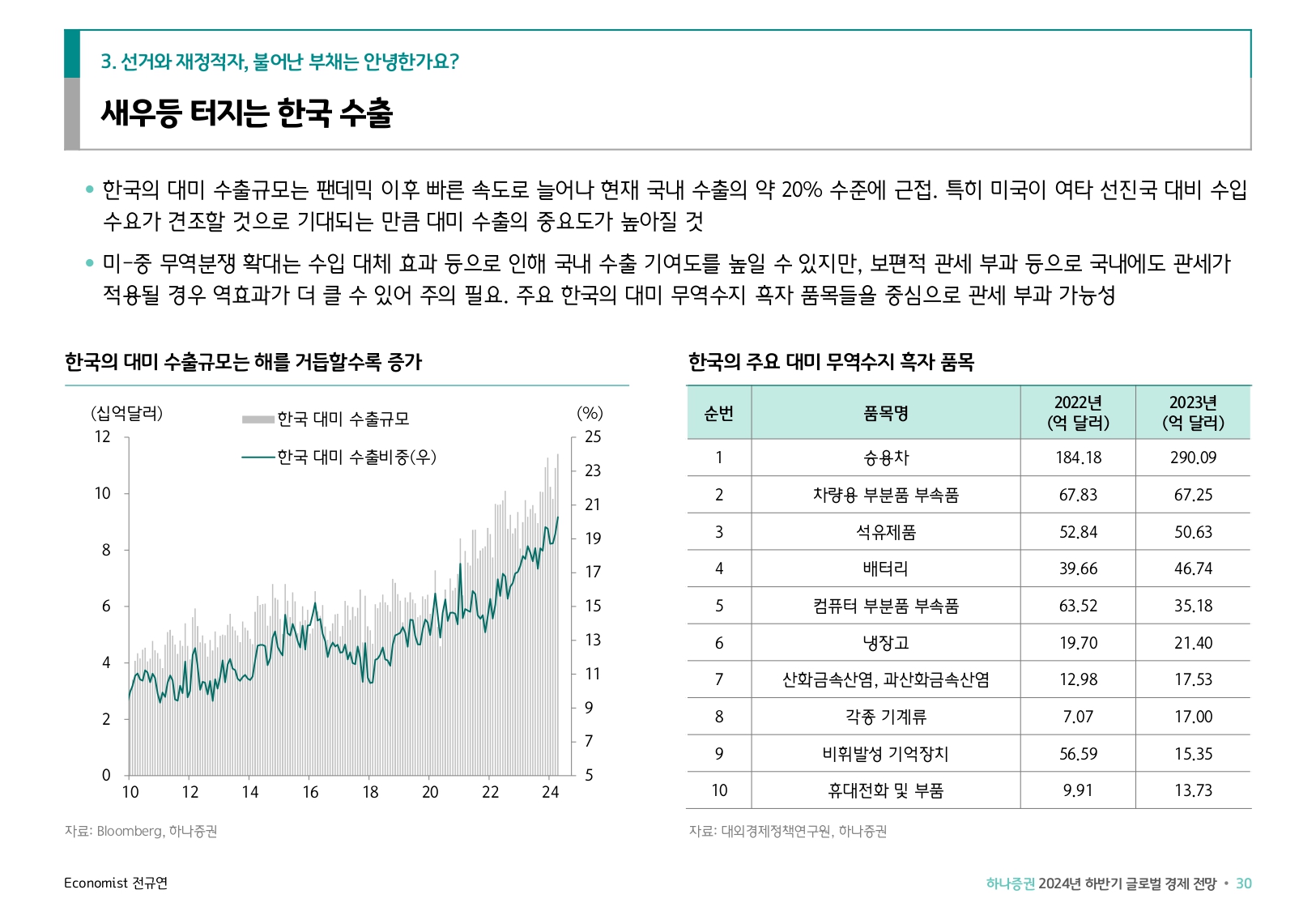

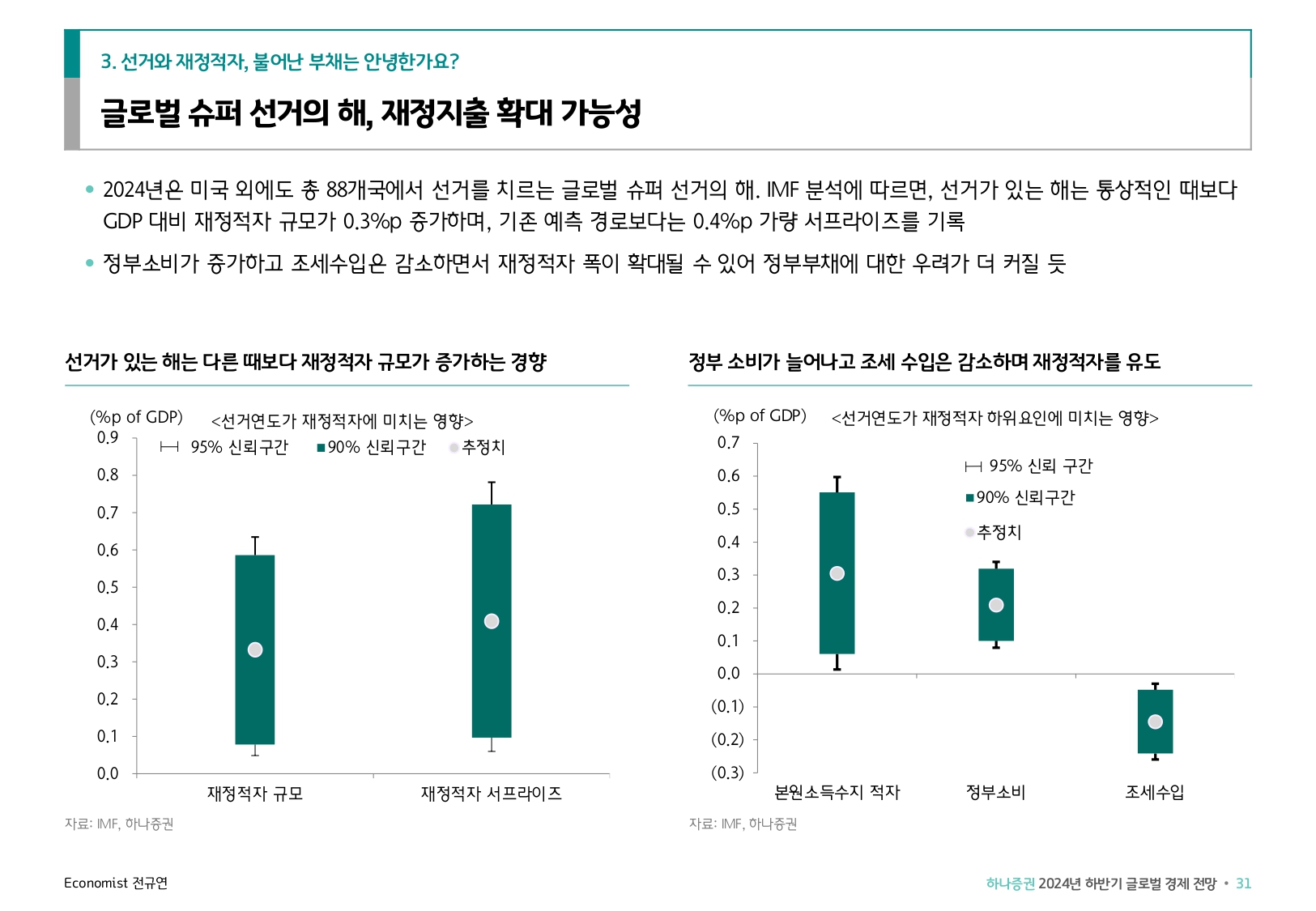

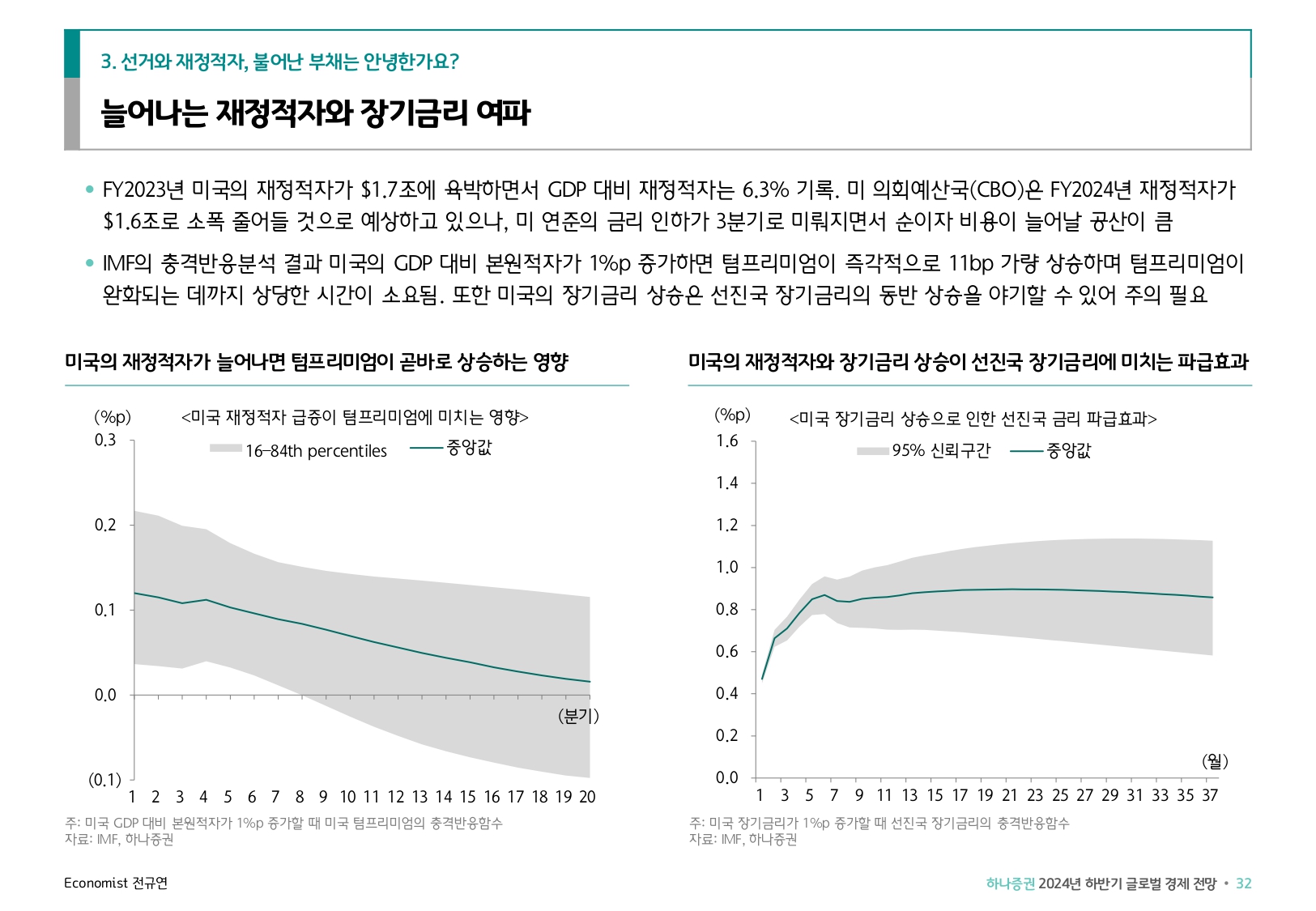

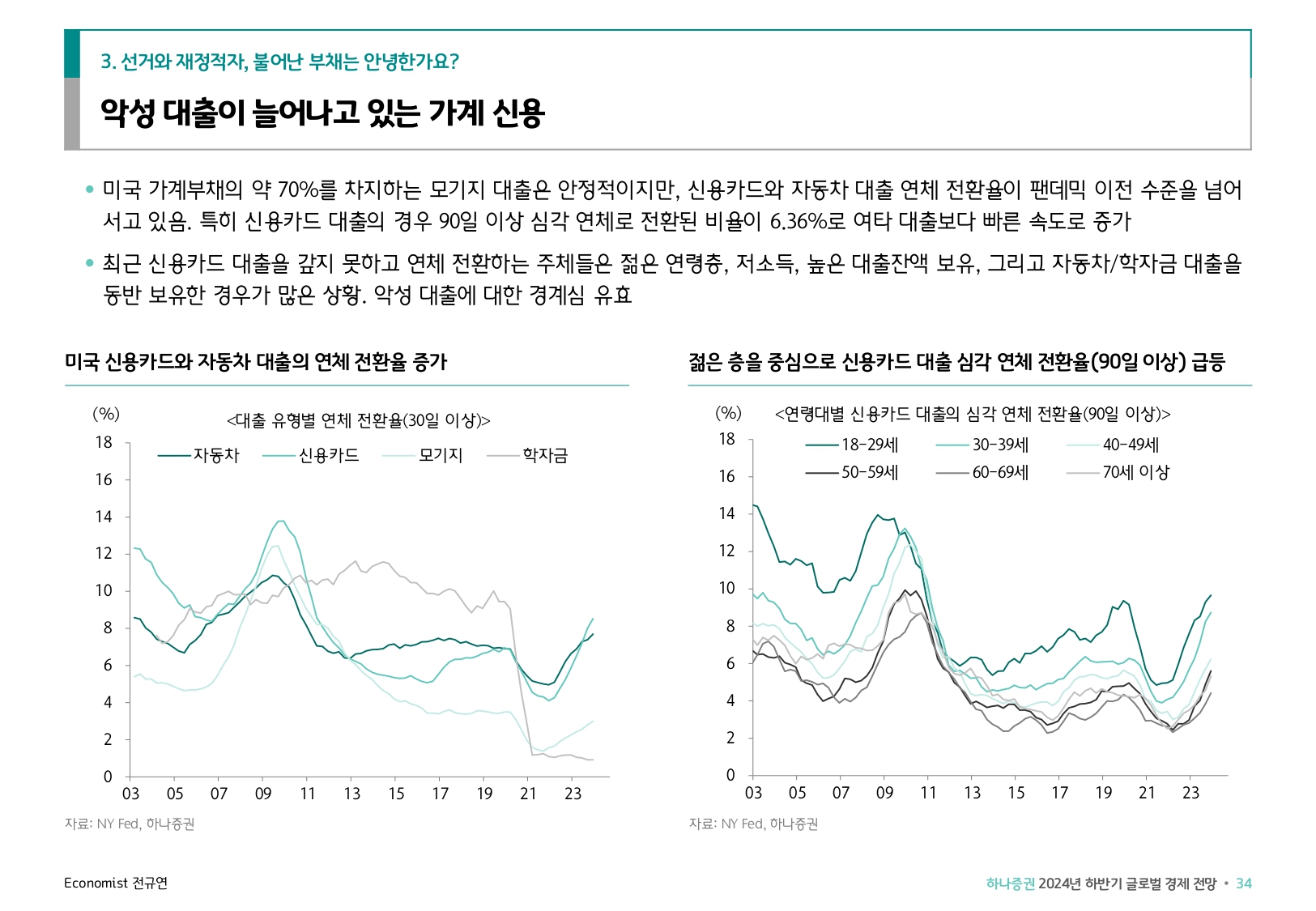

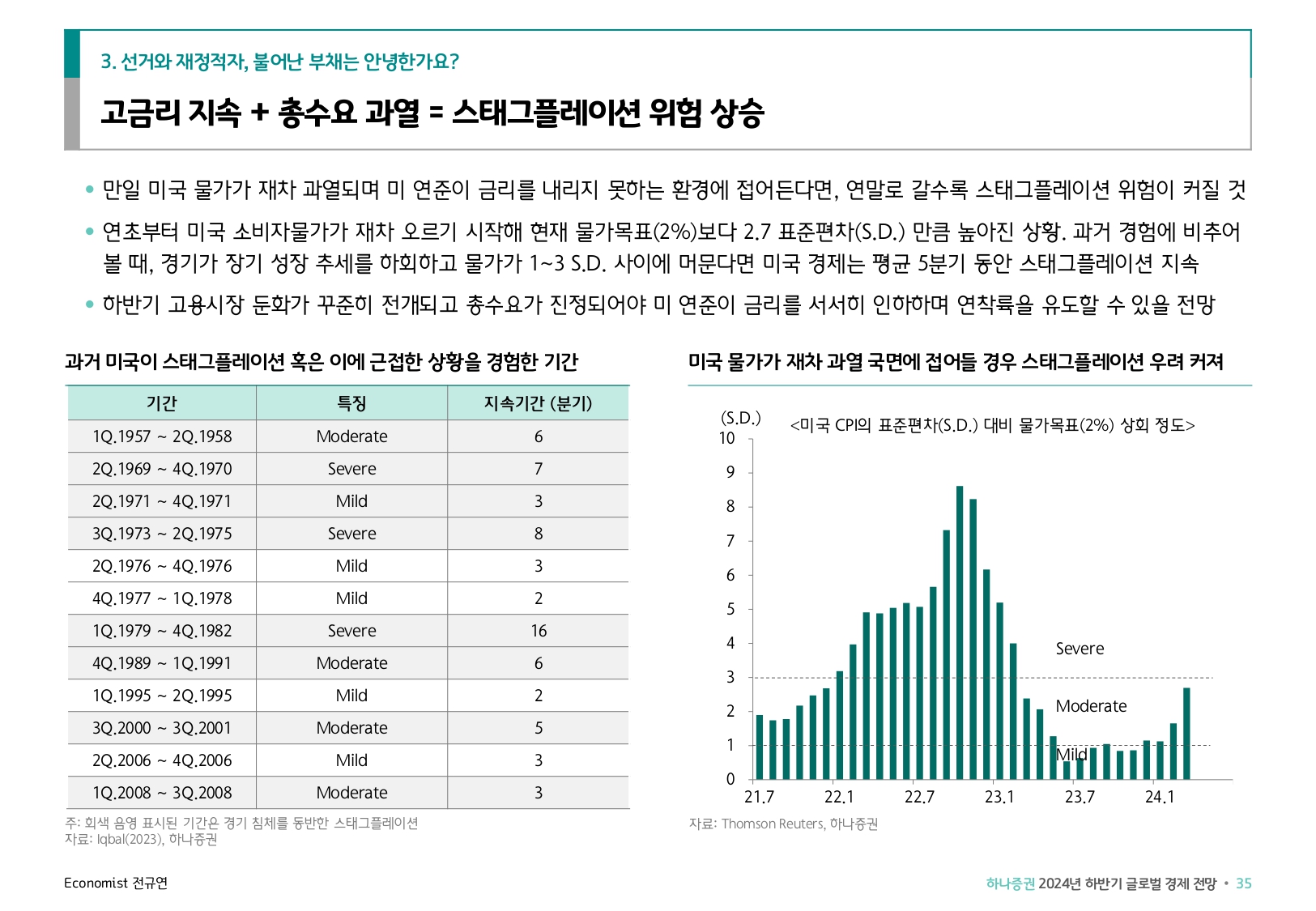

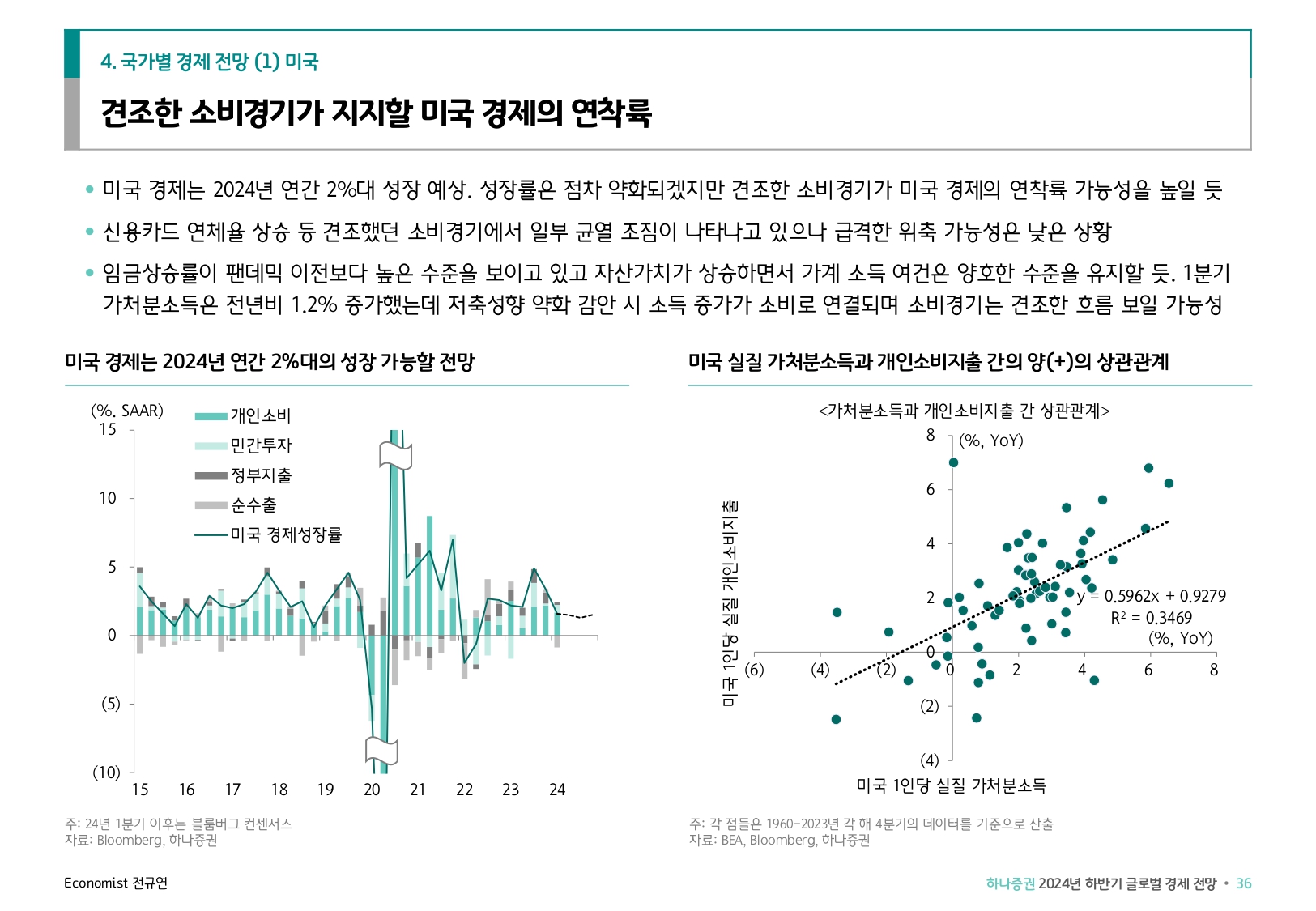

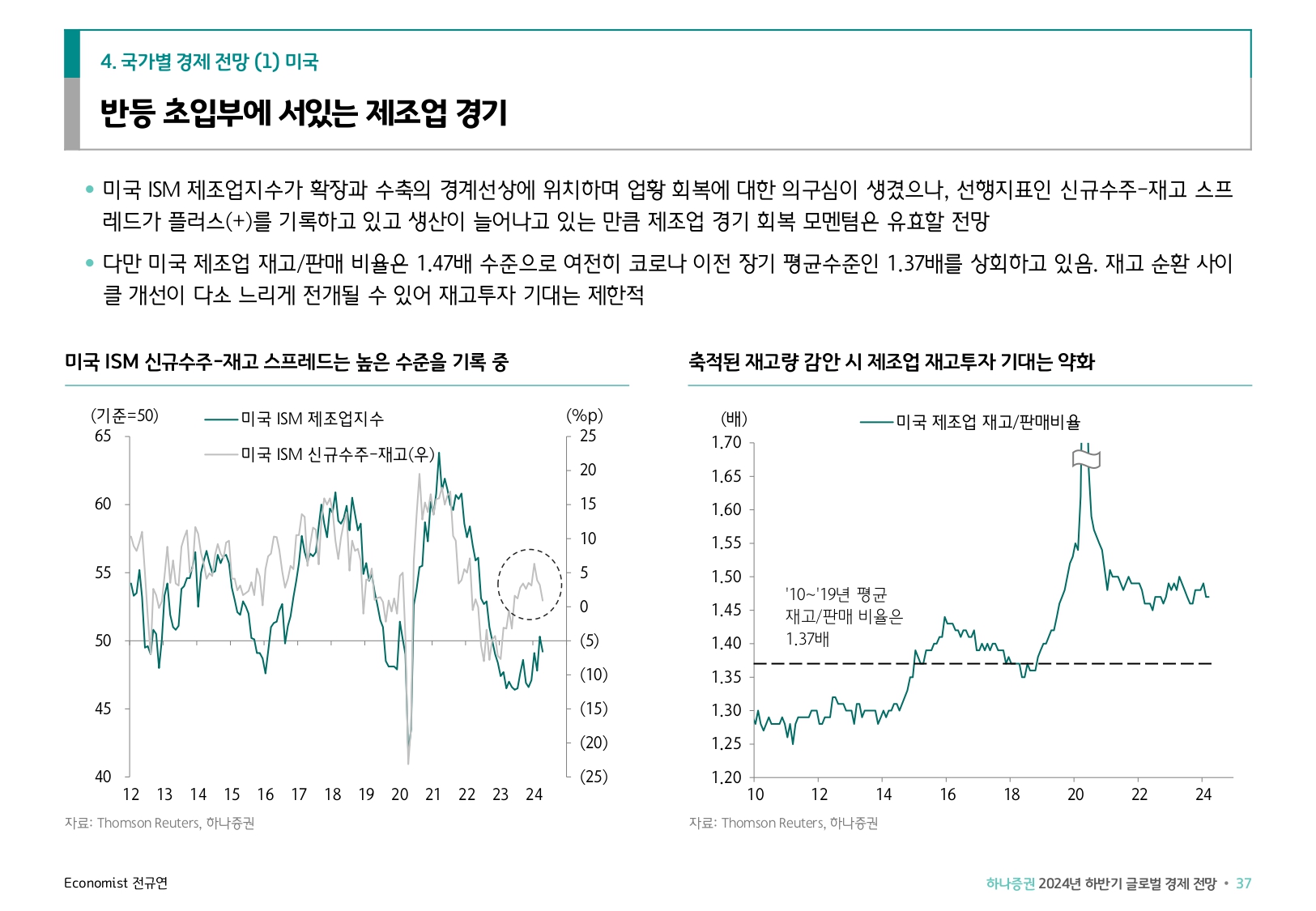

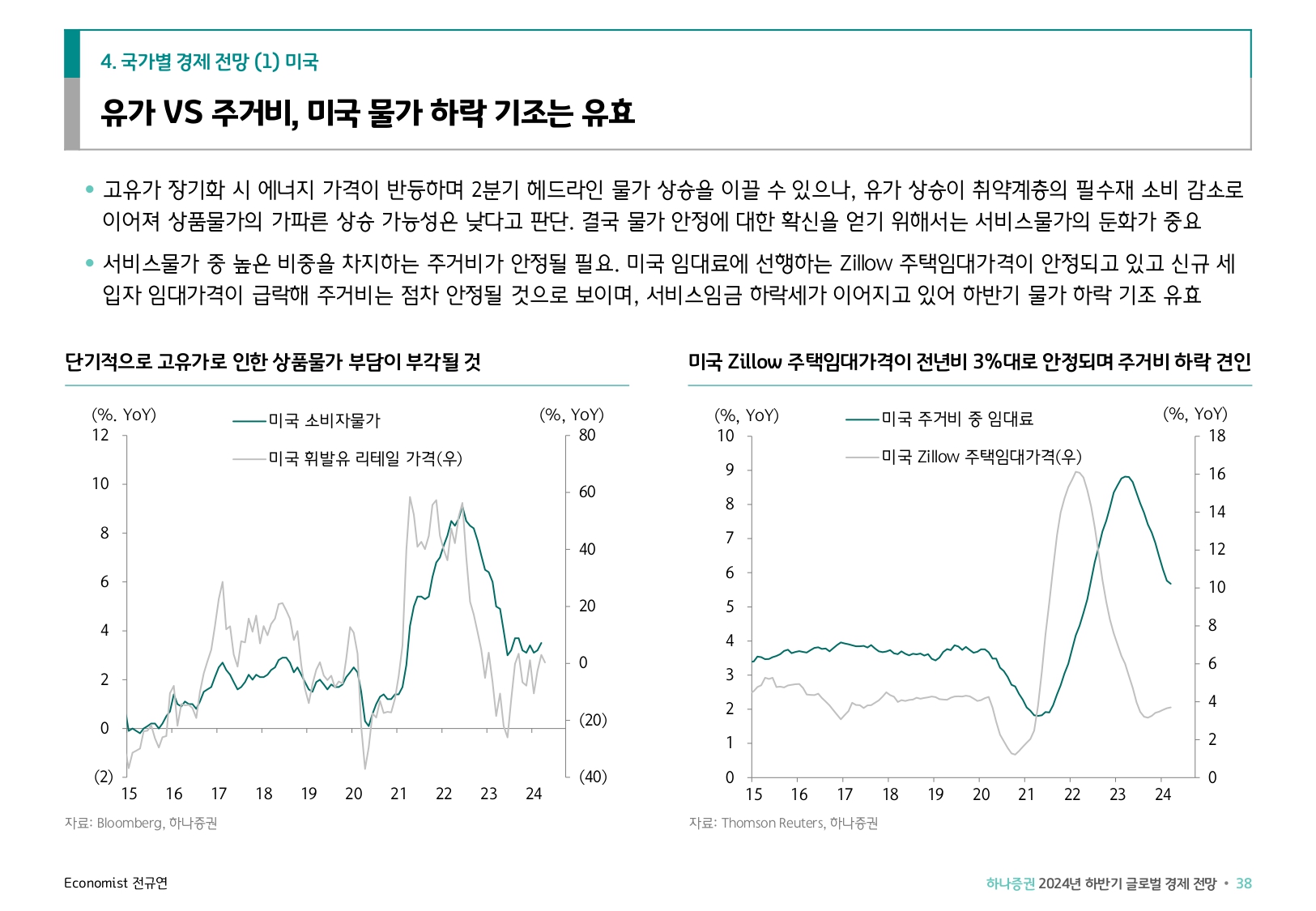

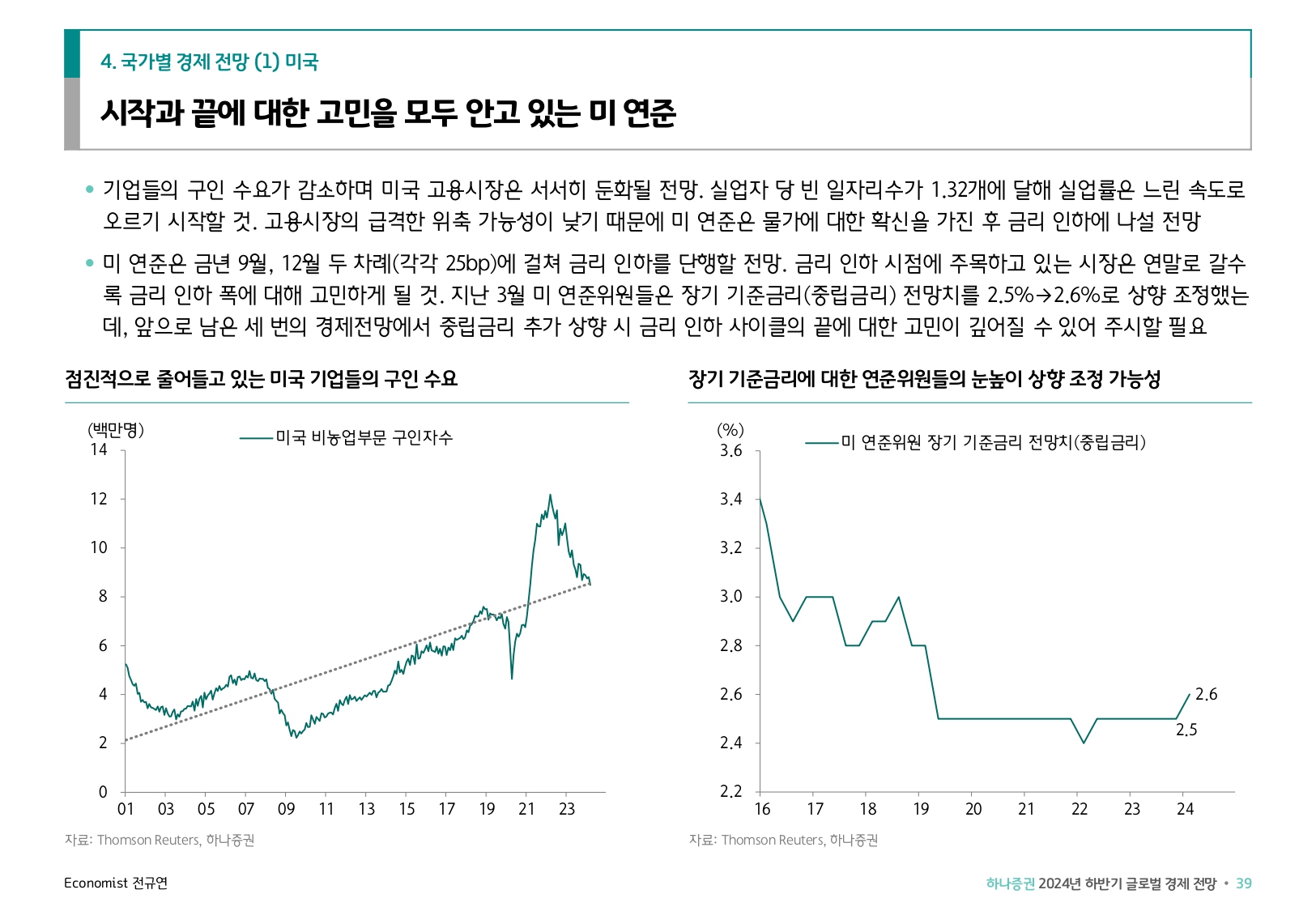

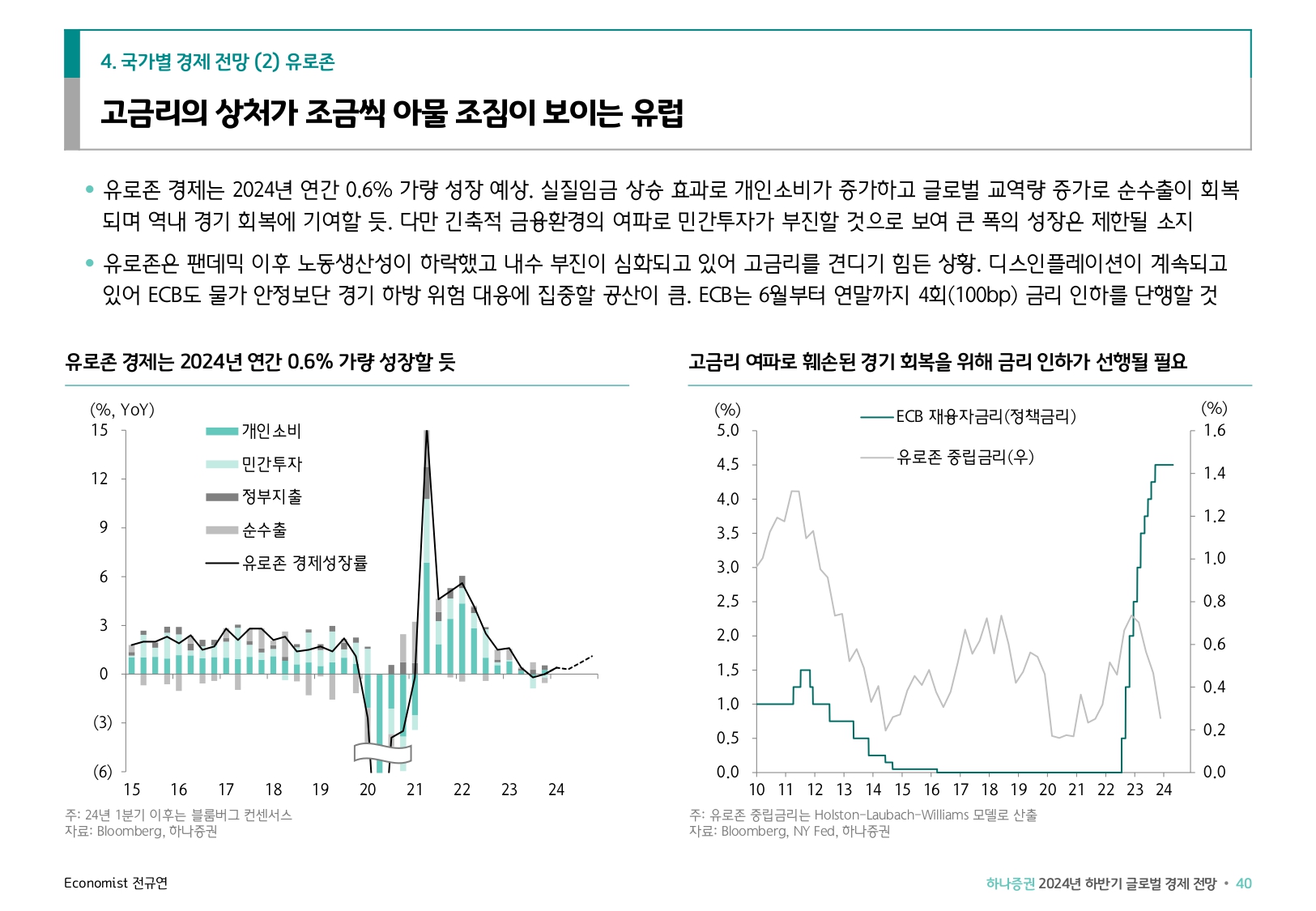

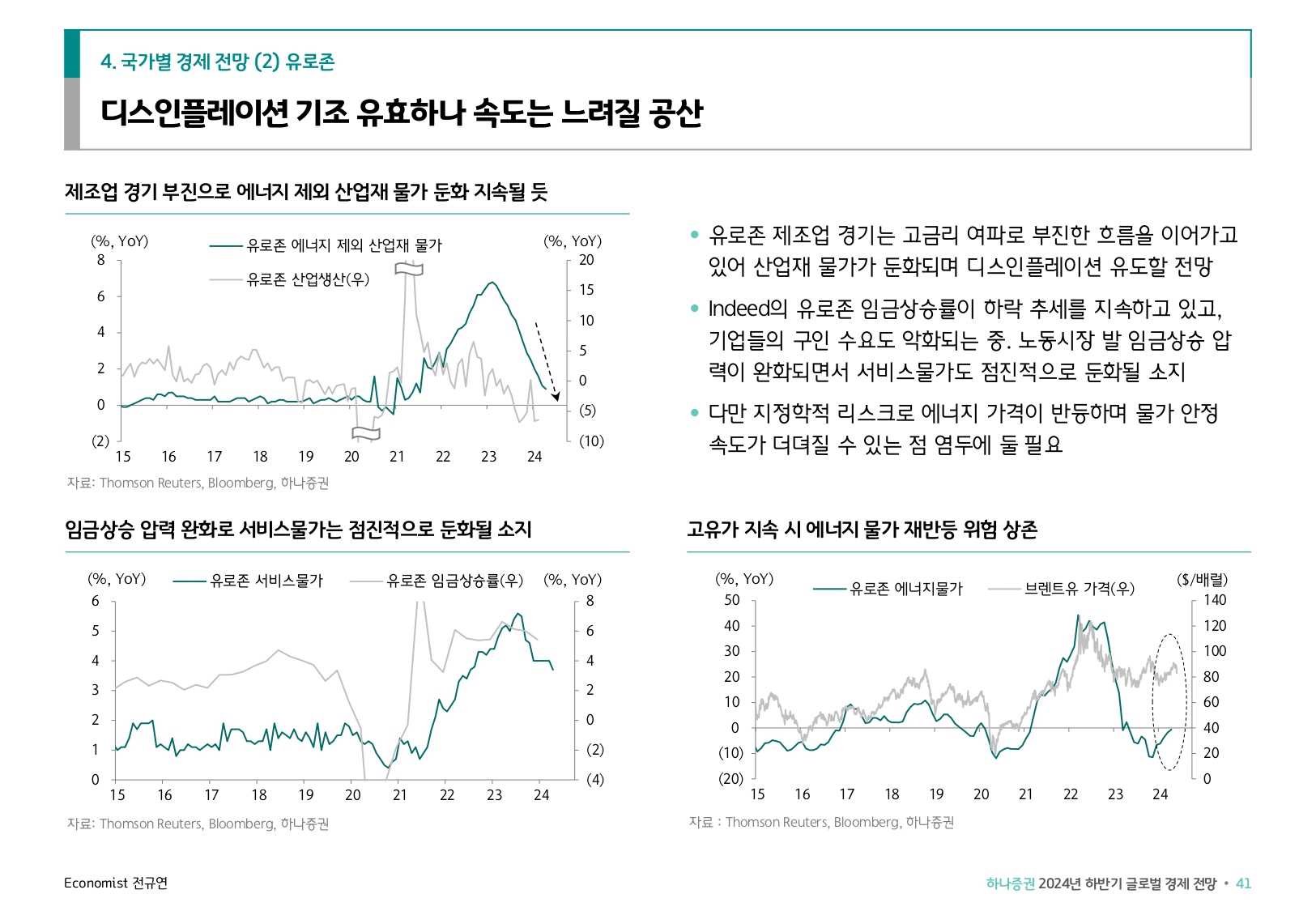

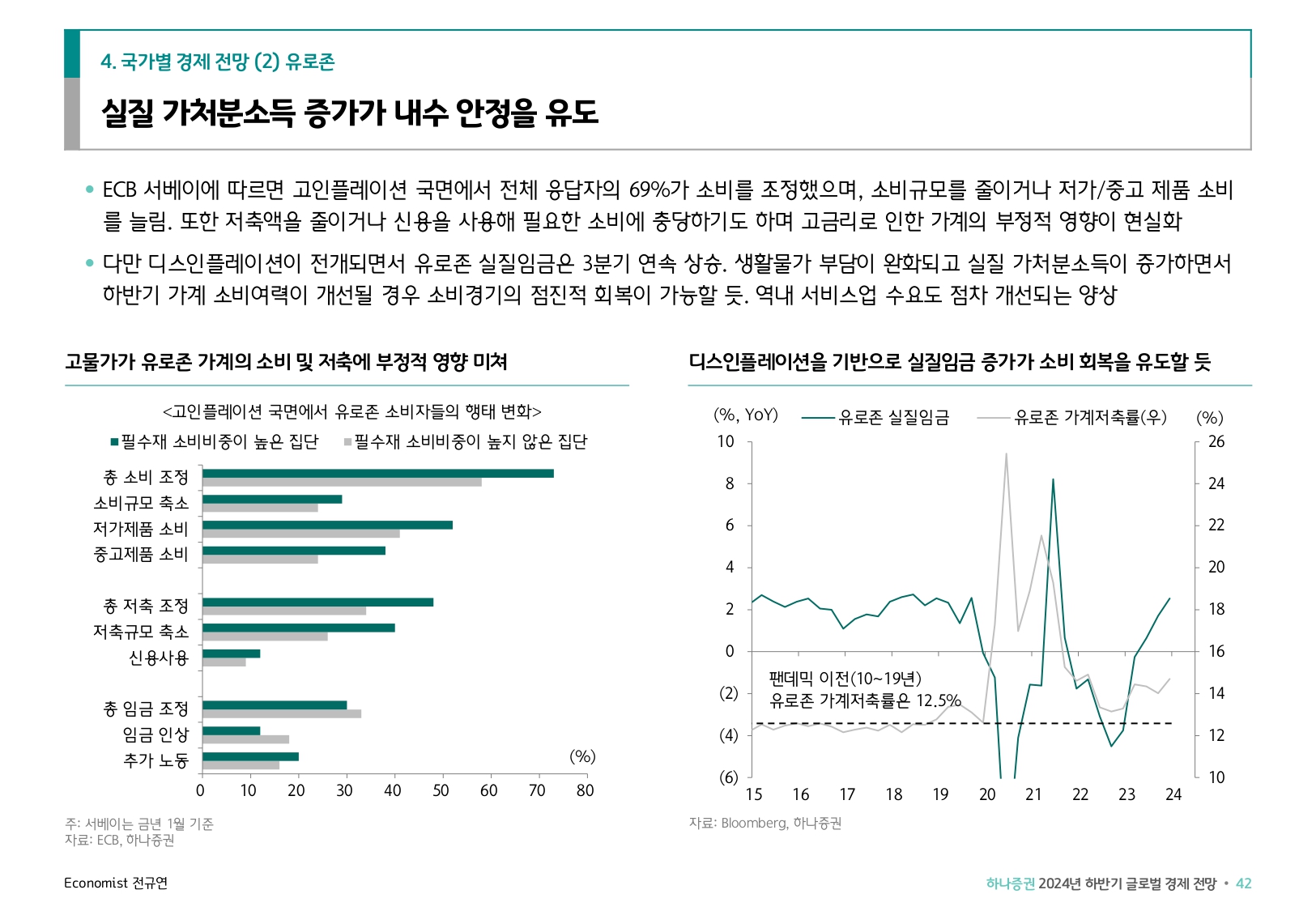

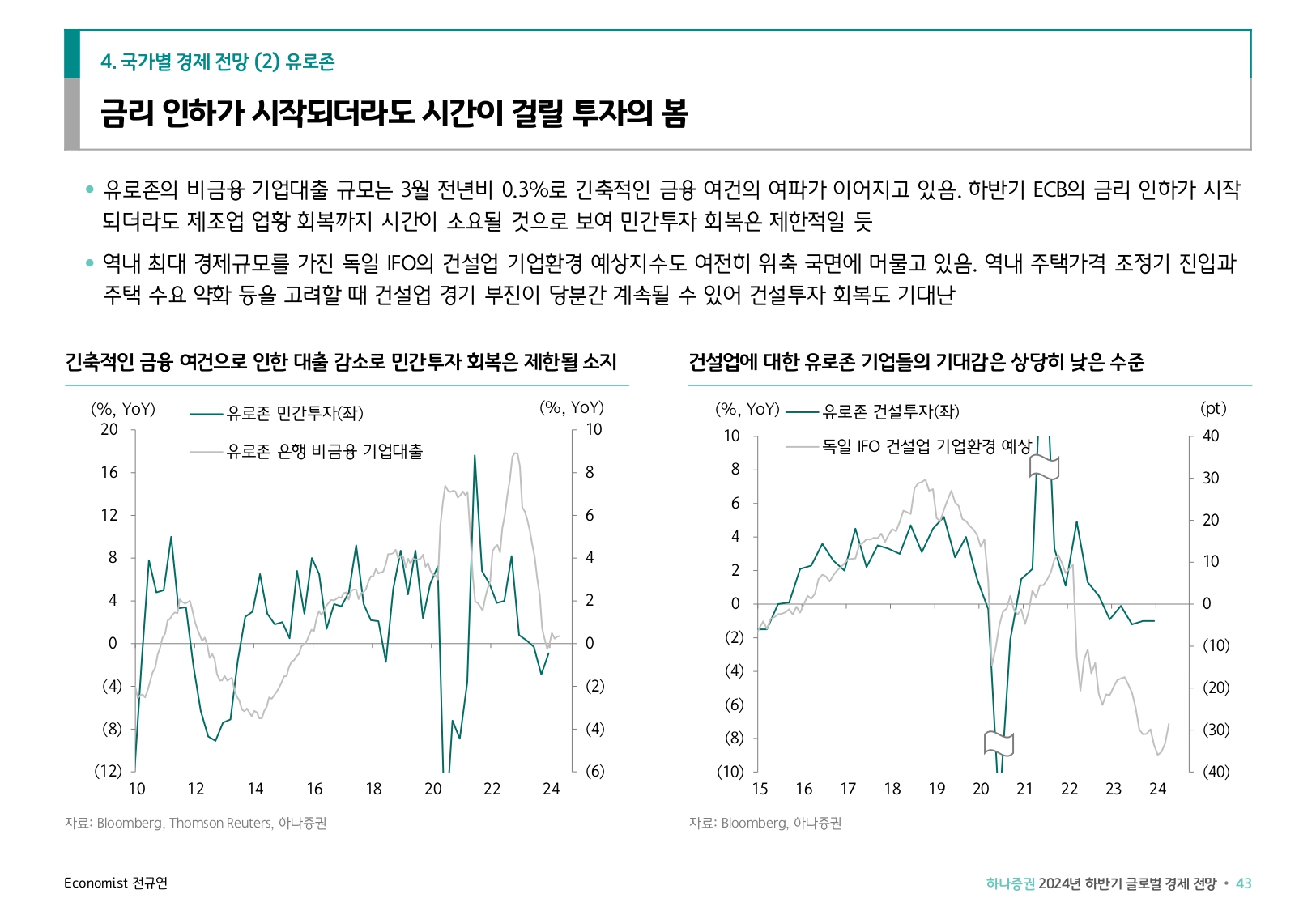

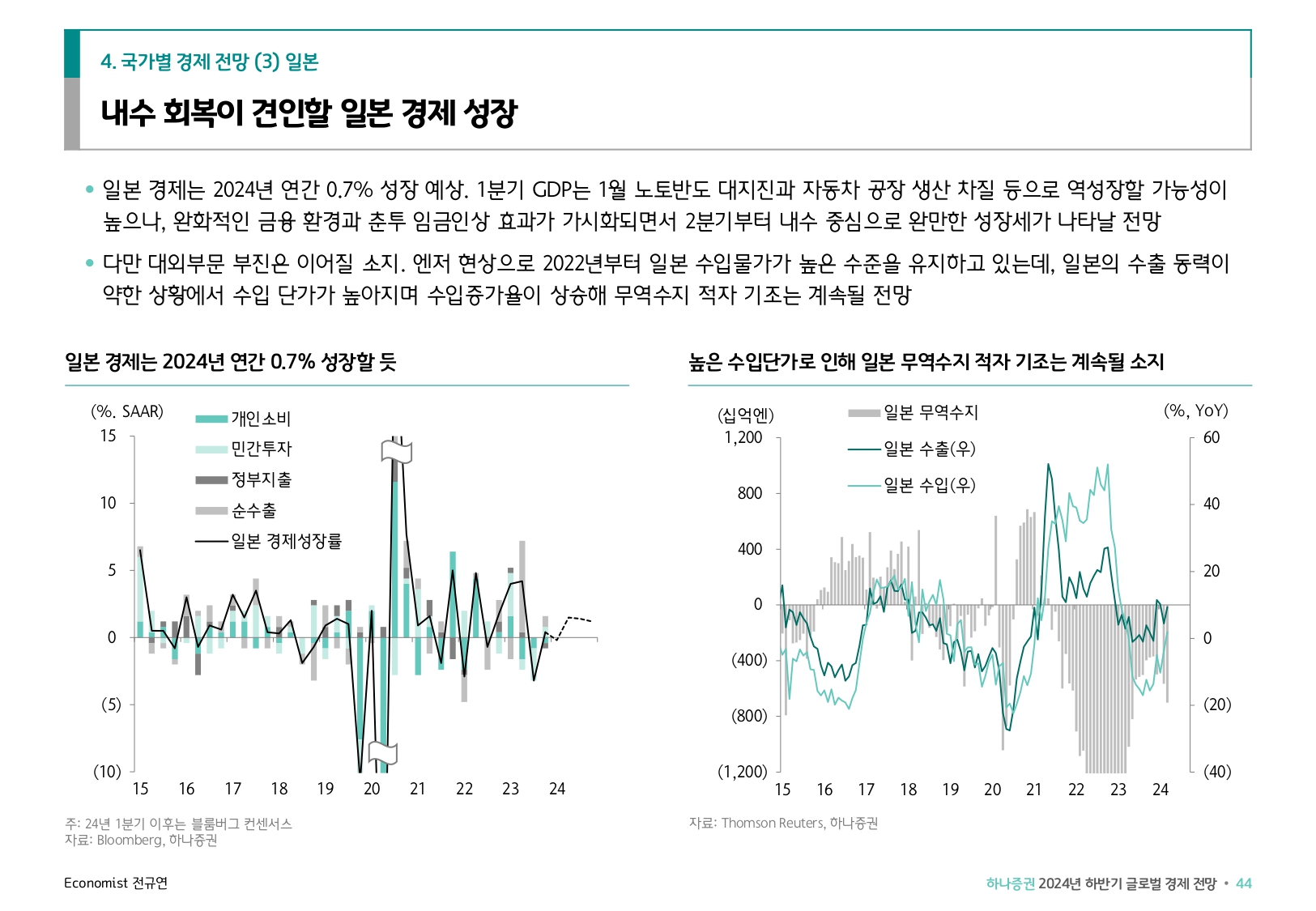

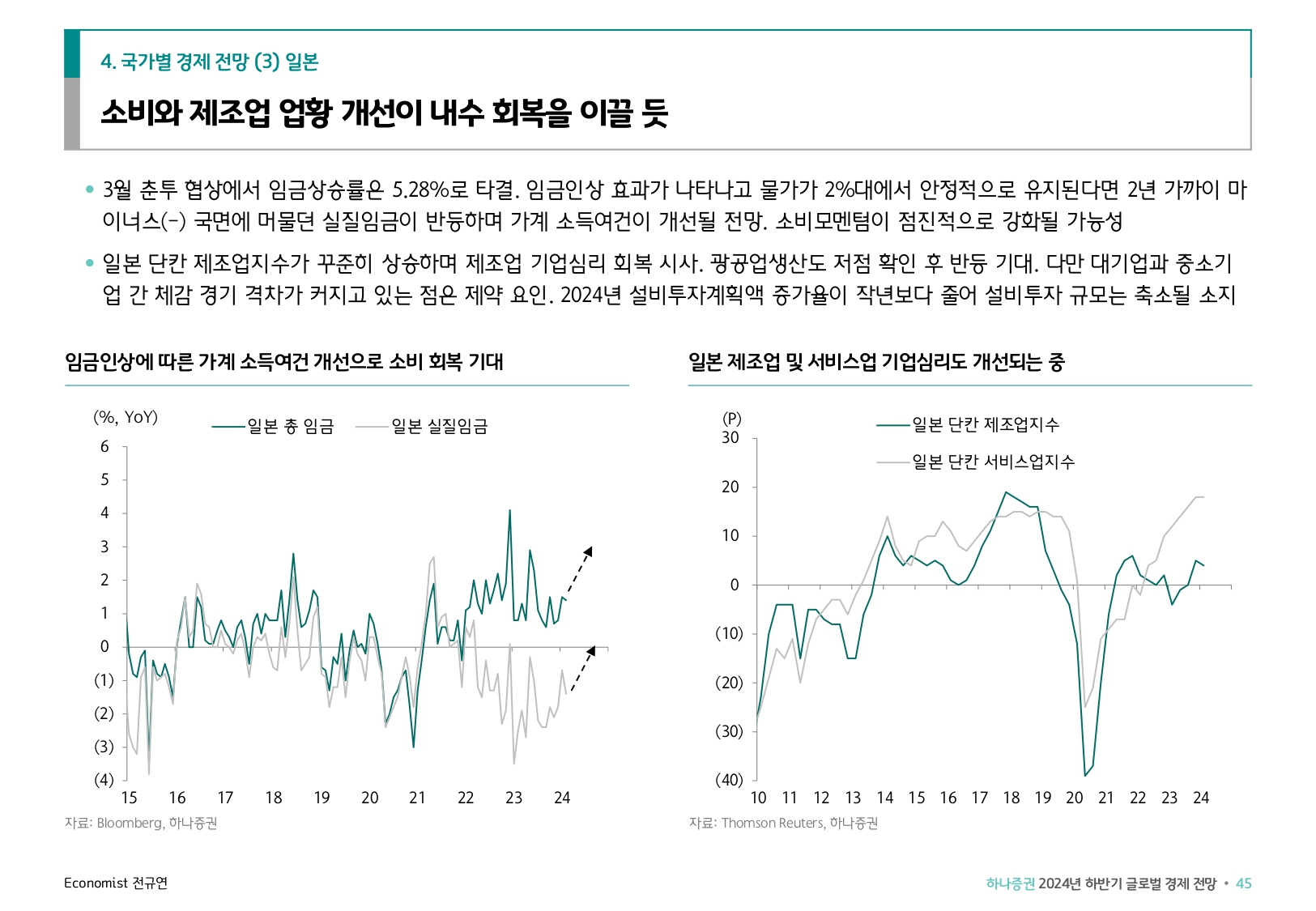

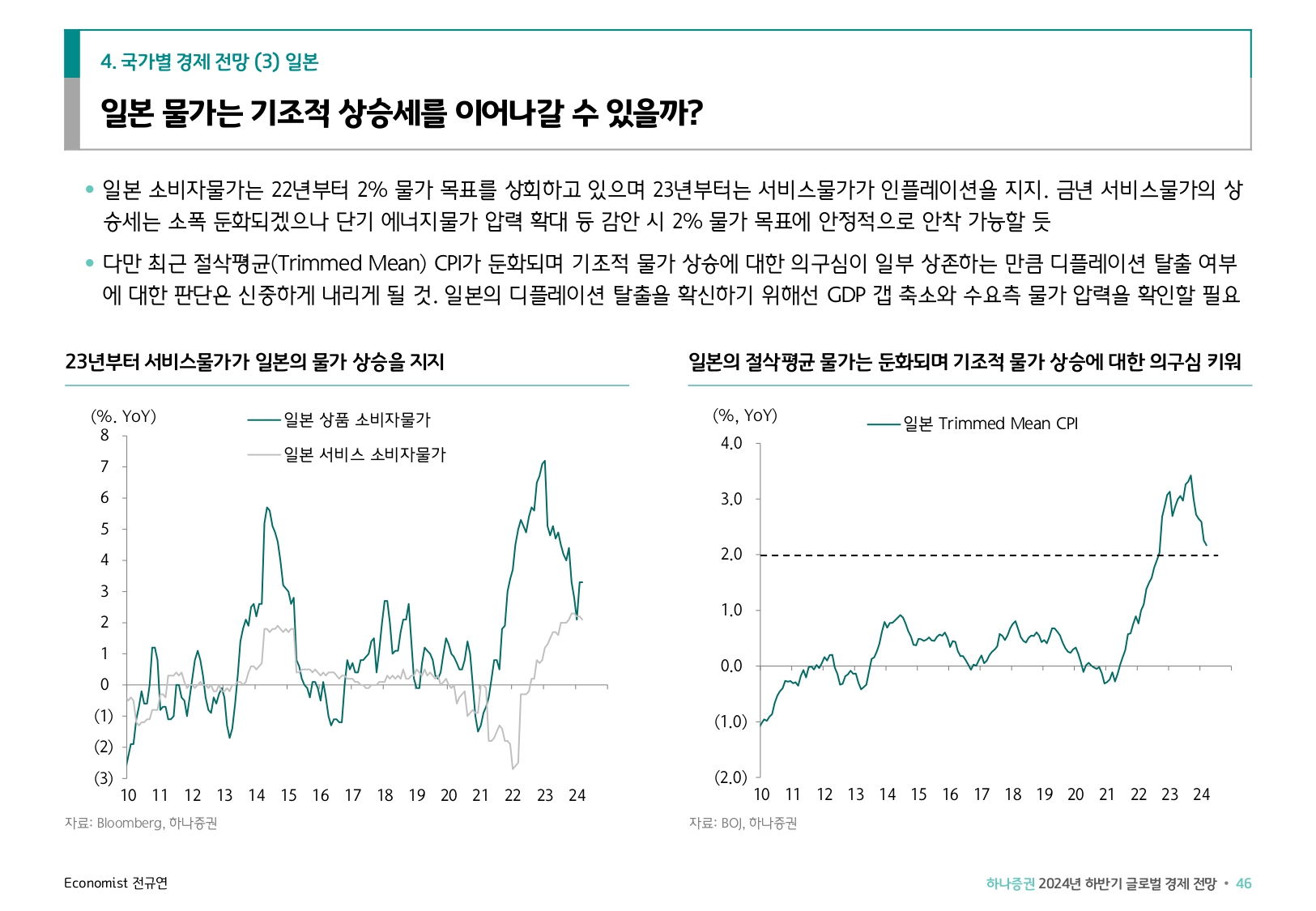

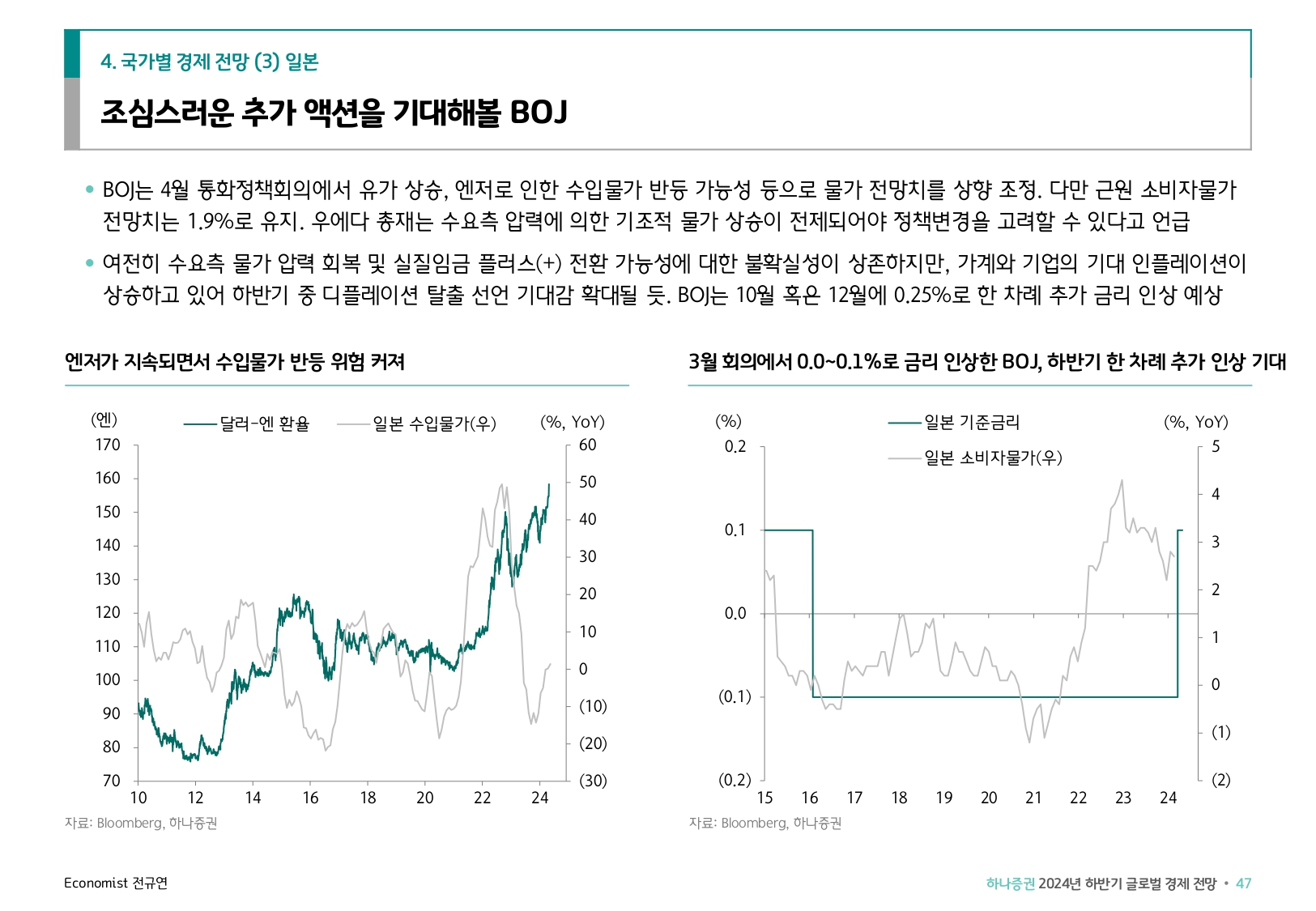

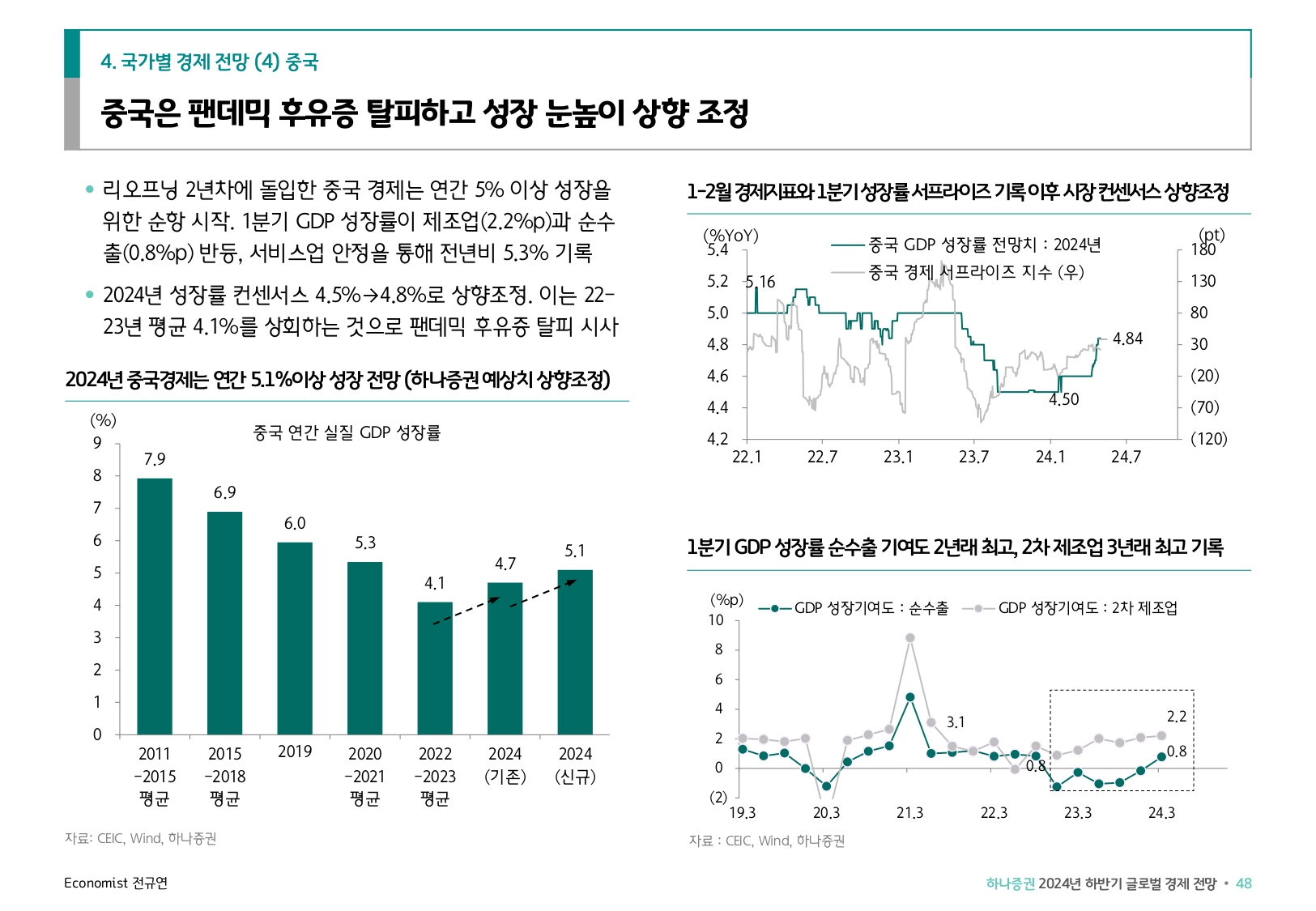

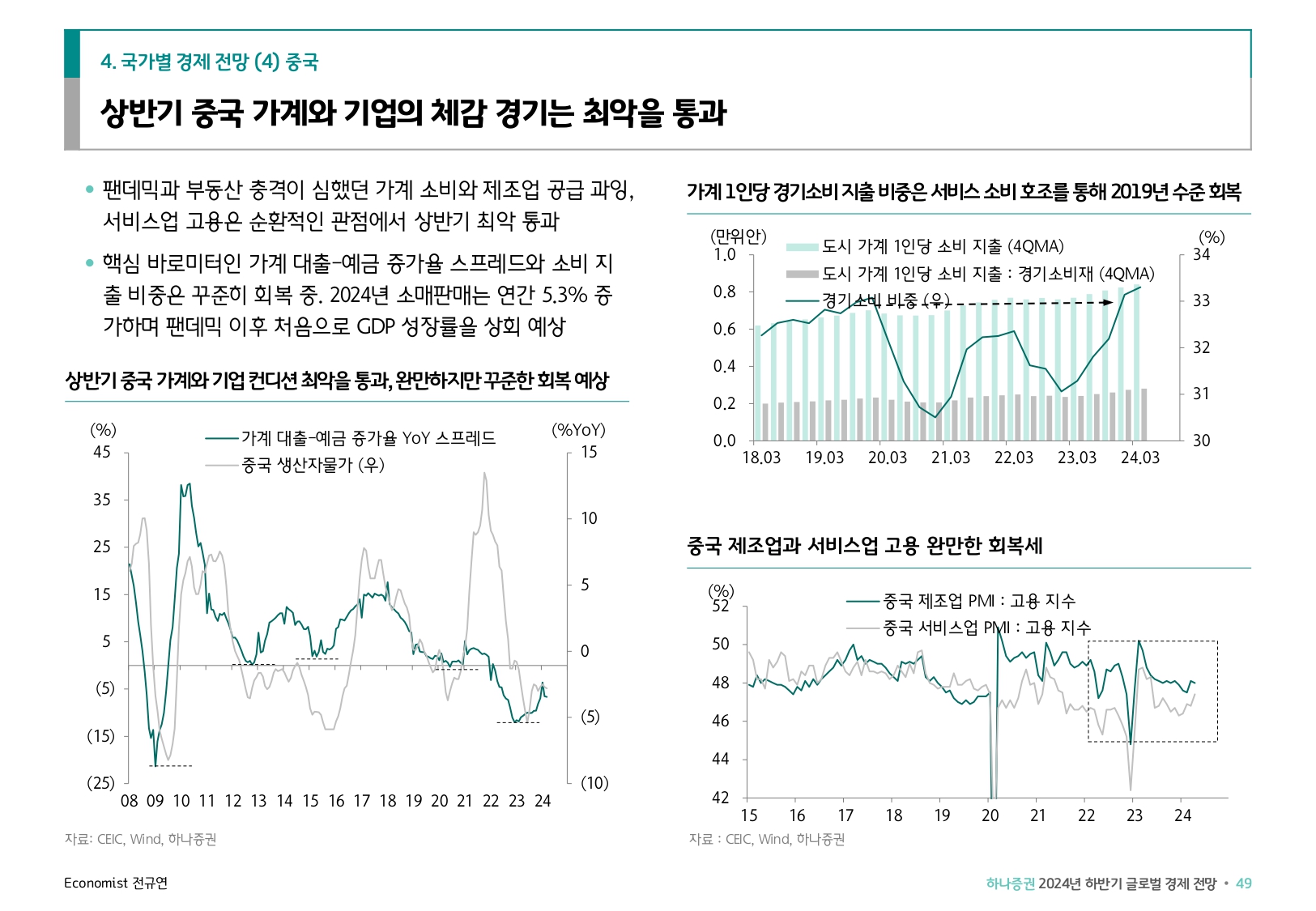

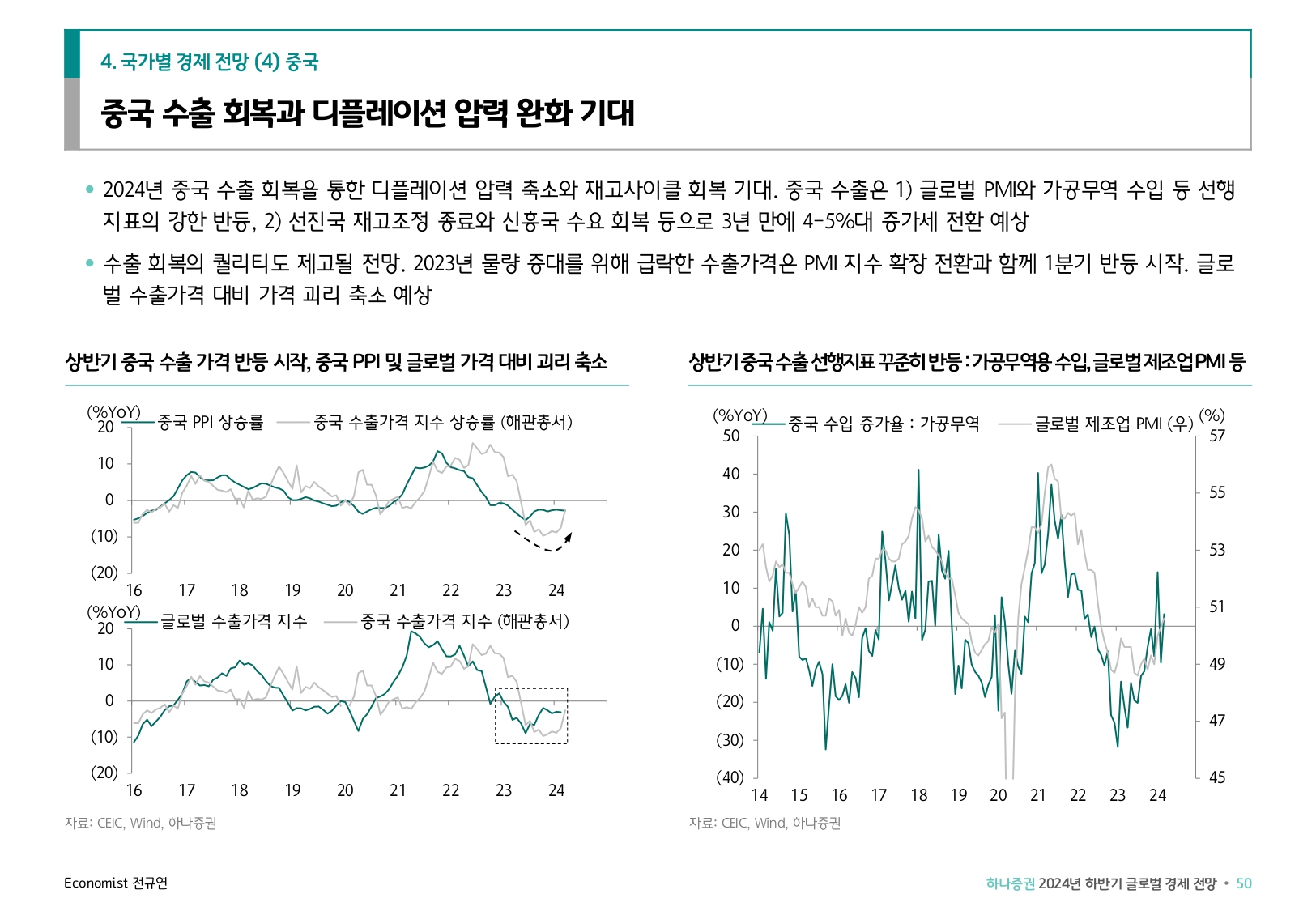

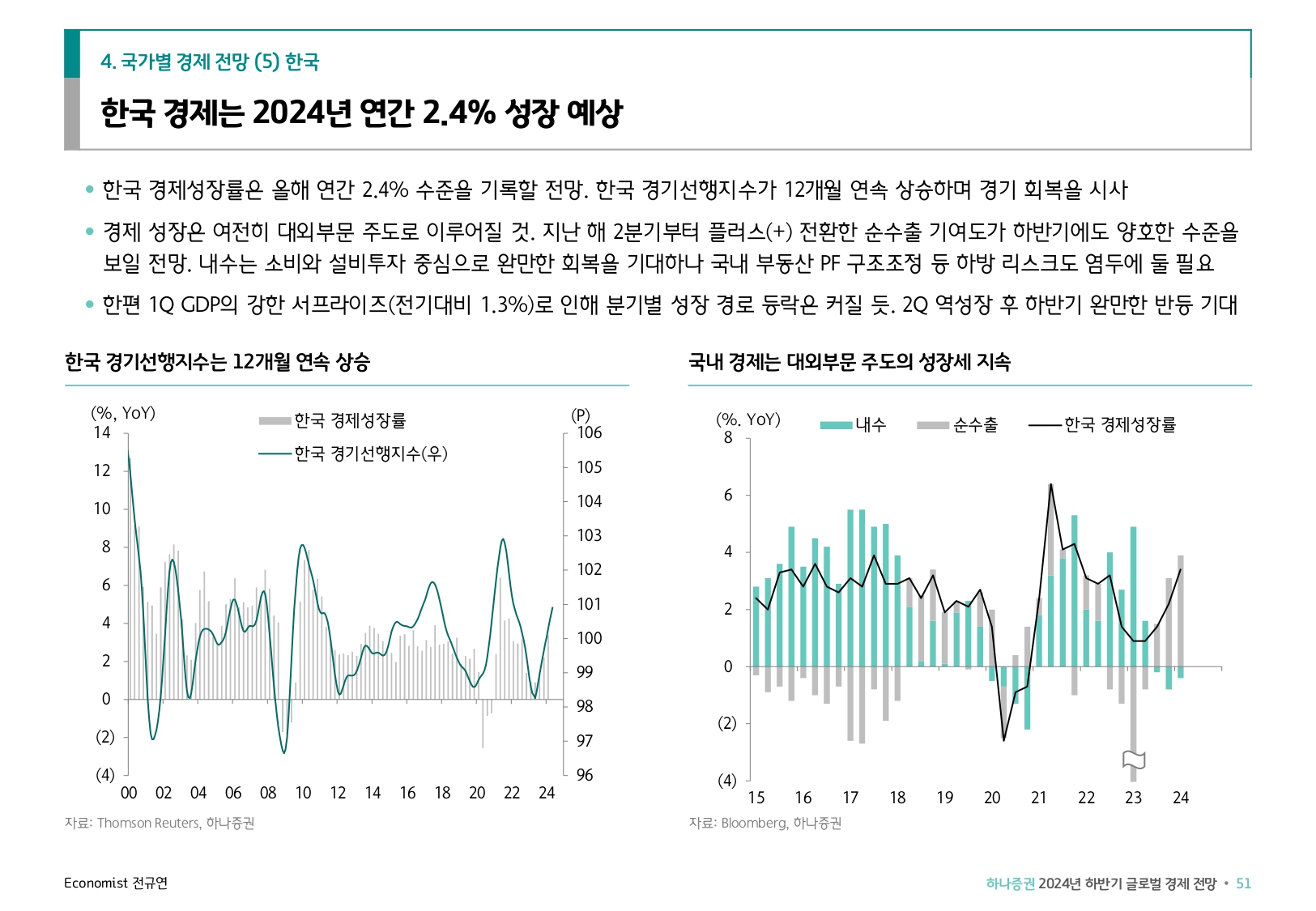

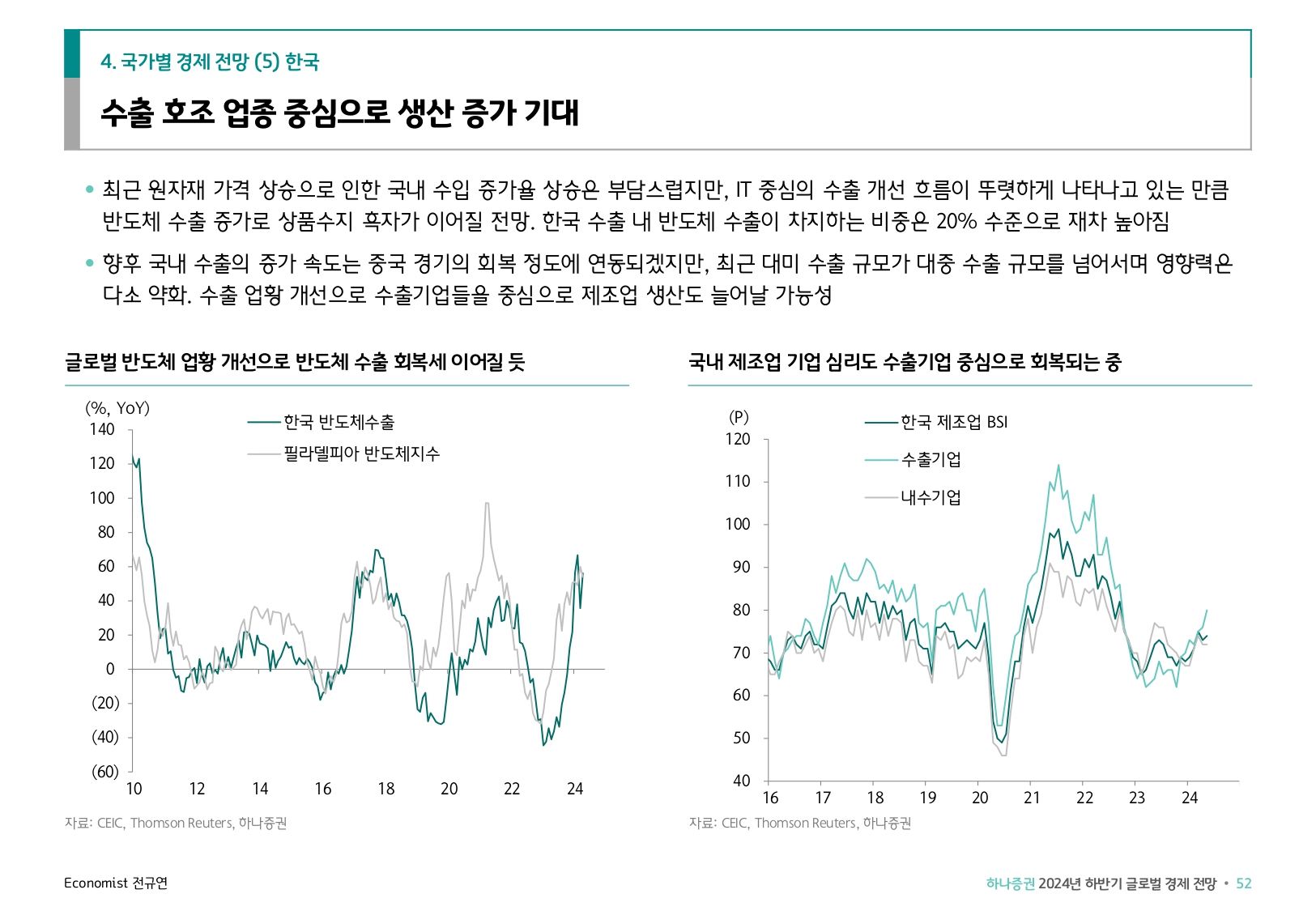

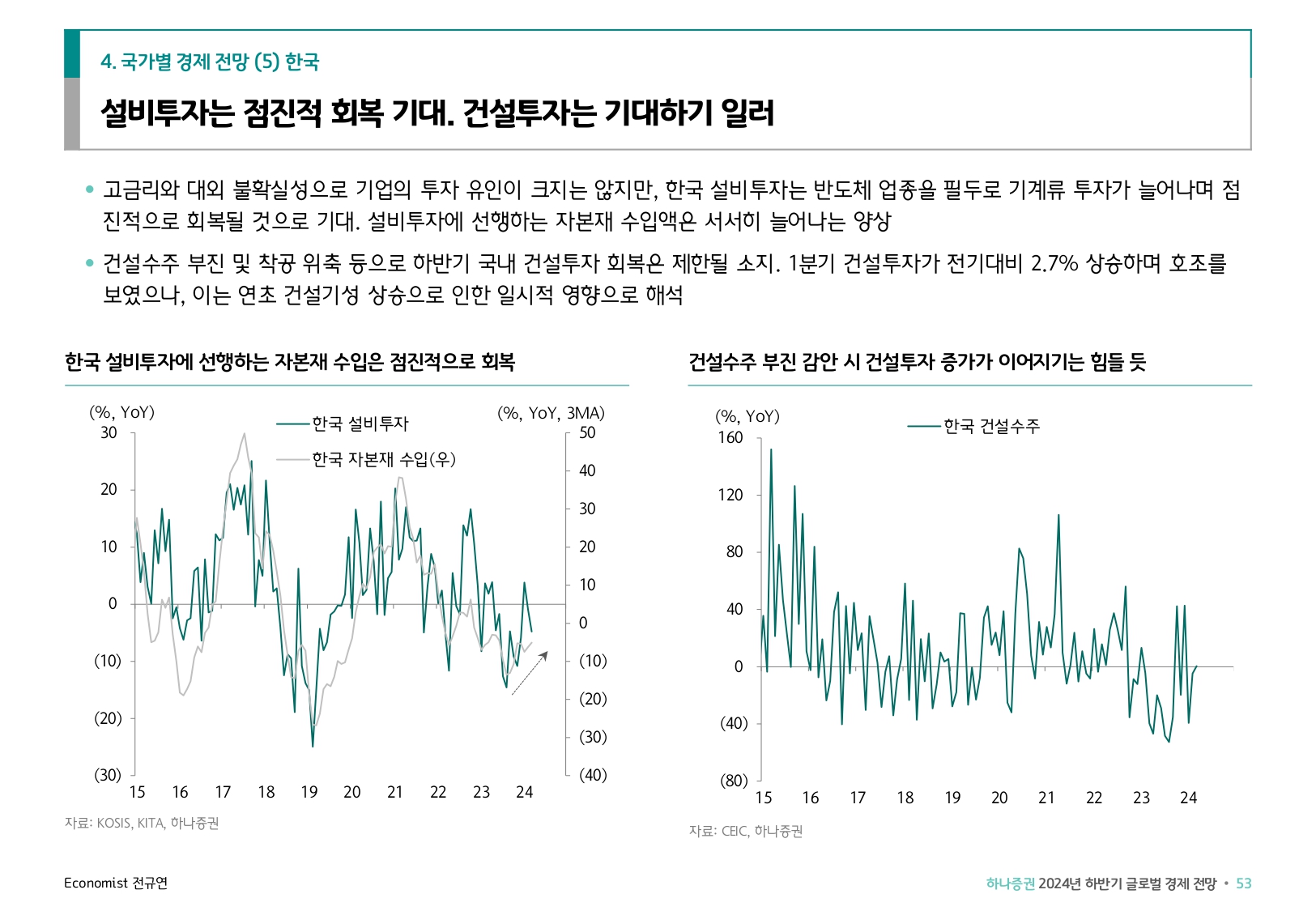

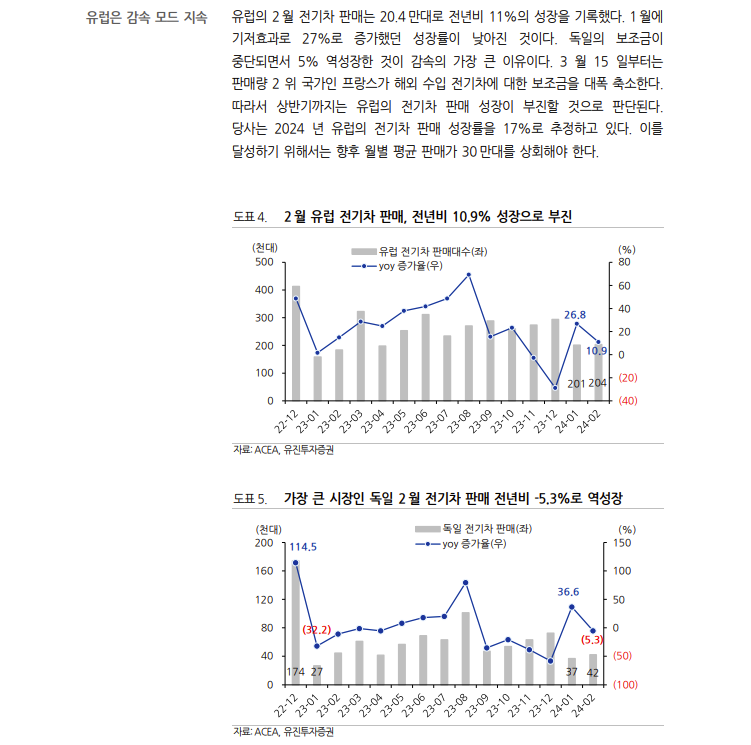

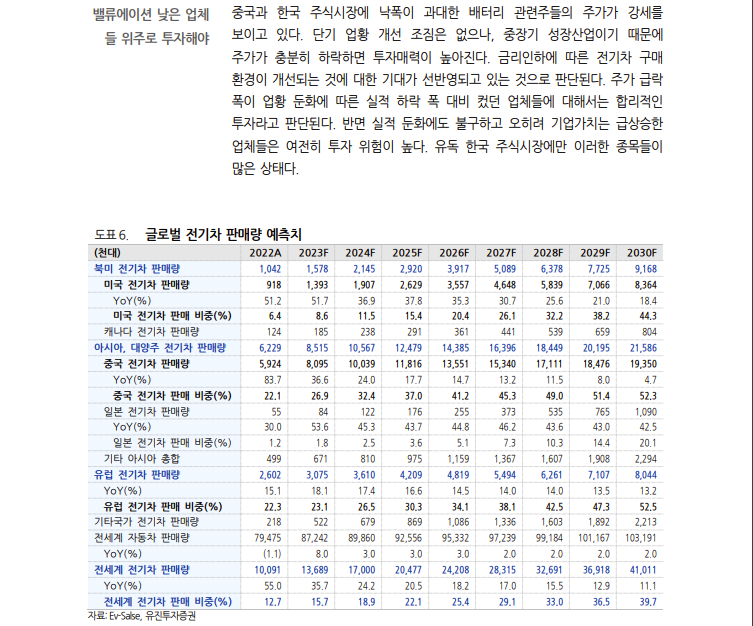

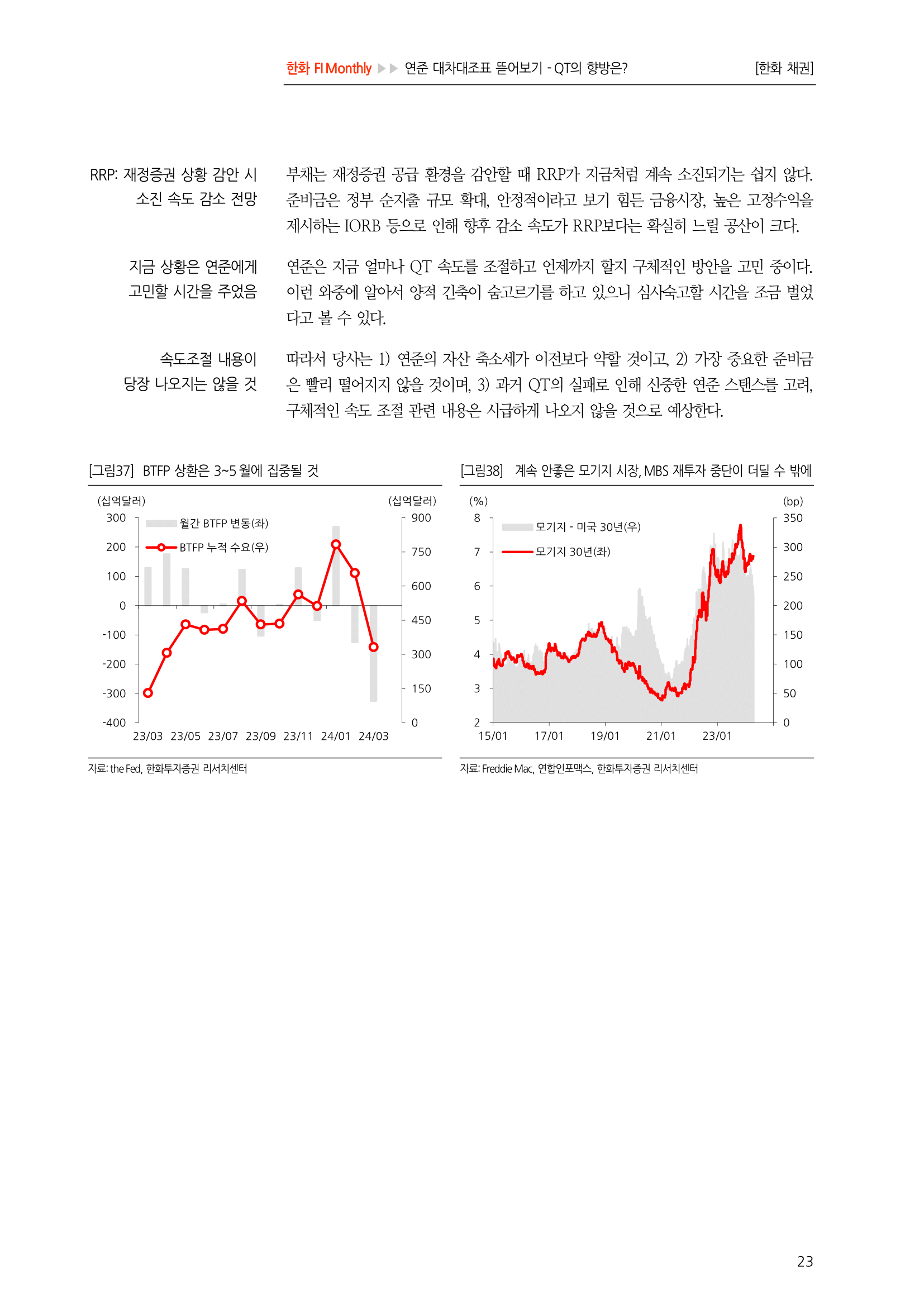

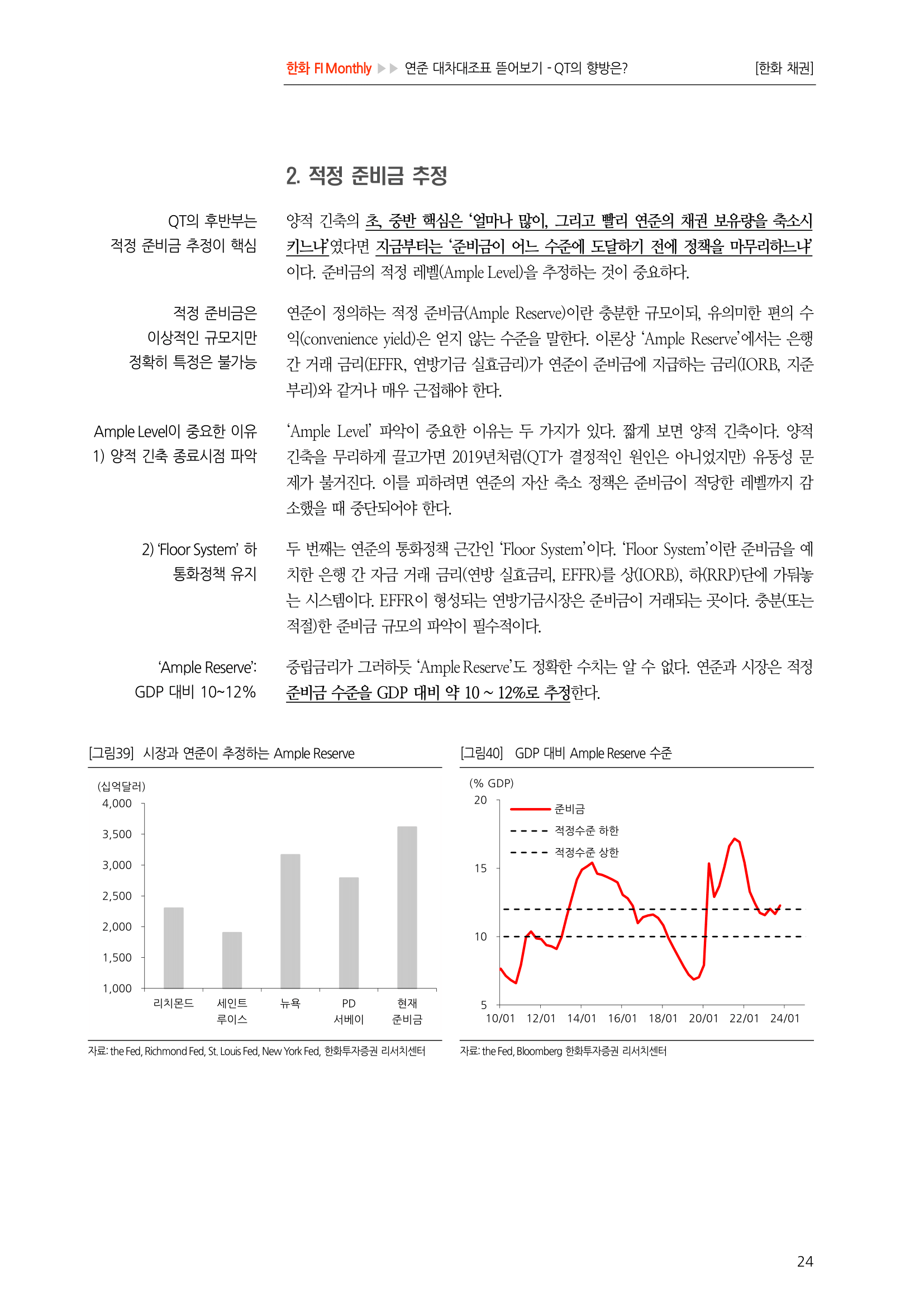

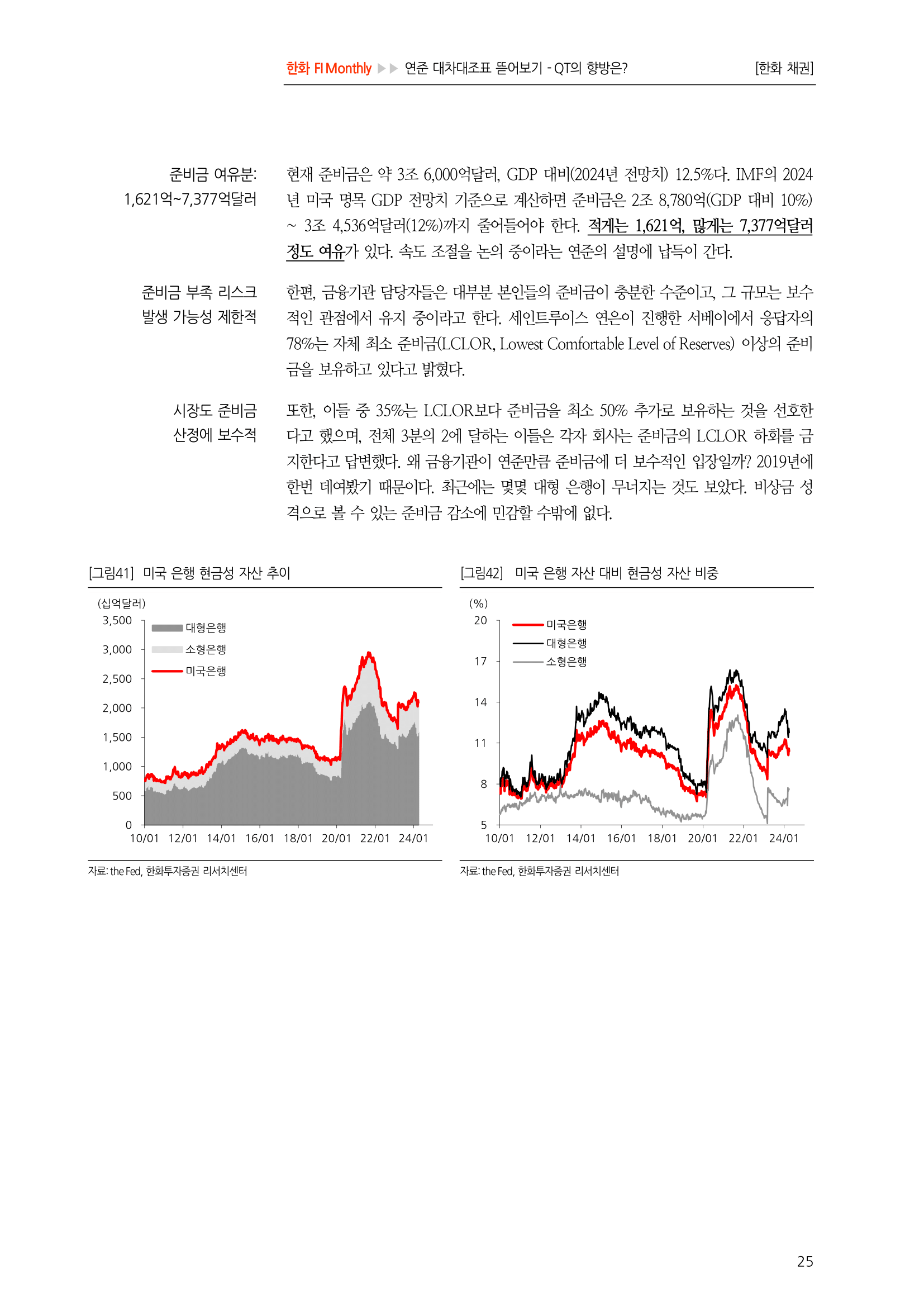

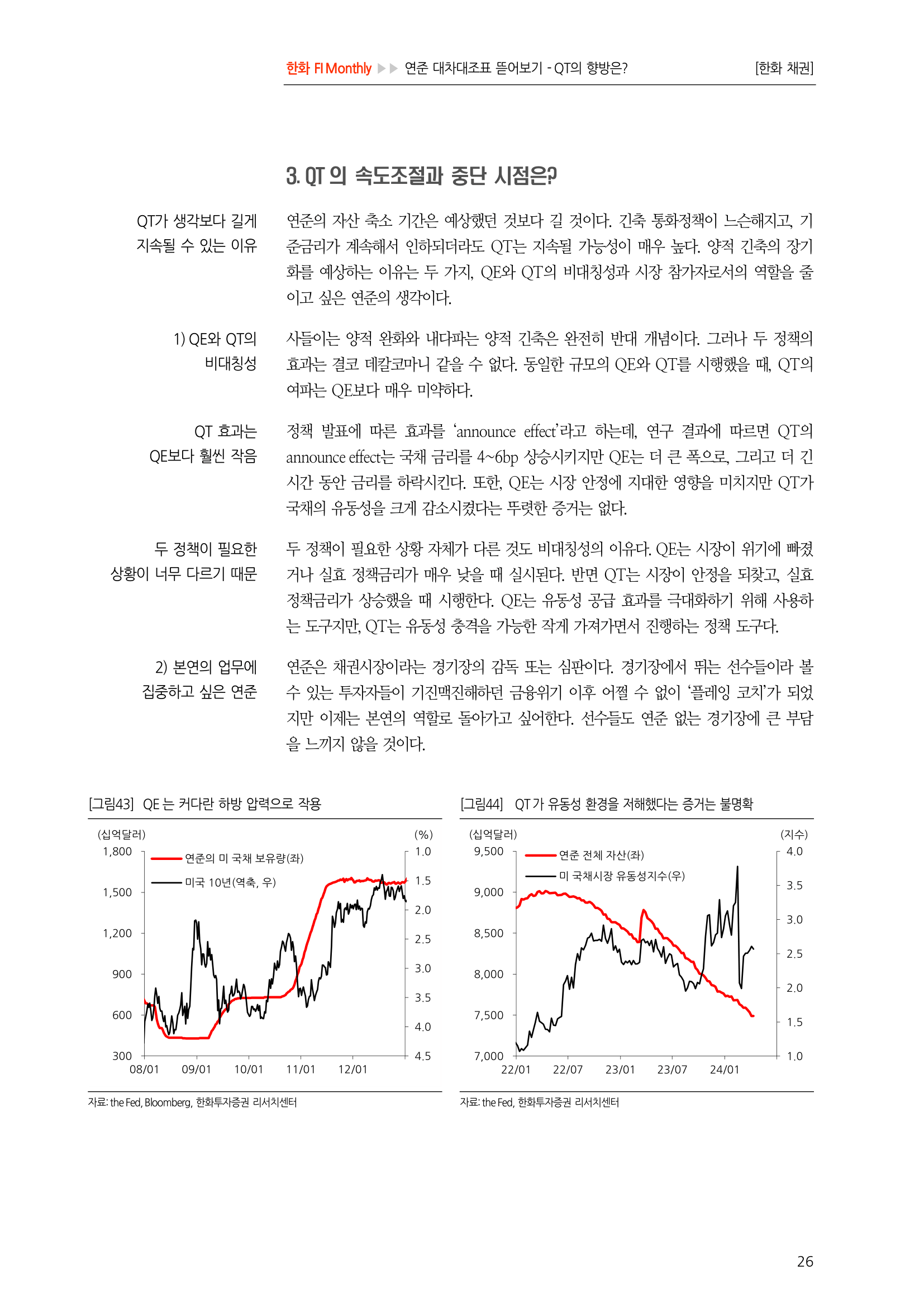

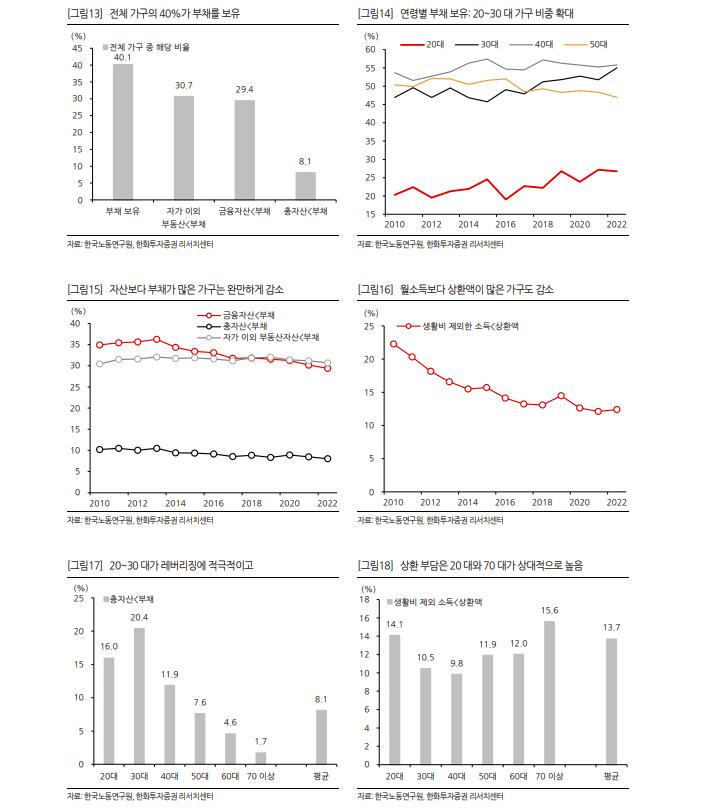

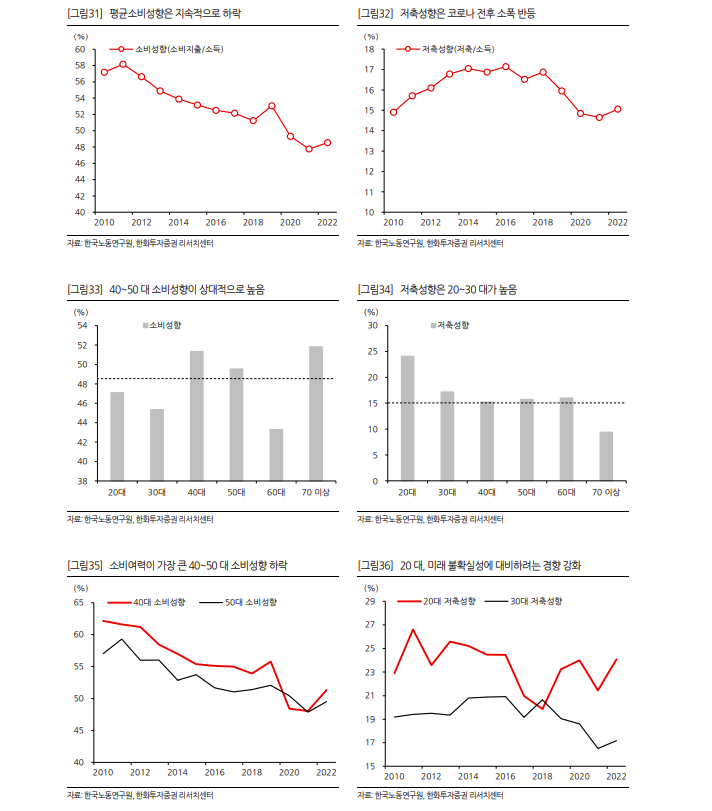

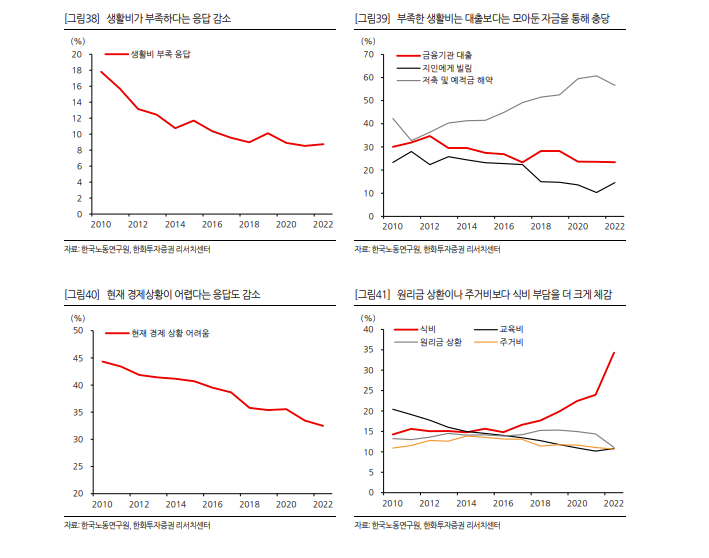

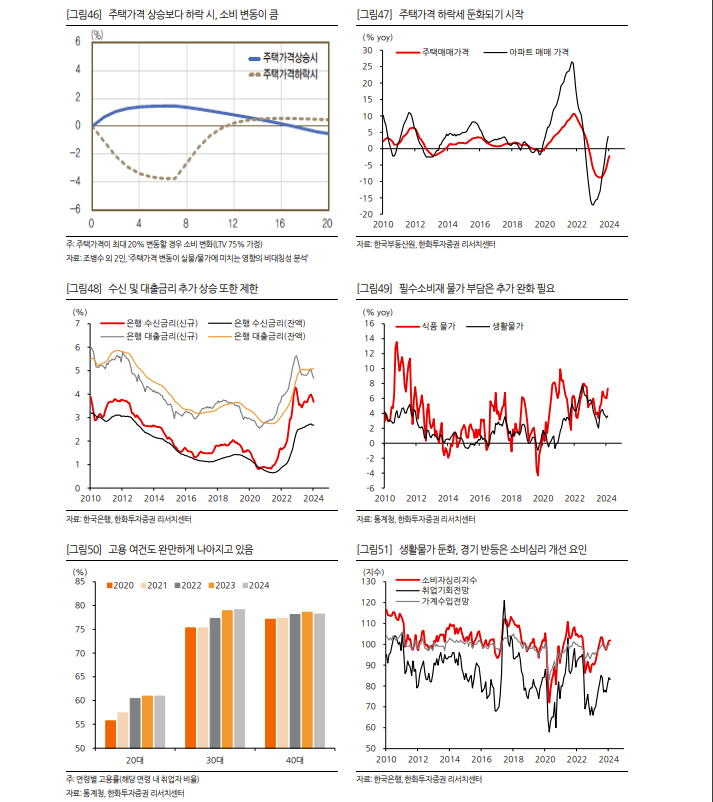

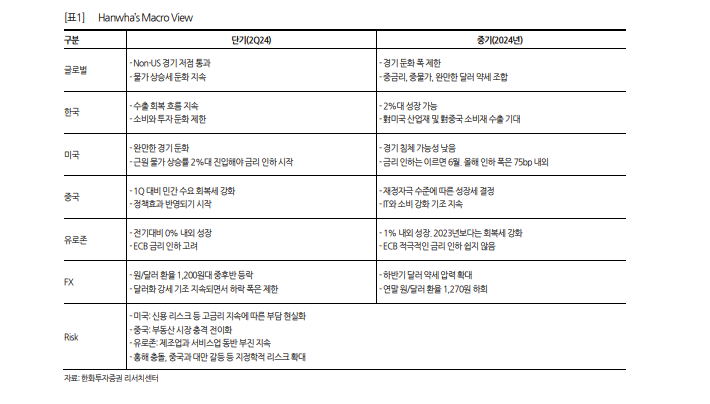

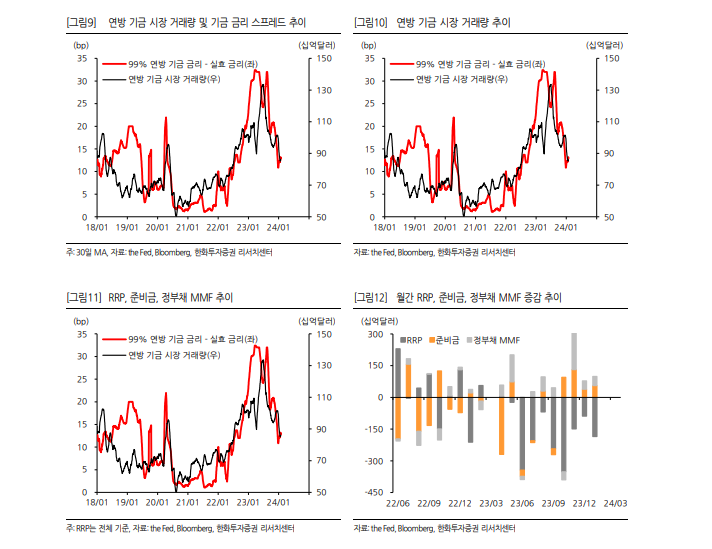

재정지출 확대 원인: 인구 노령화로 인한 복지 프로그램 지출, 지정학적 위기에 대한 미국 가버넌스 약화로 전쟁 지원금 확대, 탈세계화에 따른 공급망 재편 인센티브 제공 위해 정부 보조금 사용

탈세계화에 따른 공급 감소 우려로 고금리 장기화 전망

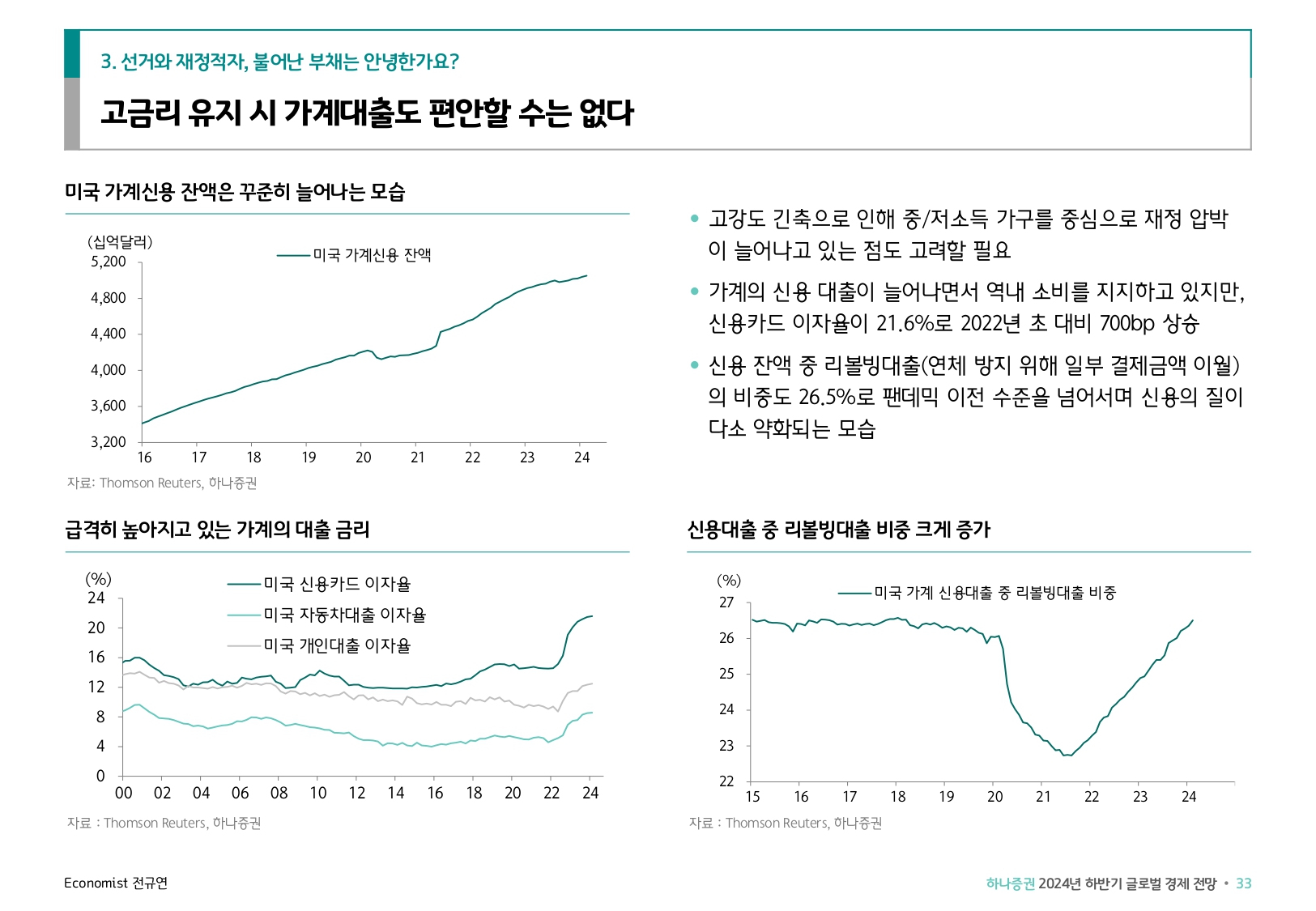

모기지 금리 증가로 거주 이전 인센티브 감소하며 노동 효율 감소

Higher Interest Rates Are Here to Stay. What It Means for the Economy.

Even as inflation eases, global changes including less trade and growing government deficits will keep rates higher than before.

As Federal Reserve officials head into their final policy meeting of the year, on Dec. 12-13, both Wall Street and Main Street are fixated on the outlook for interest rates.With inflation falling steadily, how soon—and how aggressively—will the U.S. central bank cut rates in the coming year?

As Federal Reserve officials head into their final policy meeting of the year, on Dec. 12-13, both Wall Street and Main Street are fixated on the outlook for interest rates.With inflation falling steadily, how soon—and how aggressively—will the U.S. central bank cut rates in the coming year?

The better question is where rates will settlein the coming decade. The probable answer: below today’s target range of 5.25%-5.50%, but higher than many economists and policy makers expected a year or two ago, and far higher than the near-zero rates of the past 15 years. The consequences will be profound, though not entirely detrimental, affectingthe global economy, investment portfolios, and monetary and fiscal policy for years to come.

Expectations for the long-term trajectory of interest rates lie at the heart of a debate over the so-called neutral rate, or the interest rate at which the economy is in equilibrium, with monetary policy neither too tight nor too loose. A growing chorus of economists argues that structural shifts in the economy that were either introduced during or exacerbated by theCovid pandemic are pushing the neutral rate higher than it has been in decades.

Advertisement - Scroll to Continue

There are a handful of factors at play: Governments are spending more freely without raising taxes, pushing up deficits. Consumer demand has proved to beremarkably persistent. A slowdown in globalization has led to both a decline in trade volumes and a costly effort to bring supply chains closer to home,making consumer goods more expensive.

These changes,among others, have led to increased friction in the economy and will make it more prone to bouts of inflation moving forward, economists say, forcing monetary policy to run tighter as a result. Since 2019, Fed officials’ median forecast has put the longer-run federal-funds rate—effectively their estimate of neutral—at 2.5%. That equates to a 0.5%real neutral rate, after subtracting the Fed’s 2% inflation target.

Now, many economists believe that the federal-funds rate could settle in the mid–3% range, or even as high as 4% over the longer term. Adjusted for inflation, that implies an anticipated real neutral rate of 1.5% to 2%—three or four times the level that officials were predicting a few years ago.

“That is a very different world from the world we left,” says Diane Swonk, chief economist with KPMG.

There is a catch. The neutral rate can’t be measured, and can be estimated only in hindsight. Yet gauging its level isparamountfor Fed policy makers as they weigh whether and when to cut interest rates, and how best to minimize economic damage while cooling inflation further.

If officials assume that the neutral rate is higher than it really is, they risk overtightening monetary policy. If they assume it is lower, as some economists fear the Fed is doing, they risk tightening insufficiently, thereby allowing the economy to reflate within a matter of months. Taming resurgent inflation would require even more painful monetary tightening.

“Part of the reason why I think many of the projections, including those in the markets, for cutting rates overdo it a bit is because they presume that policy is more contractionary than it already is,” says former Treasury SecretaryLarry Summers. “They assume too low a neutral rate.”

Expect the debate over “neutral” to dominate economic policy discussions in the coming months. But it will take on even greater importance thereafter, as economists and Fed officials attempt to map out what the economy might look like once price growth settles back to the Fed’s 2% annual target, and how it will compare with the pre-Covid era.

To be sure, a higher neutral rate isn’t a foregone conclusion. Opinions vary, and unexpected events, such as another financial crisis or pandemic, could force the Fed and other central banks to push rates much lower.

But for now, even Fed officials have begun to signal that they believe the neutral rate is rising. In the central bank’s quarterly projections released in March, only four officials wrote that they believed the neutral rate had climbed above 2.5%. By September, seven officials said the same. Officials will publish their latest projections on Dec. 13, at the close of the Federal Open Market Committee meeting.

The long-run implications of a higher neutral rate are substantial. Money would no longer be as cheap as it was for much of the 2010s. Debt would be more costly, and loans would bemore difficult to secure. Start-up businesses would face heightened pressure to turn profits quickly, and fewer would get off the ground.

Advertisement - Scroll to Continue

But there would be benefits, too. Savers and retirees would profit from higher-yielding fixed-income investments. Higher rates would encourage more saving and more-efficient capital allocation. And central banks would have room to adjust rates lower in the event of an economic slowdown, which would make for a less volatile economy.

“This, in my mind, is the single best financial market development in the past 20 years,” says Joseph Davis, global chief economist at Vanguard. “And there’s nothing close.”

It wasn’t so long ago that economists and policy makers werefocused on why wage and productivity growth were so sluggish, and whether inflation would ever climb back to the Fed’s annual 2% target growth level. Despite more than a decade of ultralow rates, core personal-consumption expenditures—the Fed’s preferred inflation gauge—topped 2% in only five months from 2010 to 2020.

The explanation that was growing in popularity before Covid hitwas that the neutral rate must be lower than anyone had thought. Slowing productivity and an aging workforce appeared to be weighing down the economy in such a way that monetary policy would need to remain loose for price growth to return to target.

Ultralow inflation and ultralow interest rates were makingfor an unusual equilibrium. “It’s hard to get out of that cycle without a major shock,” says Kristin Forbes, an economics professor at the Massachusetts Institute of Technology.

Then Covid arrived, upending the global economy. While the factors believed to be dragging down the neutral rate pre-Covid haven’t been eliminated, they have now been overshadowed by fresh changes that have left the economy more prone to global shocks and bouts of inflation.

Advertisement - Scroll to Continue

“We went through the proverbial looking glass, into a mirror image of the world we left,” says Swonk.

Among the most influential changes hasbeen the ballooning of government deficits, and the propensity of manyWestern governments to spend freely on policy initiatives without ensuring a commensurate increase in tax revenue to offset the costs. In the U.S., debt held by the public ballooned as a share of overall GDP from 79.4% in 2019 to 99.8% in 2020, and it’s projected to increase sharply in the coming decade.Datafrom the International Monetary Fund show that a number of European countries, including Germany and the United Kingdom, have seen similarly steep rises in recent years.

This increased deficit spending is due partly to the post-financial-crisis embrace of quantitative easing by central banks, which gave governments a regular buyer for their debt, says Torsten Sløk, chief economist at Apollo Global Management.

The combination of reduced savings and increased spending will stimulate the economy, pushing up the neutral rate over time.And a number of new trends suggest that generous federal spending is poised to continue. Consider governments’ embrace of climate-change mitigation: The continuing green transition will require expensive investments to find alternative sources of energy, while the increased frequency of natural disasters and other weather events will require costly recovery efforts.

Aging populations, too, require elevated levels of government spending on healthcare and entitlement programs, which will be major contributors to the forecast rise in the U.S. deficit in coming decades, barring political changes. Likewise, rising geopolitical tension has necessitated an increase in military spending in high-income nations. The war in Ukraine pushed total global military expenditure up 3.7% in 2022, and European spending saw its largest year-over-year jump in at least 30 years, according to theStockholm International Peace Research Institute.

Future totals could edge higher still: In the U.S., the proposed Department of Defense budget for fiscal-year 2024 came in 5% above the level that had been anticipated a year earlier, and the Congressional Budget Officeforecaststhat the agency’s overall costs will rise10% from 2028 to 2038.

Advertisement - Scroll to Continue

Heightened global tension is one result of a trend toward global fragmentation, which has led to a slowdown in worldwide trade and a renewed focus on building supply chains closer to home to minimize risk. Both shifts are likely to stoke inflationand weigh on growth. In a similar vein, an industrial-policy push for more domestic production of technology such as semiconductors has led to an increase in the use of government subsidies to incentivize investment in higher-wage nations.

In all, annual public expenditure in the U.S. could increase beginning next year by a level equivalent to 2% of gross domestic product, says Adam Posen, president of the Peterson Institute for International Economics. Other Group of Seven nations and China, he adds, are behind the U.S. but on a similar track.

“This is substantial,” Posen says. “And there is very little prospect in the near term for raising taxes.”

There is no telling yet whether any of these shifts will become permanent. But their impact has already been greater and more persistent than initially expected, a point that European Central Bank President Christine Lagarde made in a speech at the Fed’s Jackson Hole economic policy symposium in August.

That could have significant implications for the Fed’s inflation fight, where progress in reducing core inflationfrom a current annual rate of 3.5% down to 2% could prove slow. More important, it could also affect where price growth and the neutral rate settle in the future.

Says Summers: “2% is looking more and more like a floor on inflation, rather than an average inflation rate over time.”

Even assuming the neutral rate has risen, there is disagreement about what this will mean for the economy and whether it will help or harm business owners, consumers, and investors.

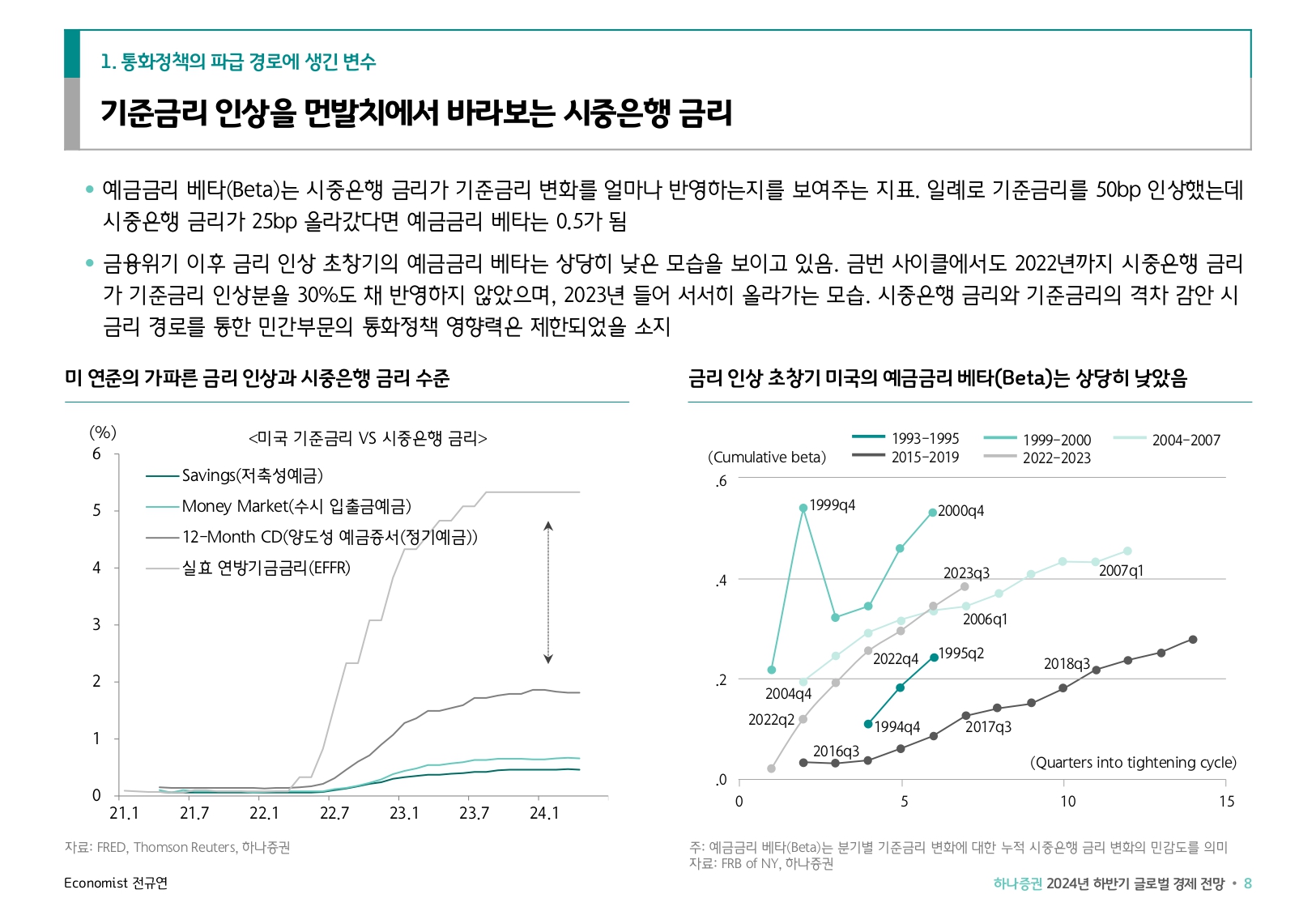

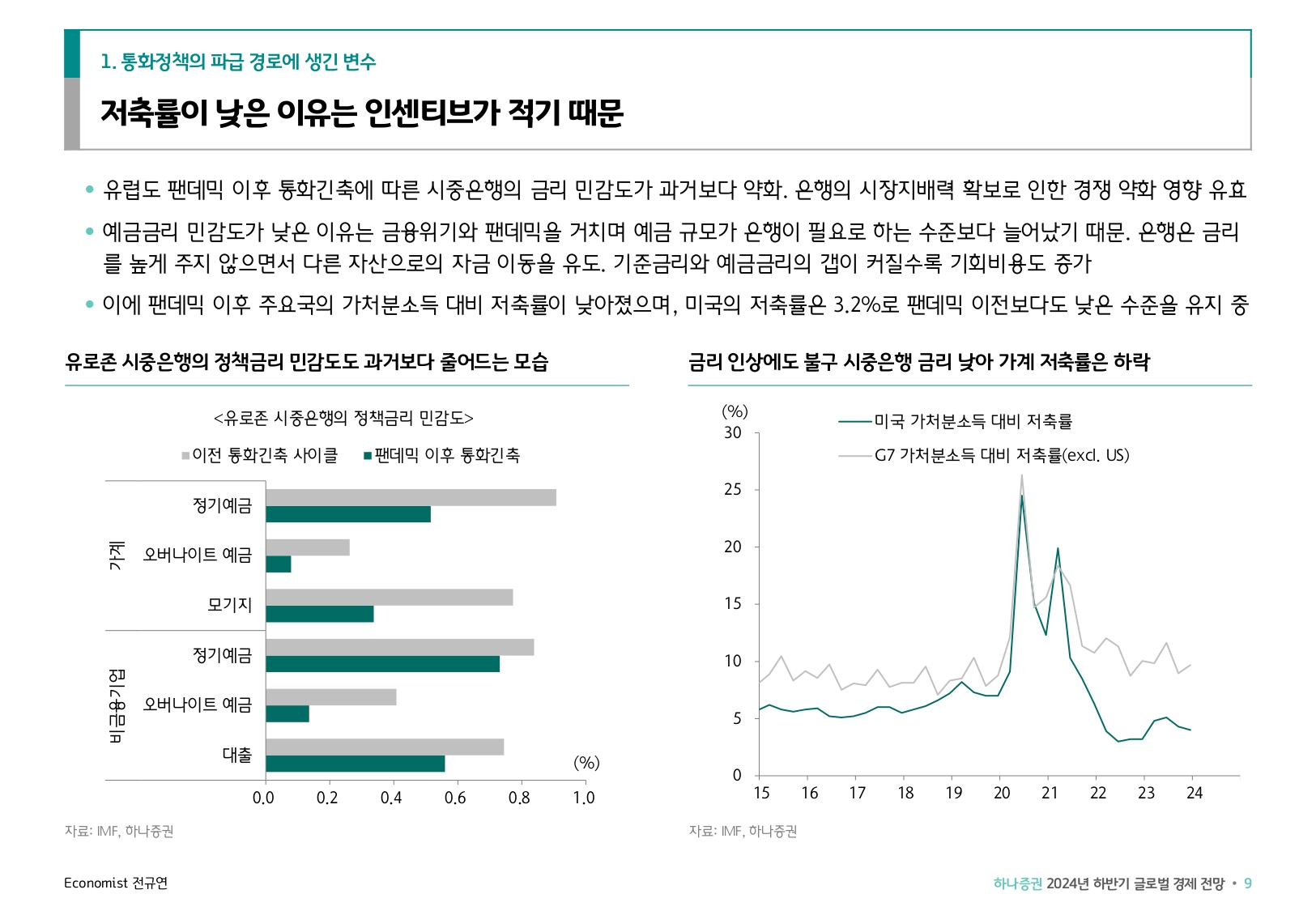

One concern is that higher rates could throw sand in the gears of the housing market by exacerbating affordability problems. In the U.S. especially, where many homeowners locked in 30-year mortgages in recent years at rates below 4%, there is an incentive to stay put rather than move, given how much more expensive the next loan would be. As a result, prospective home buyers are facing not only higher mortgage rates but also less housing supply, since fewer existing homes are coming on the market than in the past.

Advertisement - Scroll to Continue

One ripple effect could be a less efficient labor market, says MIT’s Forbes. Mobility has long been a hallmark of the U.S. economy, helping to support wage growth by allowing workers to move to take a more lucrative position.

“If you’re constrained because you don’t want to sell your house,” Forbes says, that can “take away some of the bargaining power of workers.”

The shift to a higher-rate regime over the long term will also tax millions of companies launched in the past 15 years, which have never knownanything other than the easy-money policies that haveprevailed since early 2009. That could lead to at least a brief increase in bankruptcy filings as the corporate sector adjusts to paying more to borrow money.

It could become more difficult for firms to get off the ground, too. For much of the past decade, entrepreneurs could borrow capital at little cost, allowing them to keep their doors open for years without turning a profit. “Now, you need to have a business that actually makes money, and makes money sooner, because the discount rate goes up,” Sløk says.

When debt costs more in a higher-rate world, there is less money available for otherwise fruitful investment, a shift that will be felt particularly in the public sector. U.S. interest costs nearly doubled from 2020 to 2023 and are the fastest-growing area of government spending, says theCommittee for a Responsible Federal Budget. The U.S. is on track to spend more than $13 trillion on interest costs over the next decade, the committee projects.

Given that growth, the average citizen will get less value from the government, Posen says.

Advertisement - Scroll to Continue

“To make it sound very bloodless,” he continues,“there is a robust empirical relationship across countries over time that if you have higher government interest payments as a share of GDP crowding out private-sector and public-sector investment, you have low innovation, a low rate of productivity growth, a low rate of growth overall.”

That said, the transition away from easy money has benefits, too, even if the positives are more often overlooked.

Although a higher cost of capital means that loans might be harder to come by, the best ideas will still find funding. And better capital allocation means funding will go to innovations, technologies, or projects that are best poised to take off. That could lead to better economic results, says James Bullard, the former president of the St. Louis Fed.

“I love innovation as much as the next person, but it shouldn’t just be willy-nilly,” says Bullard, now the dean of the business school at Purdue University. “You may have better discipline if you have somewhat higher real rates.”

For investors, the benefits can be even more tangible. Savers will be rewarded as cash compounds, allowing for higher returns. That is particularly beneficial to older Americans, including many retirees, who tend toward more conservative fixed-income investments.

“You’re seeing a tidal wave of change in how people think about [getting] income into portfolios,” says Rick Rieder, chief investment officer of global fixed income at BlackRock. “You can now build a portfolio to get 6%, 6.5%, 7% yield using quality fixed-income assets.”

Even those who regard higher rates as a plus for both the economy and investors recognize that there will probably have to be a painful transition period before we settle into the next equilibrium.While the economy has handled the jump from near-zero interest rates to the current level remarkably well,due in part to sustained fiscal spending, signs of a slowdown have emerged recently. Those are likely to become more noticeable in the coming months as the restrictive regime takes hold more fully and so-called zombie firms propped up by stimulus spending and low rates start to collapse.

Then, the benefits will come.

Vanguard’s Davis pictures a bell curve when thinking about growth under various interest-rate levels. Exceedingly high rates such as those seen during former Fed Chair Paul Volcker’s era in the 1980s stifle growth. But near-zero rates can promote a sluggish environment, too, he says. While they might stimulate asset prices in the short term, long-term returns fall because there is no base rate to compound.

Settling somewhere in the middle brings the most benefit, notwithstanding any interim pain. “There is a transition here,” he says. “But I would take that transition any day.”